Notice to Debt Collector - Falsely Representing Dire Consequences for Nonpayment of a Debt

What this document covers

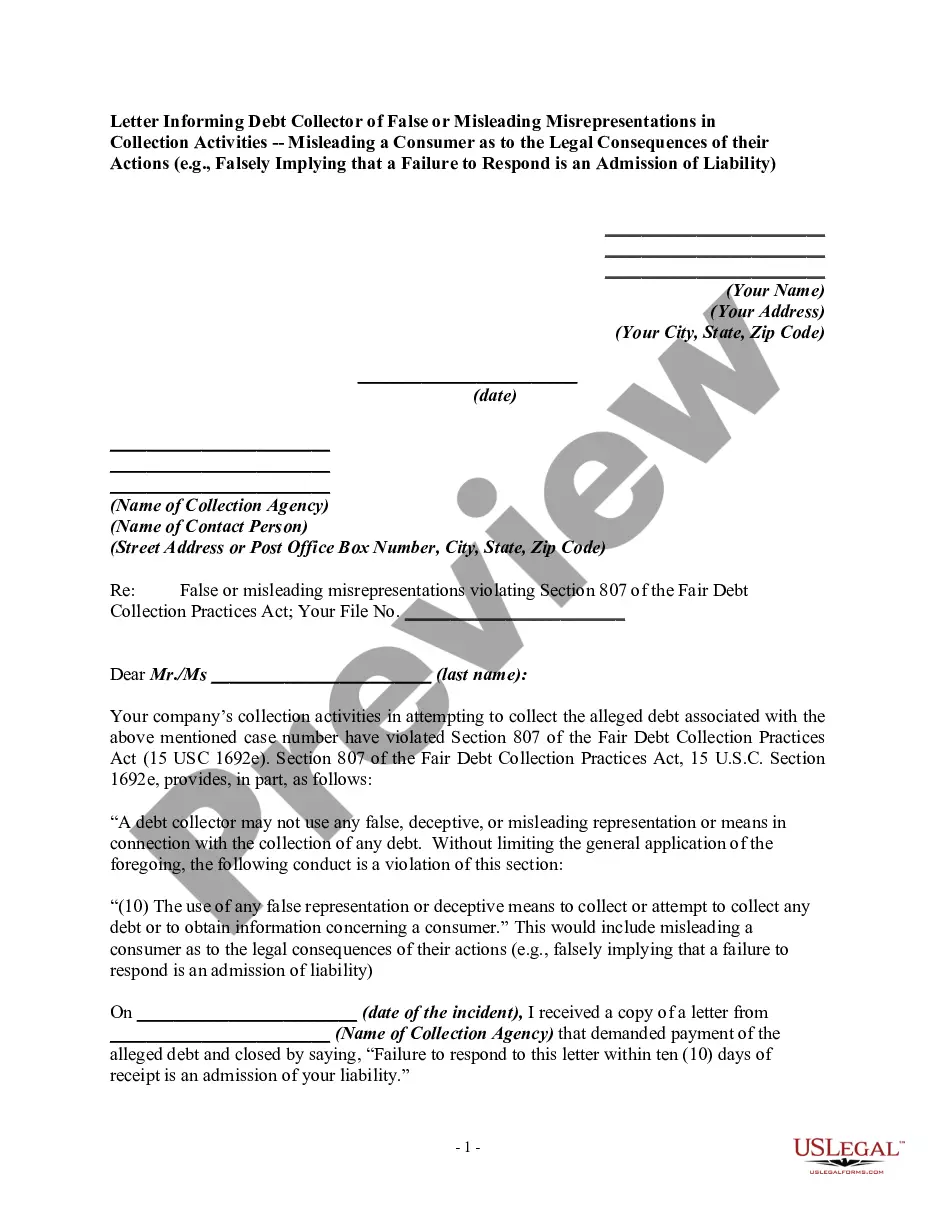

The Notice to Debt Collector - Falsely Representing Dire Consequences for Nonpayment of a Debt is a formal document used by consumers to notify debt collectors of violations under the Fair Debt Collection Practices Act (FDCPA). This form helps assert consumer rights by pointing out deceptive practices related to debt collection, including false statements about dire legal or financial consequences of nonpayment. Unlike other debt-related letters, this specific notice addresses intentional misrepresentation by debt collectors, strengthening the consumer's position in disputes.

What’s included in this form

- Consumer Information: Includes the name and contact details of the debtor.

- Debt Collector Information: Contains the name and address of the debt collection company.

- Violation Description: A section to describe how the debt collector violated the FDCPA.

- Second Notice Clause: An option to indicate prior violation notices have been sent.

- Signature Line: For the consumer to sign and date the notice.

Common use cases

This form should be used when a consumer believes a debt collector has made false or misleading representations about the consequences of not paying a debt. For example, if a debt collector threatens arrest or legal action that is not permissible, this form acts to formally notify the collector of their violation. It is also useful if there have been multiple instances of such misconduct and the consumer wishes to take further action.

Who this form is for

- Consumers who have been contacted by debt collectors.

- Individuals who believe their rights have been violated under the FDCPA.

- Anyone facing harassment or misleading threats from debt collection agencies.

Completing this form step by step

- Fill in your name and address at the top of the form.

- Enter the debt collector's name and address in the designated section.

- Clearly describe the violations committed by the debt collector.

- If applicable, indicate whether this is a first or second notice of violation.

- Sign and date the form before sending it.

- Send the completed notice via certified mail to ensure delivery confirmation.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include specific details of the violation.

- Not sending the notice via certified mail.

- Neglecting to keep copies of all correspondence with the debt collector.

- Assuming a single notice is sufficient for ongoing violations.

Advantages of online completion

- Convenience of immediate download and access from any device.

