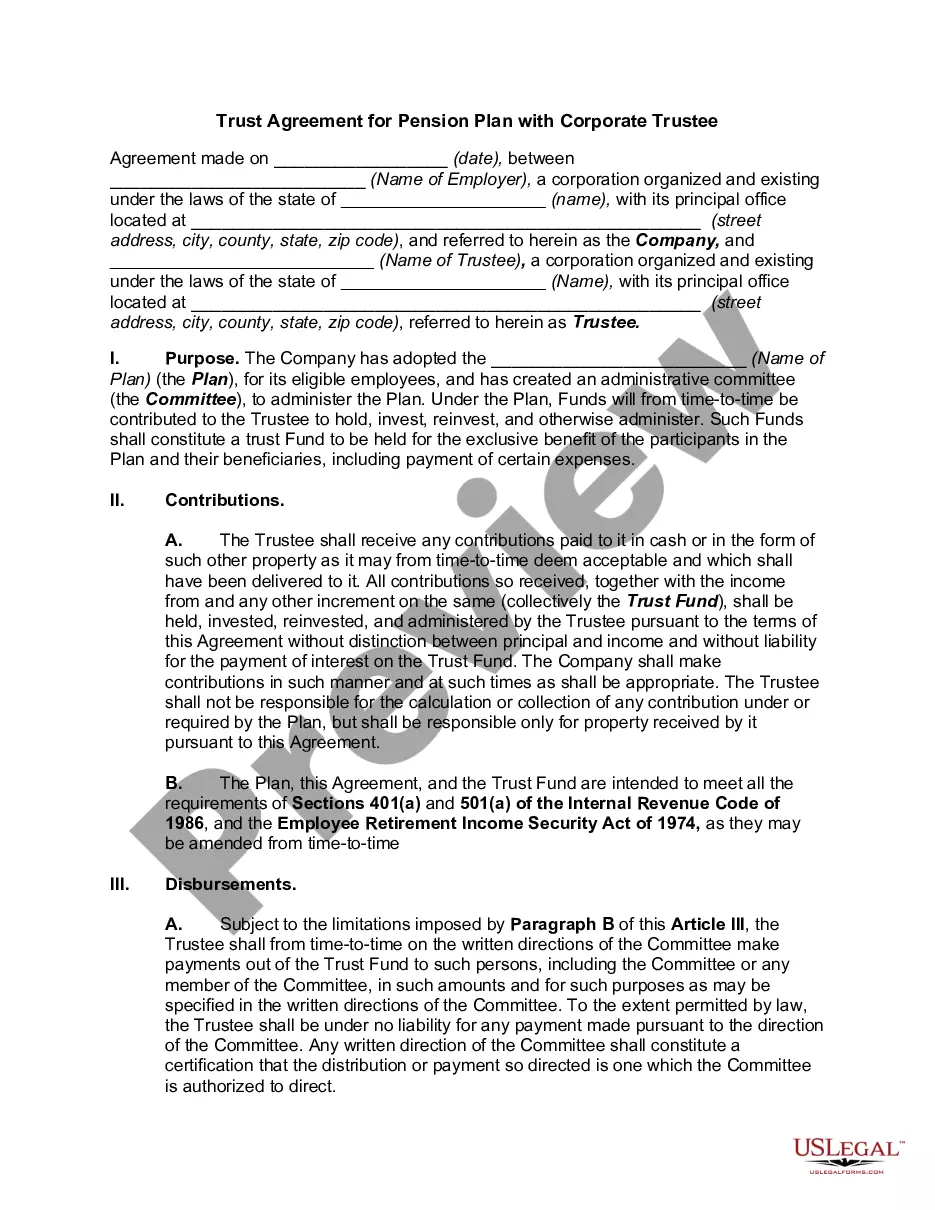

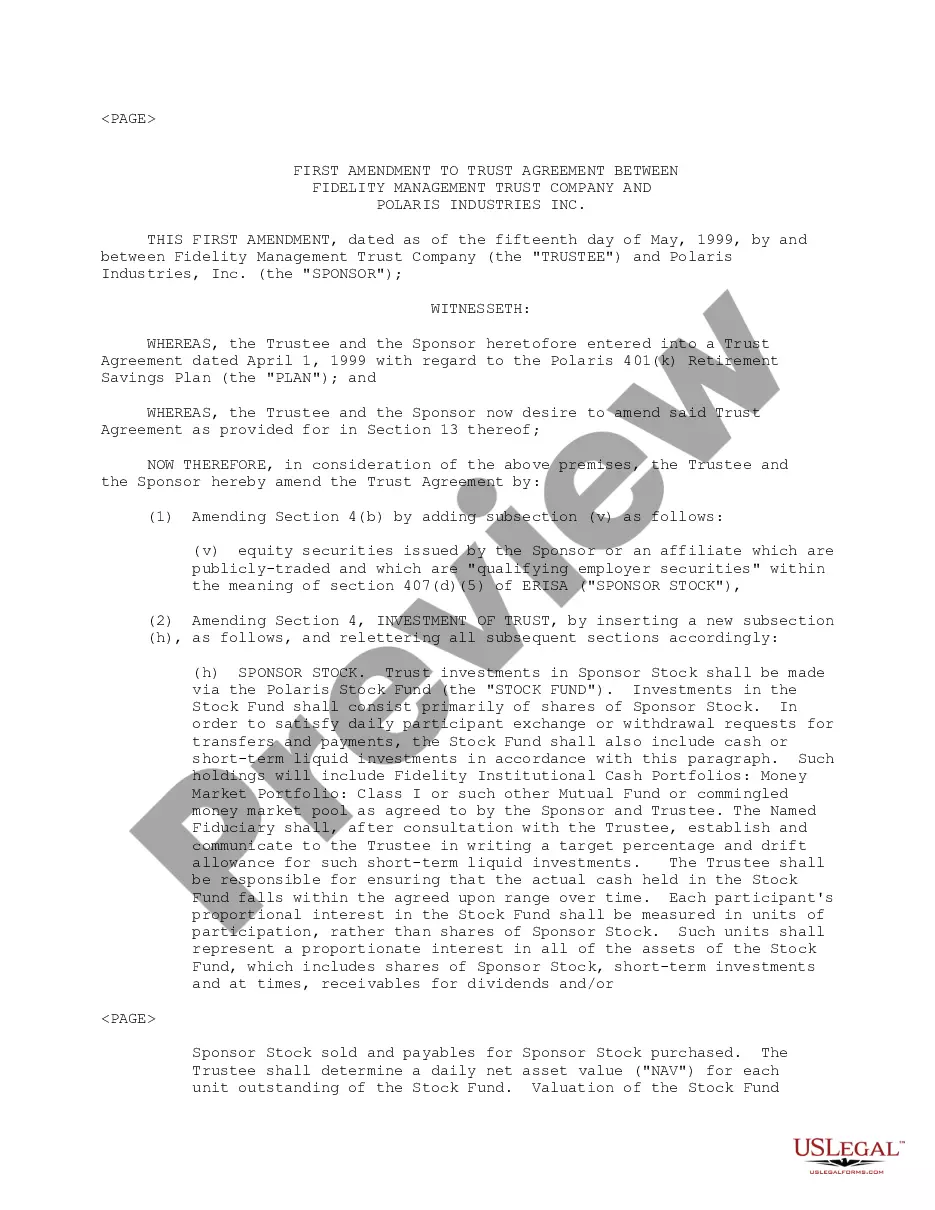

Polaris 401(k) Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust

What is this form?

The Polaris 401(k) Retirement Savings Plan Trust Agreement is a legal document that establishes a trust between Polaris Industries, Inc. and Fidelity Management Trust Company to manage and invest the assets of the Polaris 401(k) Retirement Savings Plan. This trust is specifically designed to ensure that plan assets are held and administered for the exclusive benefit of participants and their beneficiaries. Unlike other retirement planning documents, this agreement clearly outlines the responsibilities of the sponsor and trustee, including investment options and recordkeeping duties.

What’s included in this form

- Trust Establishment: This section declares the creation of the Polaris 401(k) Retirement Savings Plan Trust and specifies the initial contributions.

- Exclusive Benefit: Confirms that assets are exclusively for the benefit of plan participants and beneficiaries.

- Disbursements: Outlines procedures for disbursements from the trust, including administrator-directed requests and participant withdrawals.

- Investment Management: Details the investment options available and the process for participant investment directions.

- Recordkeeping Duties: Describes the responsibilities of the trustee for maintaining accurate records and providing reports to the sponsor.

