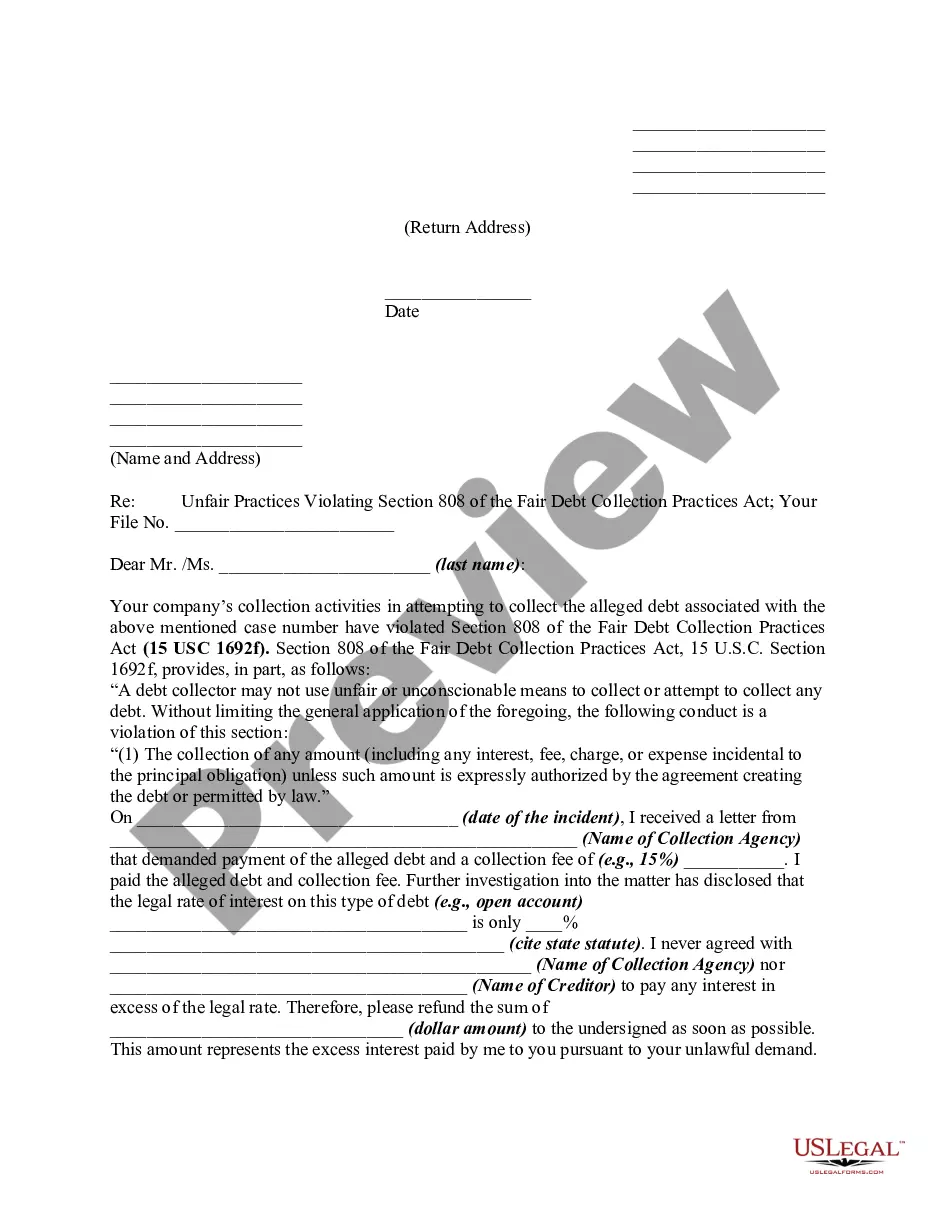

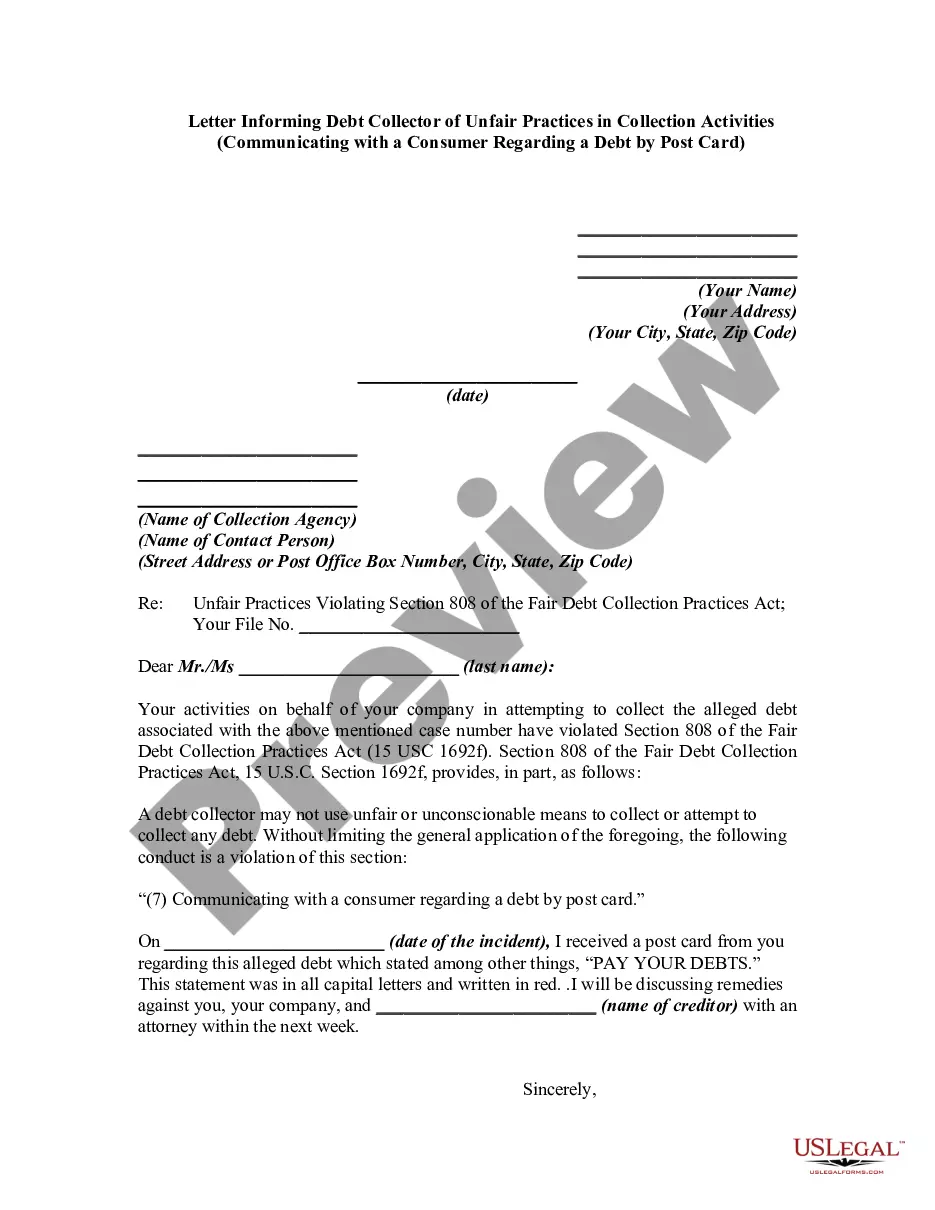

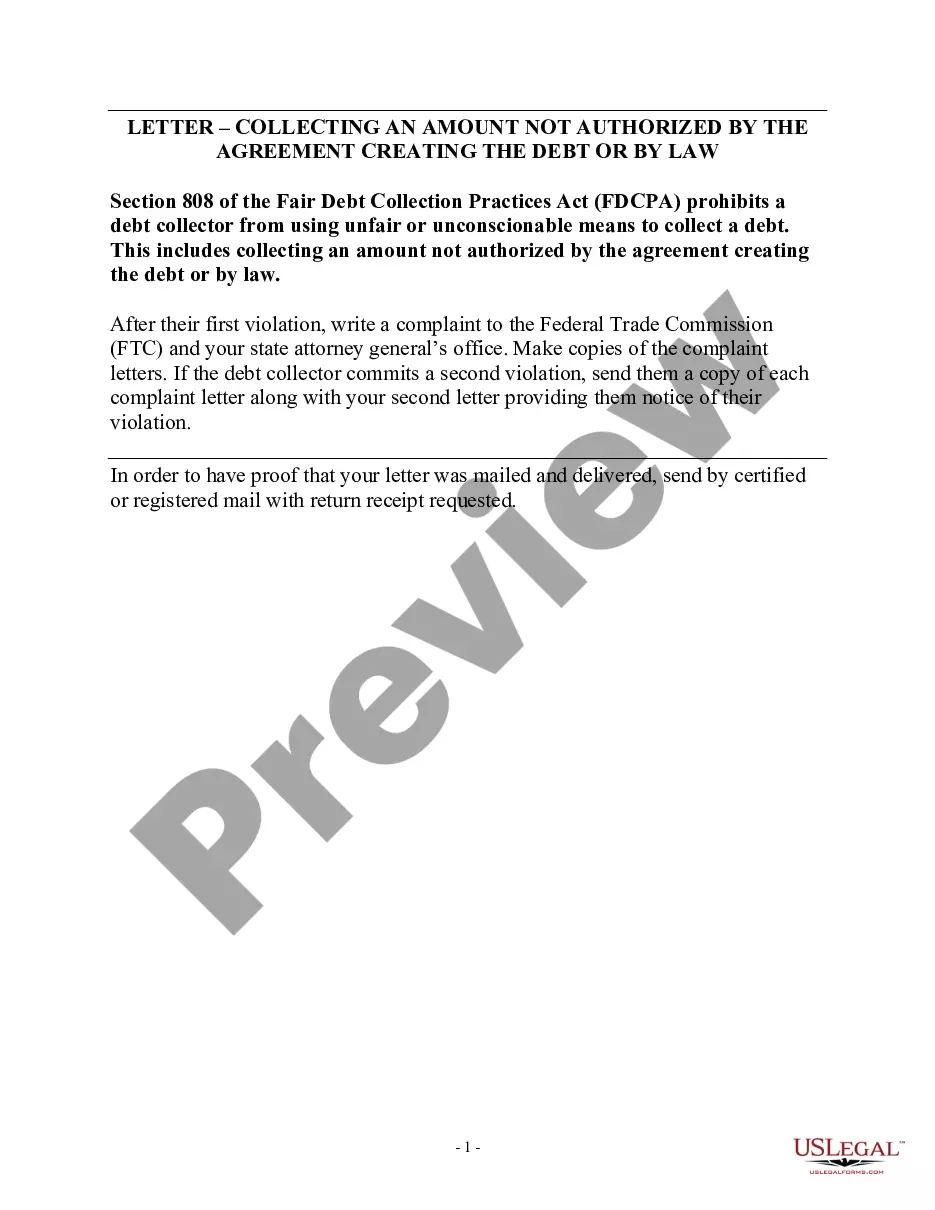

Letter Informing Debt Collector of Unfair Practices in Collection Activities - Collecting an Amount not Authorized by the Agreement Creating the Debt or by Law

What is this form?

This form is a Letter Informing Debt Collector of Unfair Practices in Collection Activities. It is designed to formally notify a debt collector when they attempt to collect amounts that are not authorized by the original agreement or by law, as specified in Section 808 of the Fair Debt Collection Practices Act. By using this form, you can address unfair practices and seek a refund for excess charges, which can help you assert your rights effectively.

Main sections of this form

- Your personal information, including name and address.

- The date of the letter to the collection agency.

- Details of the collection agency and the specific contact person.

- The reference number related to the disputed debt.

- A description of unfair practices encountered during the collection of the debt.

- A request for a refund of excess payments made beyond what is legally owed.

Common use cases

You should use this letter when a debt collector has charged you more than what you are legally required to pay or has imposed fees that were not part of your original agreement. This form serves to document your claim and ensures you communicate clearly with the debt collector about the illegitimacy of their practices.

Intended users of this form

- Anyone who has received a demand for payment from a debt collector.

