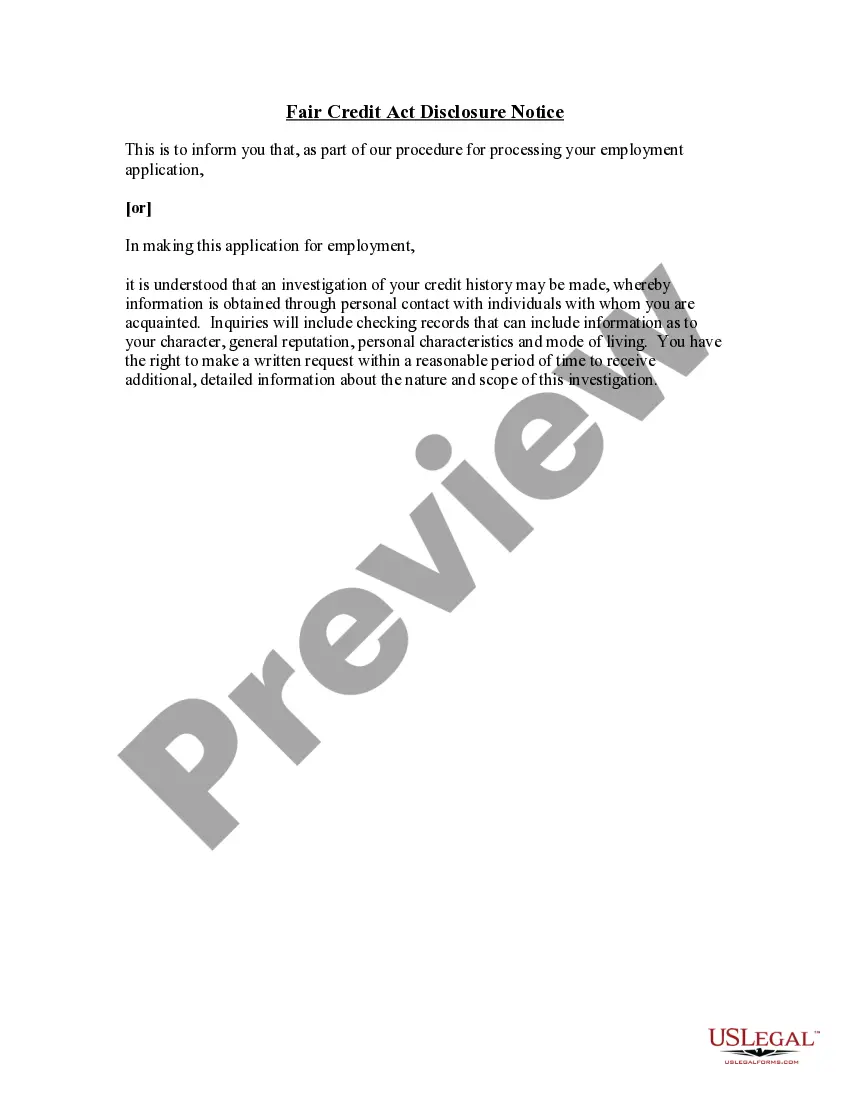

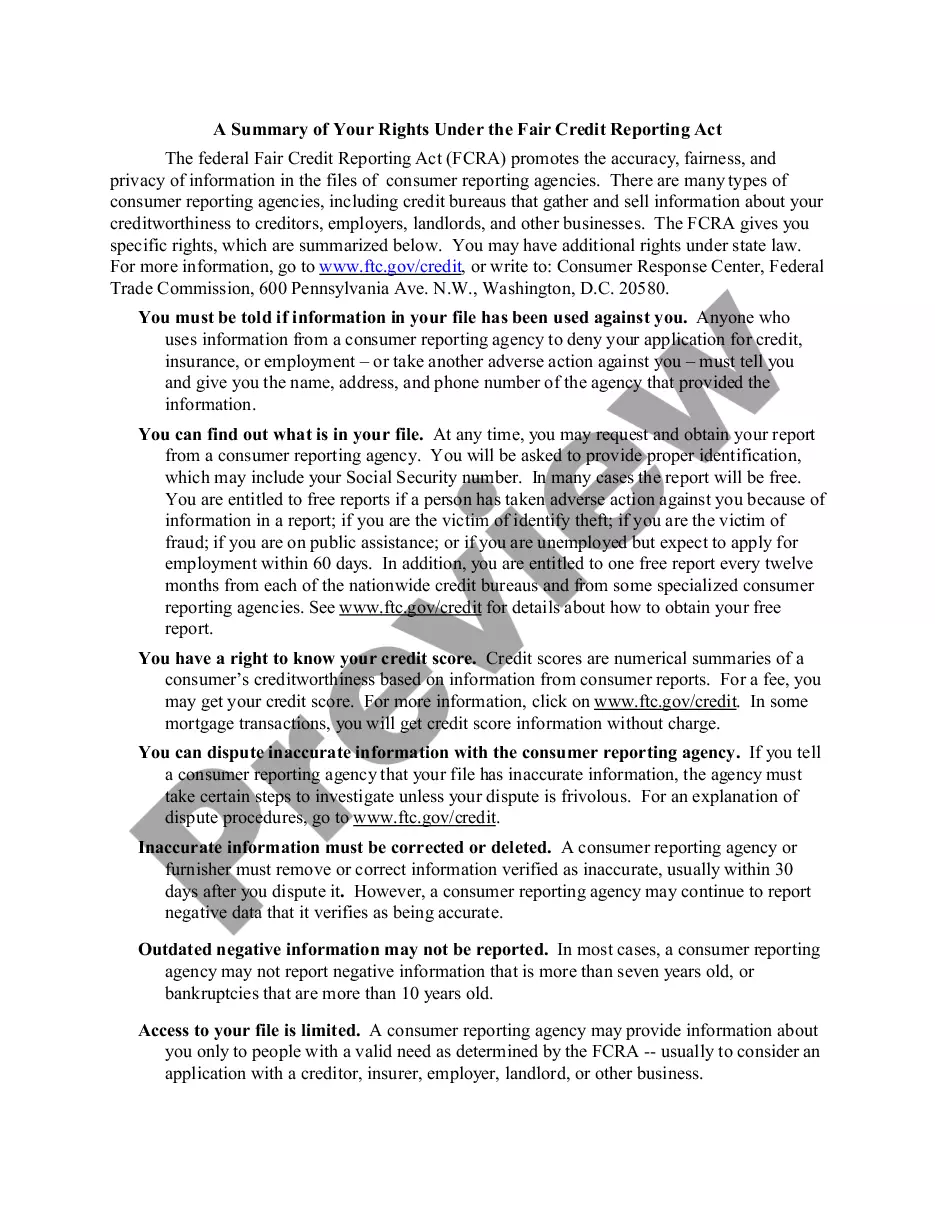

The Fair Credit Reporting Act (FCRA),15 U.S.C. 1681-1681y, requires that this notice be

provided to inform users of consumer reports of their legal obligations. The first section of this summary sets forth the responsibilities imposed by the FCRA on all users of consumer reports. The subsequent sections discuss the duties of users of reports that contain specific types of information, or that are used for certain purposes, and the legal consequences of violations.

Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA

Instant download

Description

Free preview

How to fill out Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA?

When it comes to drafting a legal form, it’s better to leave it to the professionals. However, that doesn't mean you yourself can’t find a template to use. That doesn't mean you yourself can not get a sample to use, however. Download Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA straight from the US Legal Forms site. It offers numerous professionally drafted and lawyer-approved documents and samples.

For full access to 85,000 legal and tax forms, users just have to sign up and choose a subscription. Once you are registered with an account, log in, find a certain document template, and save it to My Forms or download it to your gadget.

To make things less difficult, we have included an 8-step how-to guide for finding and downloading Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA fast:

- Make sure the form meets all the necessary state requirements.

- If possible preview it and read the description before buying it.

- Hit Buy Now.

- Choose the appropriate subscription for your needs.

- Make your account.

- Pay via PayPal or by debit/credit card.

