Proposed issuance of common stock

Understanding this form

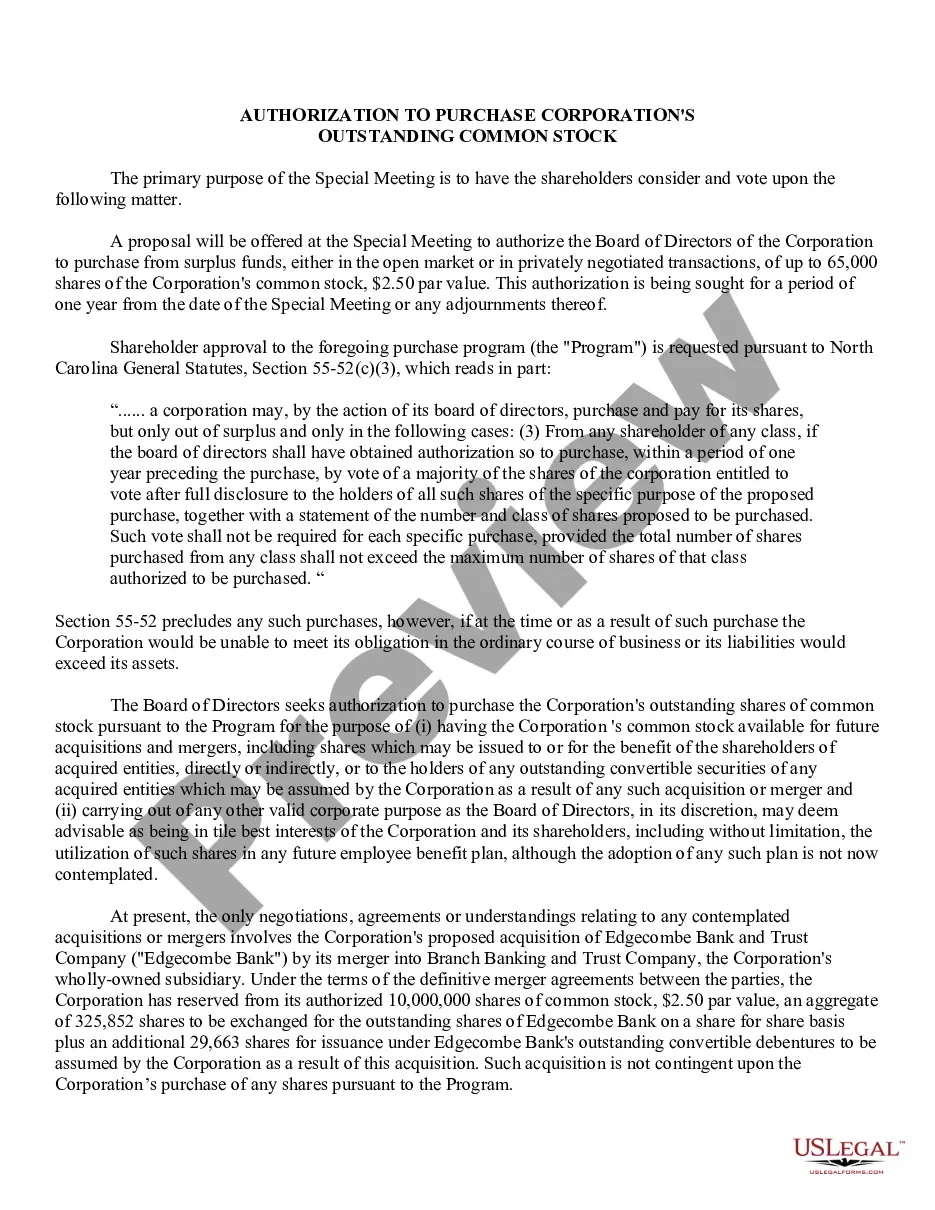

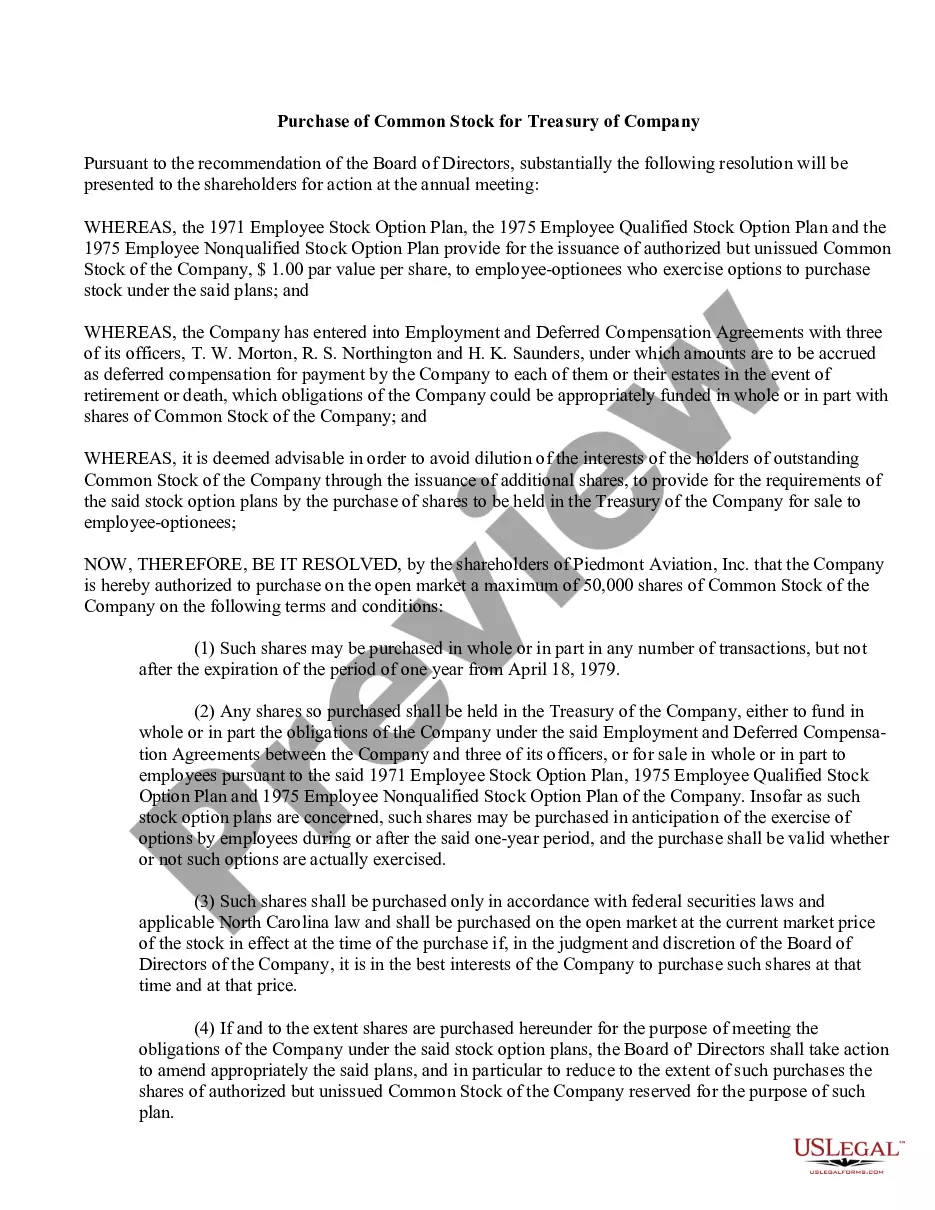

The Proposed Issuance of Common Stock form is a legal document used by companies to seek stockholder approval for the issuance of additional shares of common stock. This form is essential during corporate governance, particularly when a company plans to restructure its debt or raise equity capital. It outlines the reasons for the proposed issuance and details the terms of the proposed exchange transaction, helping stockholders to understand the implications of their vote.