- Individuals who believe they have been charged unfair fees or amounts.

- Consumers who want to formally assert their rights under the Fair Debt Collection Practices Act.

- Debtors looking to recover amounts paid in excess of legal limits.

How to complete this form

- Enter your name and address at the top of the letter.

- Fill in the date when you are sending the letter.

- Provide the debt collector's name and contact person, if known.

- Indicate your file number associated with the debt.

- Clearly explain the unfair practices observed and the unauthorized amounts demanded.

- Request a refund for any excess amounts you mistakenly paid.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Not providing accurate information about the debt or the collection agency.

- Failing to include the specific date and details about the unfair practices.

- Not requesting a specific amount as a refund.

- Using vague language that does not clearly explain your violation claims.

Benefits of completing this form online

- Convenience of accessing the form anytime and from anywhere.

- Editability allows for quick customization to fit your specific situation.

- Reliable templates drafted by licensed attorneys enhance your legal communication.

- Immediate download saves time compared to traditional paper forms.

Legal use & context

- This form is enforceable under the Fair Debt Collection Practices Act.

- Documenting unfair practices may strengthen your case should you need to escalate the matter.

- Using this letter helps to formalize your complaint, ensuring it is taken seriously by the collection agency.

What to keep in mind

- This letter addresses unfair debt collection practices.

- It requests reimbursement for any excess fees charged.

- Clarifies your rights under federal law, providing a clear structure for your grievance.

Looking for another form?

Form popularity

FAQ

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

Know Your Rights! RIGHT TO DISPUTE THE DEBT: Within 30 DAYS of receiving notice of the debt from the debt collector, you can send a letter to the debt collector disputing the debt and requesting the name and contact information of the original creditor.

Your full name and address. The collections agency's name and address. A request for the amount of the debt claimed to be owed. A request for the name of the original creditor. A request for the judgment information (if applicable) A request for proof of the company's license.

Step 1: Keep detailed records of what the debt collector is doing. Step 2: Take action write to the debt collector, complain to an External Dispute Resolution scheme (Ombudsman Service) or VCAT. Step 3: Complain to a Regulator.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

Dispute the error with the credit bureau. Report the collections account and ask to have it removed from your credit report. 2feff Provide copies of any evidence you have proving the debt doesn't belong to you. Even if the debt belongs to you, that doesn't mean the collector is legally able to collect from you.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.