- Editability allows you to tailor the content to your specific situation.

- Access to legally vetted templates crafted by licensed attorneys.

Legal use & context

- This form serves as a formal notice under the FDCPA and can help establish a paper trail for legal purposes.

- Use of this form is a proactive step in protecting consumer rights against unlawful debt collection practices.

What to keep in mind

- This form helps consumers formally address violations of the Fair Debt Collection Practices Act.

- Provide detailed examples of the violations when completing the form.

- Always send the notice via certified mail for proof of delivery and record-keeping.

Looking for another form?

Form popularity

FAQ

You may be able to sue a creditor or credit reporting agency if there is wrong information on your credit report that is not being removed.

You have the right to force the debt collector to prove you owe the money. Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

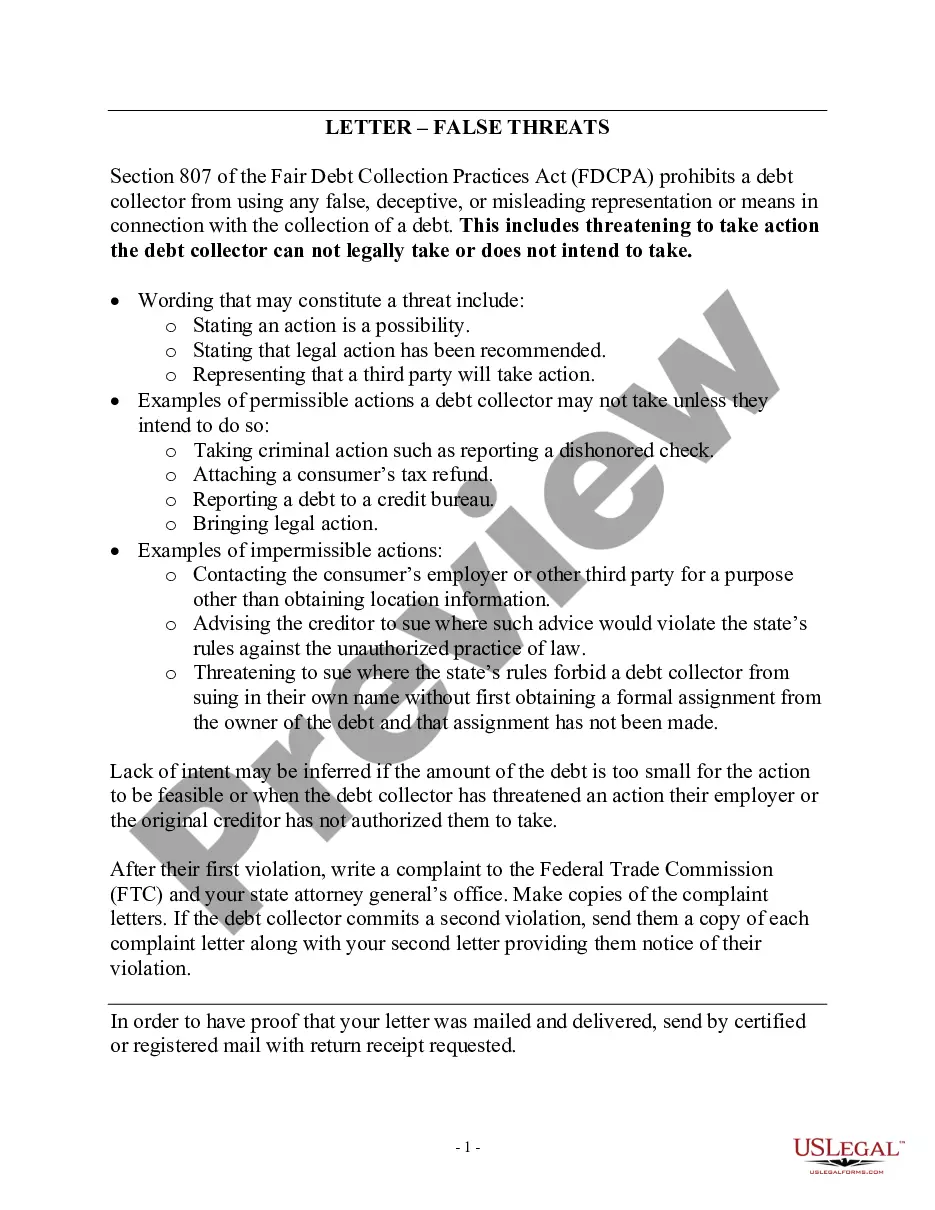

For example, they can't: misrepresent the amount you owe. lie about being attorneys or government representatives. falsely claim you'll be arrested, or claim legal action will be taken against you if it's not true.

Sue the Debt Collector in State Court The consumer may bring a lawsuit against the debt collector in state court. In the lawsuit, you must prove that the debt collector violated the FDCPA. If successful, you may be able to collect $1,000 in statutory damages, and possibly more if you suffered harm from the violations.

If the debt holder still doesn't pay whomever is collecting the debt, the creditor can file a lawsuit against the debt holder in civil court. However, the creditor is less likely to do so if the balance owed is under $1,000, or if the debt is settled.

You have the right to sue the collection agency if they act improperly for one year from the improper action. You can sue for lost wages and other expenses incurred, including legal and court costs. Also, the judge is allowed to award you up to $1,000 in punitive damages.

You received a letter in the mail. The agency is licensed in your state. The collector can verify your personal details. You can request information about the debt. There's more than one method of payment. A company works with you, not against you.

Debt collectors using fake summons to entrap their consumers will typically issue fake summonses with limited legal language or terminology (if any at all). To verify legitimacy within a court summons, look for any type of confirmation of pending actions that exist between the various parties involved.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.