Second Notice to Debt Collector of False or Misleading Misrepresentations in Collection Activities - Failure to Disclose to Debtor in Subsequent Communication that Letter Requesting Information Regarding Alleged Debt was from a Debt Collector

What this document covers

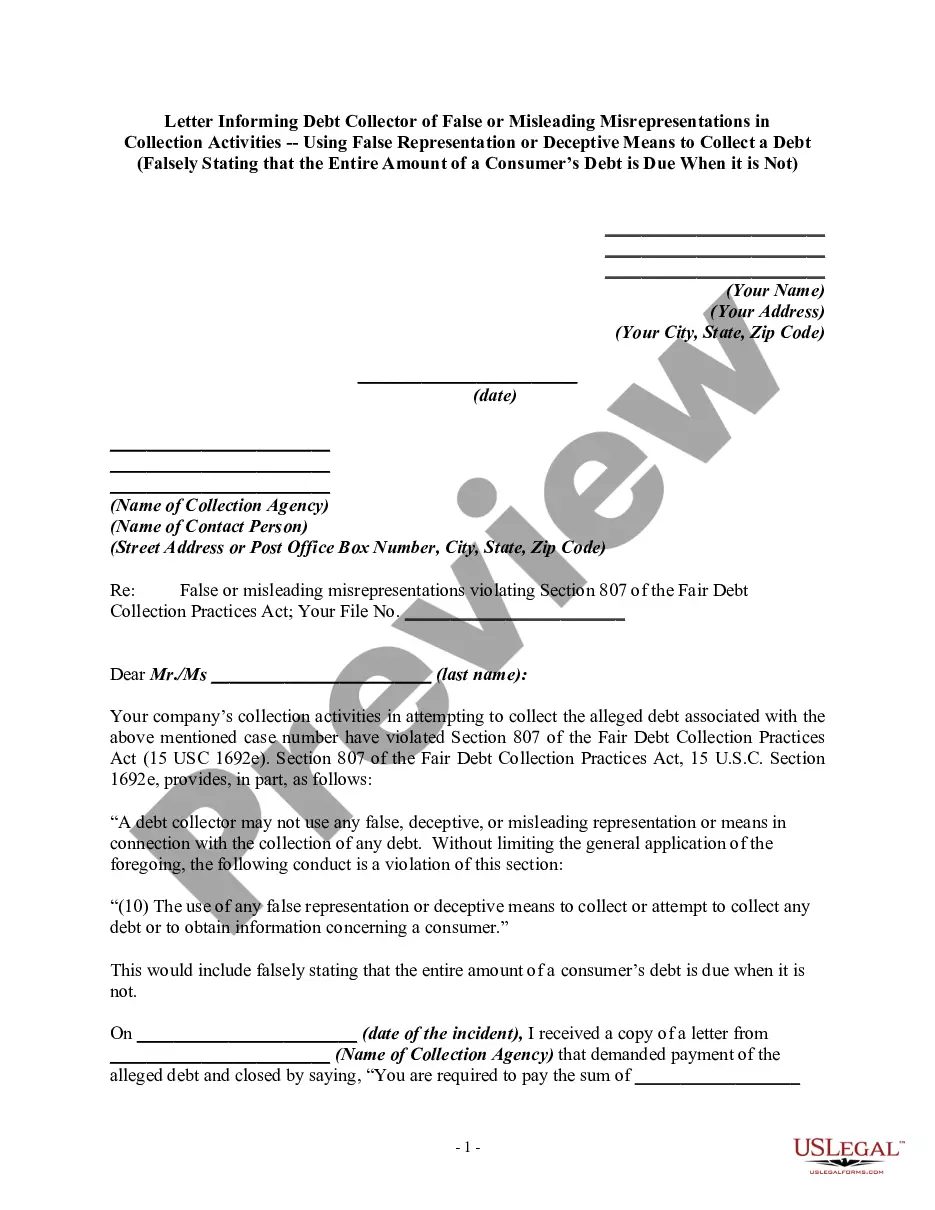

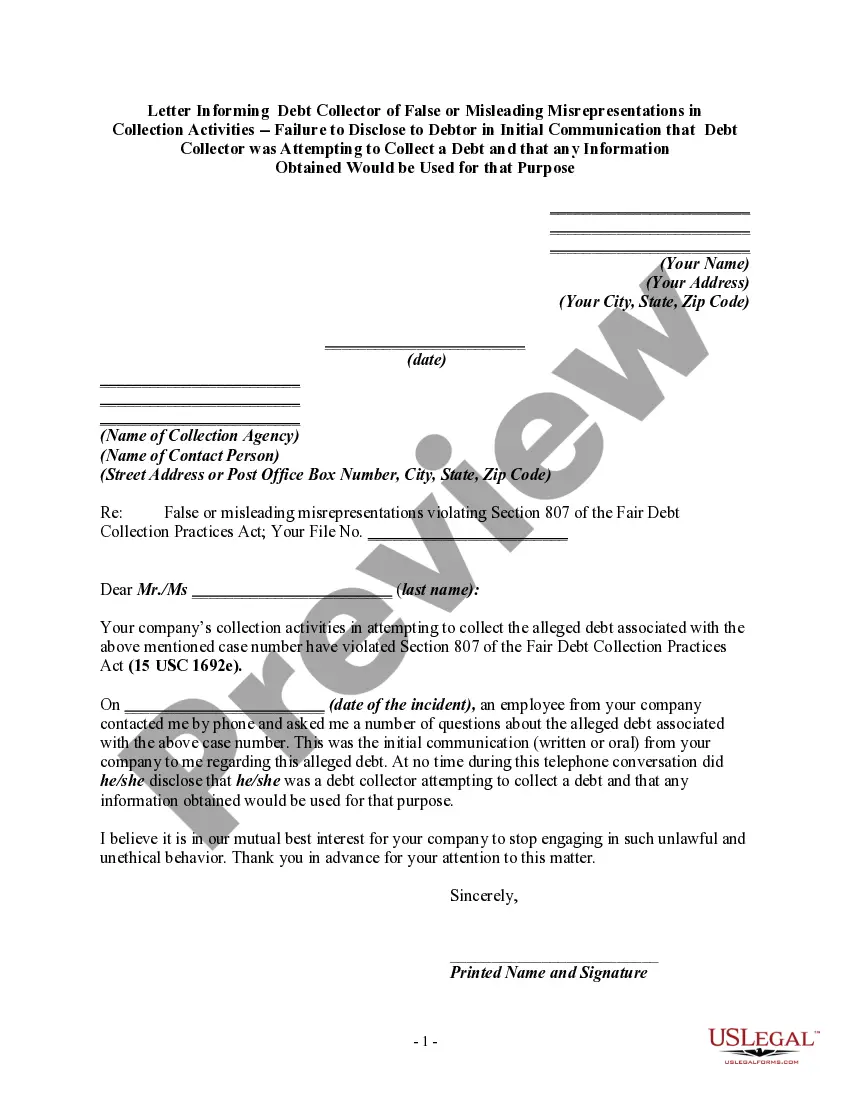

The Second Notice to Debt Collector of False or Misleading Misrepresentations in Collection Activities serves to formally inform a debt collector that they have failed to disclose that they are attempting to collect a debt. This notice is issued under the provisions of the Fair Debt Collection Practices Act (FDCPA) and highlights any misrepresentations in prior communication. This form distinguishes itself from other collection-related notices by focusing specifically on deceptive practices regarding disclosure.

Key components of this form

- Your contact information: Name, address, and date.

- Collector's information: Name of the collection agency, contact person, and their address.

- Allegation specifics: Reference to the alleged debt and past communication dates.

- Description of the violation: Explanation of how the collector failed to disclose their status as a debt collector.

- Statement of intent: Notice of rights under the FDCPA to seek damages for deceptive practices.

When this form is needed

This form should be used when you have previously communicated with a debt collector who has failed to identify themselves as such in either written or oral communications. If you believe that their actions violate the FDCPA and you wish to formally document this issue, sending this second notice can help assert your rights as a consumer.

Who this form is for

- Individuals dealing with debt collection agencies who believe they are being misled.

- Consumers seeking to protect their rights under the Fair Debt Collection Practices Act.

- Anyone who has received misleading communications regarding a debt they allegedly owe.

Instructions for completing this form

- Fill in your name and address at the top of the form.

- Enter the date you are sending the notice.

- Provide the name of the collection agency and the contact person.

- Specify the date of the previous communication and the date of the letter received.

- Clearly outline how the previous correspondence failed to disclose that it was from a debt collector.

- Sign the form to validate your claim.

Notarization guidance

This form does not typically require notarization unless specified by local law. Ensure that you comply with any local requirements to strengthen your notice.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include complete contact information can delay the response.