- Select a needed format if a number of options are available (e.g., PDF or Word).

- Download the file.

When the Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA is downloaded it is possible to complete, print and sign it in any editor or by hand. Get professionally drafted state-relevant papers in a matter of minutes in a preferable format with US Legal Forms!

Form popularity

FAQ

Two federal laws the Equal Credit Opportunity Act (ECOA), as implemented by Regulation B, and the Fair Credit Reporting Act (FCRA) reflect Congress's determination that consumers and businesses applying for credit should receive notice of the reasons a creditor took adverse action on the application or on an

The statement that a dispute meets the requirements of the FCRA means both that the consumer filed a formal dispute, and that the CRA has issued a formal Notice of Results of Reinvestigation finding the asserted inaccuracy has been verified as accurate.

A dispute notice from a consumer must include: 1) Sufficient information to identify the account or other relationship that is in dispute, such as an account number and the name, address, and telephone number of the consumer; 2) The specific information that the consumer is disputing and an explanation of the basis for

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

The Fair Credit Reporting Act (FCRA) is a federal law that helps to ensure the accuracy, fairness and privacy of the information in consumer credit bureau files. The law regulates the way credit reporting agencies can collect, access, use and share the data they collect in your consumer reports.

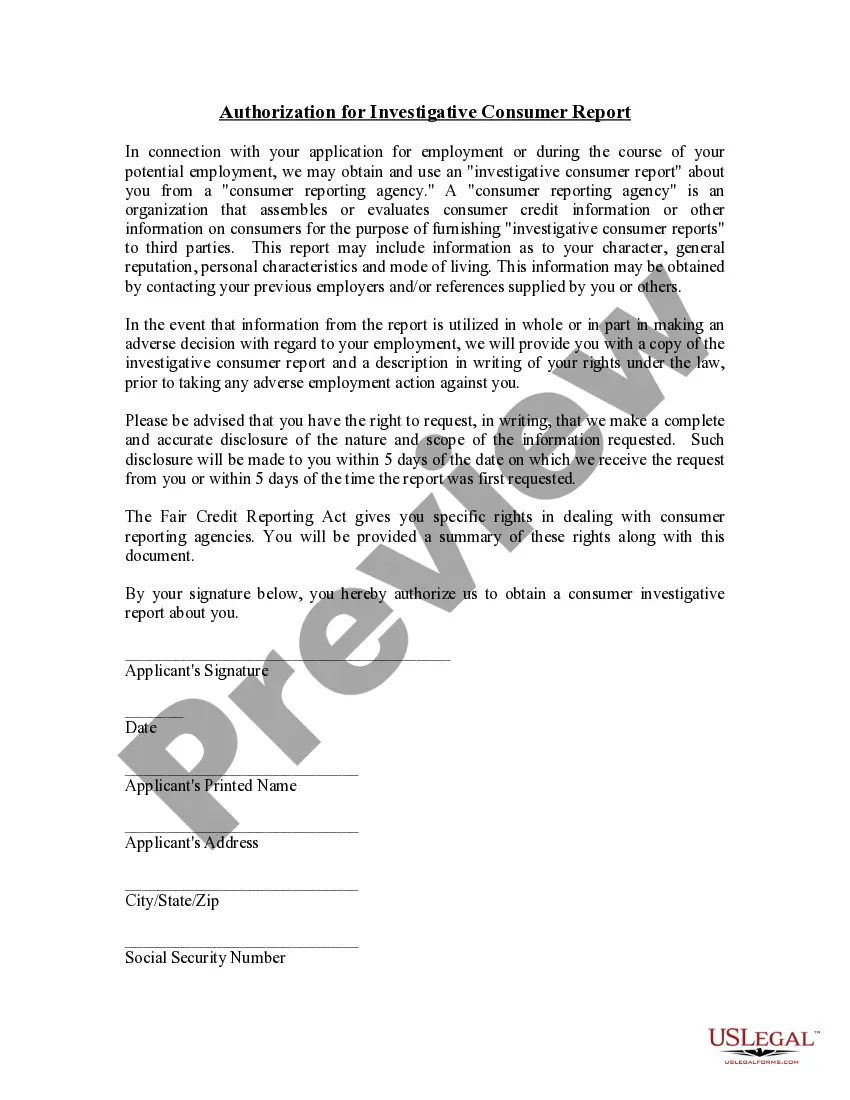

The FCRA defines a consumer report as any written or oral communication that meets all of the following conditions:220e It bears on a consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living.