Key components of this form

- Introduction and recommendation from the Board of Directors.

- Details of the existing debentures and their interest costs.

- Proposed issuance and terms of up to 3,000,000 shares of common stock.

- Exchange transaction specifics, including conversion options for existing debentures.

- Voting requirements and conditions under New York Stock Exchange guidelines.

- Potential financial impact and rationale for the issuance.

When this form is needed

This form is used when a corporation plans to issue additional shares of common stock, particularly in an exchange transaction involving existing debt. It is necessary when the company seeks to reduce its financial obligations or to raise more equity capital to enhance its financial health. If your company has existing debentures that you wish to retire or convert into equity, this form is indispensable for formalizing the proposal before shareholders.

Who this form is for

- C-Levels or executives within the company responsible for corporate governance.

- Members of the Board of Directors looking to recommend a stock issuance.

- Shareholders seeking to understand and vote on capital restructuring proposals.

- Legal counsel assisting with the issuance process and compliance requirements.

Steps to complete this form

- Begin with the introduction, stating the purpose of the proposal.

- Summarize the existing debt situation and the rationale for the new issuance.

- Specify the number of shares to be issued and the terms of the exchange transaction.

- Provide background information on the impact of the proposed changes on the company's financial position.

- Outline the voting requirements and necessary approvals from shareholders.

- Finalize the document with the date and signatures of involved parties.

Does this document require notarization?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly explain the reasons for the stock issuance.

- Not including all required terms of the exchange transaction.

- Overlooking state-specific filing requirements or regulations.

- Neglecting to obtain proper board approvals before presenting to shareholders.

Benefits of completing this form online

- Quick access to a legally drafted document tailored for corporate needs.

- Ability to customize language to suit your specific situation.

- Convenience of obtaining the form instantly without needing to visit an office.

- Reliability of using templates created by licensed attorneys.

Legal use & context

- This form is vital for compliance with corporate law requirements regarding stock issuance.

- It ensures transparency in capital restructuring efforts, promoting shareholder trust.

- Utilizing this form can help prevent legal complications regarding improper issuance of shares.

Main things to remember

- The Proposed Issuance of Common Stock form is vital for corporate compliance in equity issuance.

- Proper completion helps facilitate restructuring of debts through equity issuance.

- Understanding stockholder and state requirements is crucial for validity.

Looking for another form?

Form popularity

FAQ

A public offering is the sale of equity shares or other financial instruments such as bonds to the public in order to raise capital.The financial instruments offered to the public may include equity stakes, such as common or preferred shares, or other assets that can be traded like bonds.

When a company issues additional shares of stock, it can reduce the value of existing investors' shares and their proportional ownership of the company. This common problem is called dilution.

Generally, a company has two options to account for stock issuance costs: Debit to Paid-in Capital: treats issuance costs as a reduction to paid-in capital in excess of the security's par value.

Stock issuances are public offerings of shares, also known as partial ownership, in a formerly private company in exchange for money. The company then uses this capital for expansion, debt payment or other purposes.

A public offering is the offering of securities of a company or a similar corporation to the public. Generally, the securities are to be listed on a stock exchange.The services of an underwriter are often used to conduct a public offering.

The entry to record the issuance of common stock at a price above par includes a debit to Cash. Cash is increased (debit) by the issue price. The journal entry would also include a credit to both Common Stock (increased) and Paid-In Capital in Excess of Par--Common Stock (increased).

To record the stock purchase, the accountant debits Investment In Company and credits Cash. At the end of each period, the accountant evaluates the value of the investment. If the value declined, the accountant records an entry debiting Impairment of Investment in Company and credits Investment in Company.

It's typically good news for investors, because it means that after having their investment locked up for nine or ten years, they can finally sell it in the public market and get their return!

If you are selling common stock, which is the most frequent scenario, then record a credit into the Common Stock account for the amount of the par value of each share sold, and an additional credit for any additional amounts paid by investors in the Additional Paid-In Capital account.