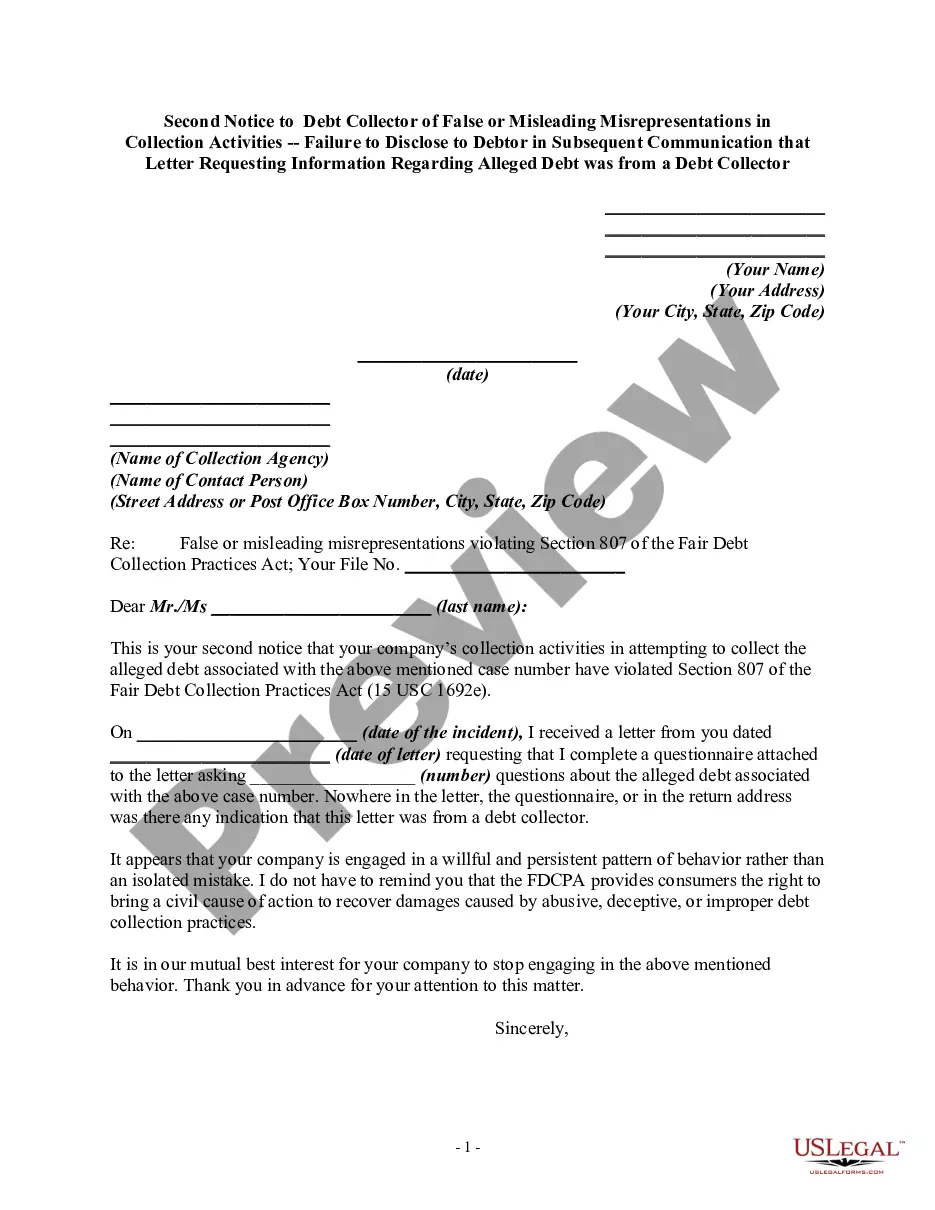

Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor

What this document covers

This form, known as the Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or Other Criminal Means to Harm, serves as an official follow-up communication to a debt collector. It warns that their actions may be in violation of the Fair Debt Collection Practices Act (FDCPA) and that further harassment could result in legal action against them. This form is crucial for ensuring your rights are protected in the face of aggressive debt collection practices.

Key parts of this document

- Your personal information, including name and address.

- Details of the debt collector, including their agency name and contact person.

- Description of the harassment or abusive behavior experienced.

- Specific reference to Section 806 of the FDCPA.

- A statement outlining potential legal action.

- Your signature and printed name to validate the notice.

When this form is needed

You should use this form if you have experienced continued harassment from a debt collector despite previous warnings or notices. If you feel threatened or if the collector has made comments indicating they might use violence or criminal means, this form is an important step to formally document the behavior and seek resolution.

Who can use this document

- Consumers facing ongoing harassment from debt collectors.

- Individuals who previously communicated with a debt collector and received no relief.

- Any debtor who wishes to assert their rights under the FDCPA following threats or abusive practices.

How to complete this form

- Enter your name and address at the top of the form.

- Provide the date when you are sending the notice.

- Include the name of the collection agency and the contact person responsible for your case.

- Describe the abusive behavior in detail, including the date it occurred and the name of the employee involved.

- Sign and print your name at the end of the letter to validate it.

Notarization guidance

This form does not typically require notarization unless specified by local law. It is sufficient to complete the form and send it directly to the debt collector.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the date of abusive incidents.

- Not providing enough detail about the nature of the harassment.

- Omitting signature, which could invalidate the notice.

- Sending the notice without keeping a copy for personal records.

Why complete this form online

- Immediate access to a legally sound template drafted by licensed attorneys.

- Editable format allows you to personalize your information easily.

- Convenient download option provides a ready-to-use document.

- Informed support to guide you through the process of asserting your rights.

Key takeaways

- This form is essential for documenting repeated harassment from debt collectors.

- Completing this notice provides a formal warning and potential for legal action if abuse continues.

- Ensure all details are accurate and legible to avoid complications.

Looking for another form?

Form popularity

FAQ

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

The Fair Debt Collection Practices Act (FDCPA) is the main federal law that governs debt collection practices. The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

When a Debt Collector Calls, How Should You Answer? The phone call from a debt collector never comes at a good timebut the best response is to confront the state of these affairs head-on. You may want to hide or ignore the situation and hope it goes awaybut that can make things worse.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Refused Offers A creditor isn't required to negotiate a settlement offer with a debtor, according to the Federal Trade Commission, but does so at its own discretion. This applies to a collection agency as well.The agency can choose to refuse your settlement offer and instead request payment of the debt in full.