File a Dispute. You can file your dispute through a written letter to the CRA (it's free to submit) or you can look up the CRA's online filing instructions. Wait. Once you've notified the CRA, it has 30 business days to investigate your claims. Get the Results. Your Report is Corrected. Complain.

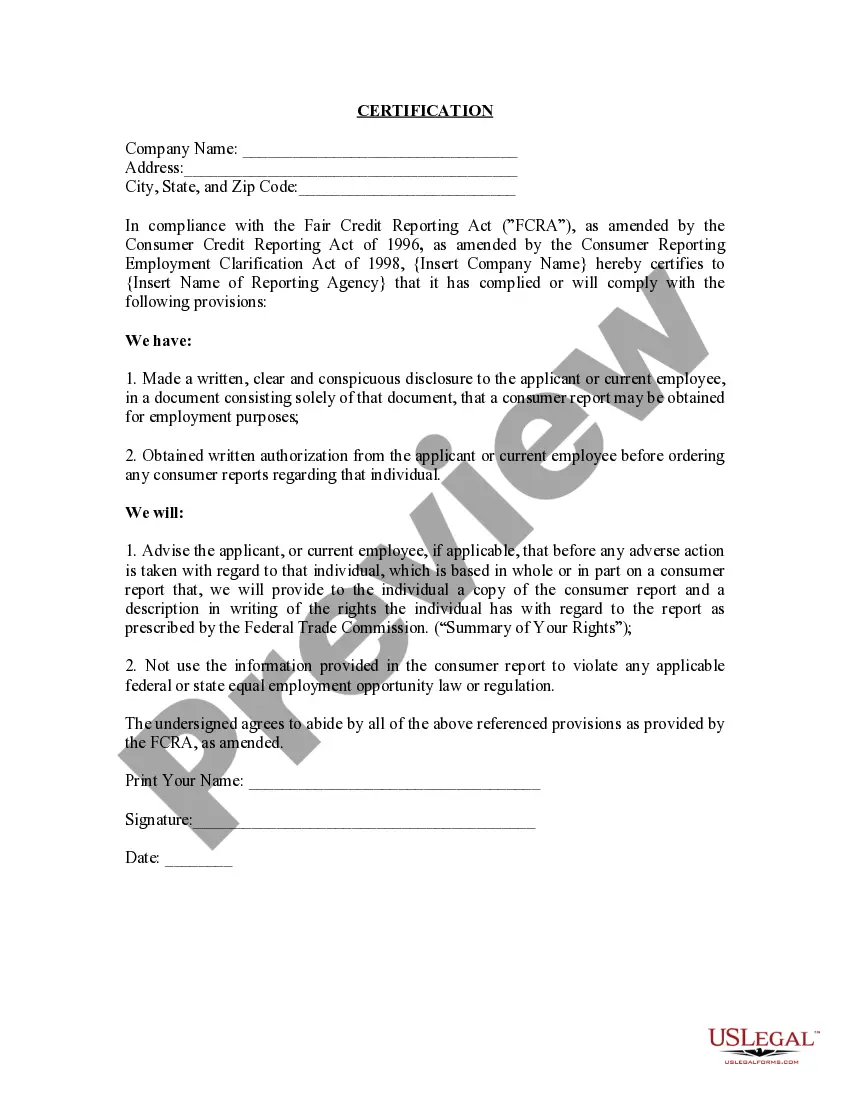

Notified the applicant or employee and got their permission to get a consumer report; complied with all of the FCRA requirements; and.

Common violations of the FCRA include: Creditors give reporting agencies inaccurate financial information about you. Reporting agencies mixing up one person's information with another's because of similar (or same) last name or social security number. Agencies fail to follow guidelines for handling disputes.