- Amendments and Modifications: States how the agreement can be changed and under what conditions.

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

Retirement Savings Plan Trust Agreement between Polaris Industries, Inc. and Fidelity Management Trust Co. regarding establishment of trust")

When to use this document

This form should be used when establishing or managing a 401(k) retirement savings plan for employees. It is applicable in scenarios where a business aims to formalize the management of its retirement plan assets, ensuring compliance with legal regulations and providing a structured investment strategy for plan participants.

Intended users of this form

Individuals or entities who should use this form include:

- Businesses offering a 401(k) plan to employees

- Plan sponsors looking to provide a secure retirement savings option

- Trustees responsible for managing retirement plan assets

- Financial consultants advising on retirement plan structures

Steps to complete this form

To complete the Polaris 401(k) Retirement Savings Plan Trust Agreement, follow these steps:

- Identify the parties involved, including the sponsor (Polaris Industries, Inc.) and trustee (Fidelity Management Trust Company).

- Incorporate the initial contributions and outline the trust's assets.

- Specify disbursement methods and conditions for participant withdrawals.

- Define the investment options available to plan participants and the role of the named fiduciary.

- Ensure accurate recordkeeping and reporting mechanisms are established in line with the agreement.

- Include clauses for amendments to the agreement, ensuring clarity on the process of making changes.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it is advisable to consult with legal professionals regarding any specific requirements that might apply in your jurisdiction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to accurately identify the parties involved in the agreement.

- Neglecting to specify investment options which can cause confusion for participants.

- Ignoring FTC regulations regarding participant communications and reporting.

- Omitting necessary signatures, which may invalidate the agreement.

- Forgetting to amend the agreement when regulations change or if there are significant business changes.

Benefits of completing this form online

- Convenient access to a legally compliant trust agreement tailored for retirement plans.

- Expertly drafted by licensed attorneys, reducing the risk of error.

- Ability to download and customize the form for immediate use.

- Time-saving by providing a structured approach to managing retirement plan assets.

- The trust agreement provides a framework that complies with ERISA regulations, ensuring that retirement plans are administered legally and appropriately.

- It must clearly outline the roles of the sponsor and trustee to avoid any conflicts of interest or legal issues.

- Correctly completed, this document helps protect the rights of plan participants and beneficiaries.

What to keep in mind

- The Polaris 401(k) Trust Agreement is essential for managing retirement plan assets responsibly.

- Clear guidelines and roles enhance compliance with federal regulations.

- Proper execution of the form ensures legal protection for both the sponsor and plan participants.

Looking for another form?

Form popularity

FAQ

1Paying for Account Management.2Contribute the Max for the Match.3Learn the Basics of Investing.4Be Sure to Rebalance.5Learn to Love the Index Fund.6Be Wary of Target Date Funds.7Go Beyond Your 401(k)8The Bottom Line.

Call Your Old Employer. Use an Old 401(k) Plan Statement. Ask Former Employees. Be a Sleuth. Use Additional Government Document Recovery Tools. Leverage the National Registry. Looked for Unclaimed Money.

1Leave It With Your Former Employer.2Roll It Over to Your New Employer.3Roll It Over Into an IRA.4Take Distributions.5Cash It Out.6The Bottom Line.

Call 800-FIDELITY or 800-343-3548. Contact us to determine which retirement options would work best for you. I have a specific question about my 401(k) plan. Where can I learn more?

Since your 401(k) is tied to your employer, when you quit your job, you won't be able to contribute to it anymore. But the money already in the account is still yours, and it can usually just stay put in that account for as long as you want with a couple of exceptions.

The amount of cash that's in the fund when you retire is what you will receive as a pension. Thus, there is no guarantee that you will receive anything from this defined-contribution plan. The fund may lose all (or a substantial part) of its value in the markets just as you're ready to start taking distributions.

If you already have a 401(k) and want to check the balance, it's pretty easy. You should receive statements on your account either on paper or electronically. If not, talk to the Human Resources department at your job and ask who the provider is and how to access your account.

Also, 401(k) money is protected from creditors in the event you had to file for personal bankruptcy, and by cashing it out, you will lose this protection. 1feff You will also be eroding your nest egg and would be better off using an IRA rollover or making a transfer to a new 401(k) plan instead of cashing in this money.