- Not specifying the dates clearly can lead to confusion for the debt collector.

- Using vague language that does not clearly state the nature of the violation.

Why complete this form online

- Convenient access to legal templates that can be filled out and downloaded immediately.

- Edit the template as needed to customize your message for your situation.

- Reliable legal formatting to ensure compliance with legal standards.

Legal use & context

- This form can help consumers assert their rights under the FDCPA.

- It serves as a documented notice of misrepresentation, which may be used as evidence in any disputes.

- Failure to respond to this notice by the collector may strengthen your claim against them for non-compliance.

Key takeaways

- Utilize this form to formally notify debt collectors of misleading communication.

- Be clear and concise in your claims to avoid potential confusion.

- Understand your rights and the provisions of the FDCPA to protect yourself as a consumer.

Looking for another form?

Form popularity

FAQ

Sue the Debt Collector in State Court. Sue the Creditor in Small Claims Court. Report the Action to a Government Agency. Report the Action to the State Attorney General. Use the Violation as Leverage in Debt Settlement Negotiations.

Sue the Debt Collector in State Court. Sue the Creditor in Small Claims Court. Report the Action to a Government Agency. Report the Action to the State Attorney General. Use the Violation as Leverage in Debt Settlement Negotiations.

Harassment of the debtor by the creditor More than 40 percent of all reported FDCPA violations involved incessant phone calls in an attempt to harass the debtor.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

You have the right to sue the collection agency if they act improperly for one year from the improper action. You can sue for lost wages and other expenses incurred, including legal and court costs. Also, the judge is allowed to award you up to $1,000 in punitive damages.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.The court might also order the debt collector to stop engaging in certain collection activities.

No. Debt collectors are prohibited from deceiving or misleading you while trying to collect a debt. Debt collectors are generally prohibited under federal law from using any false, deceptive, or misleading misrepresentation in collecting a debt.

You should first write to the company or debt collection agency in question expressing your complaint. If they do not adequately resolve the issue you may be able to take your complaint to the Financial Ombudsman Service.

Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing. Dispute the debt on your credit report. Lodge a complaint. Respond to a lawsuit. Hire an attorney.