Executive Director Loan Plan with copy of Promissory Note by Hathaway Instruments, Inc.

Understanding this form

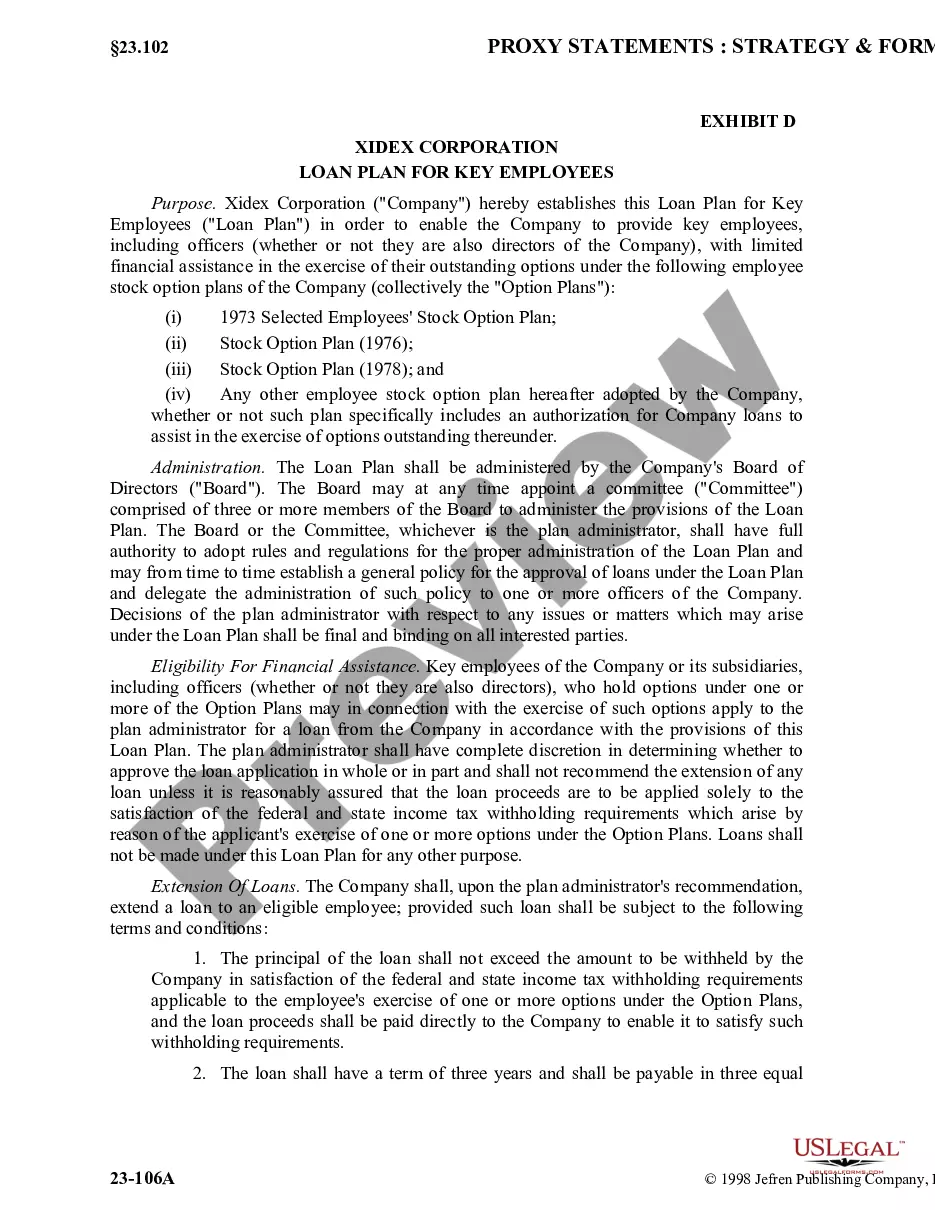

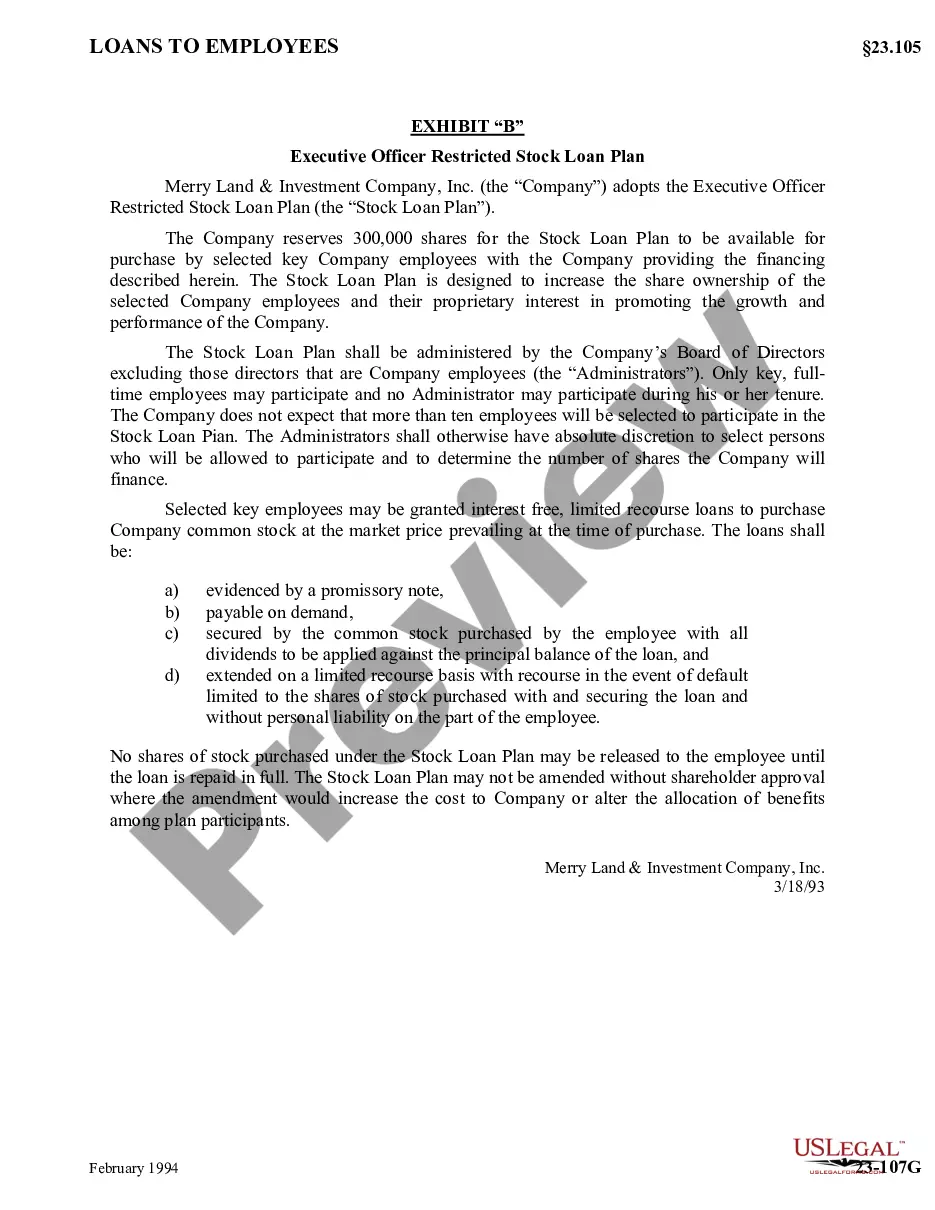

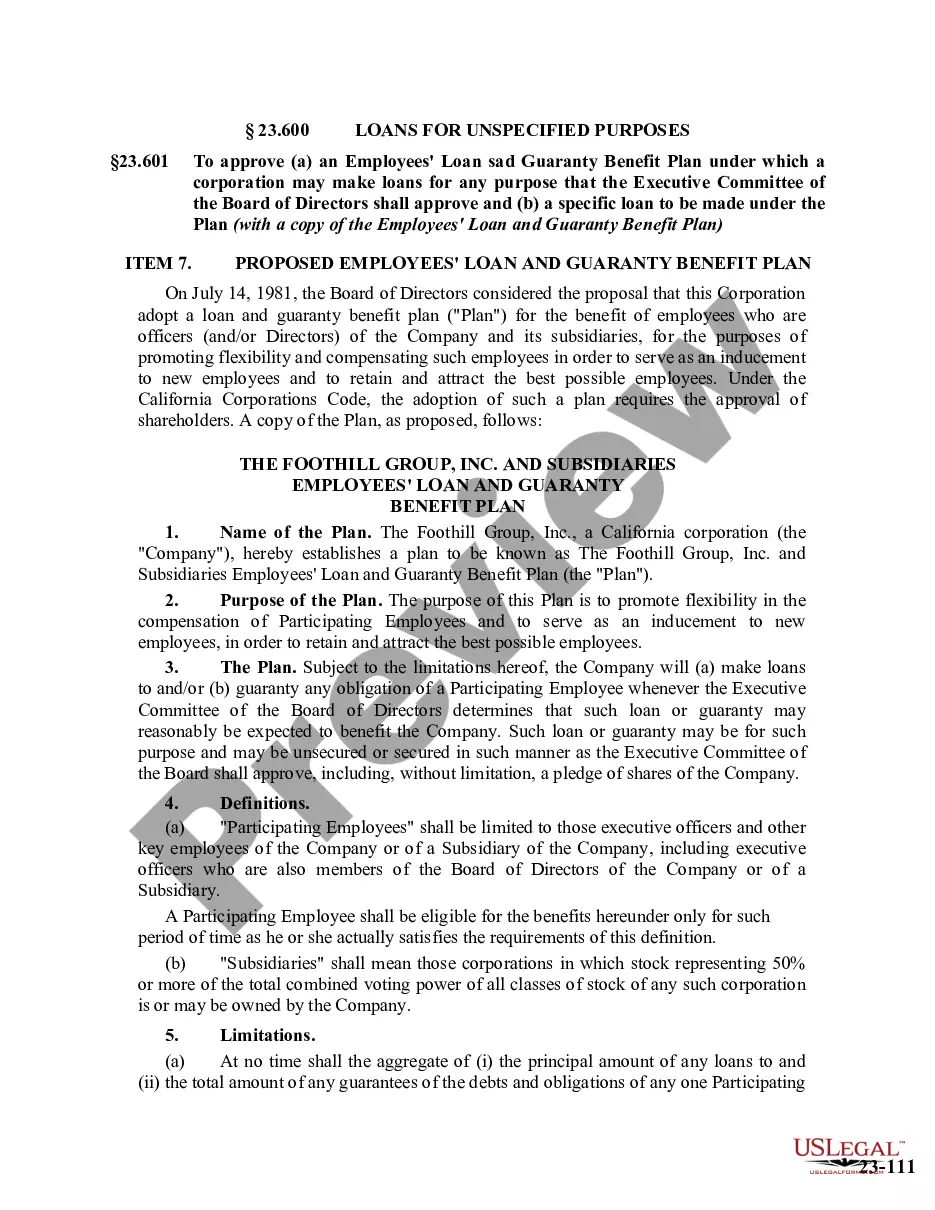

The Executive Director Loan Plan with copy of Promissory Note is a legal template designed for corporations to establish a structured loan program for their executives and directors. This form provides a framework for granting interest-free or low-interest loans as an incentive, distinguishing it from standard loan agreements by its specific focus on corporate leadership. It is useful for organizations looking to enhance their attractiveness to qualified executives while managing loan provisions within corporate governance standards.

What’s included in this form

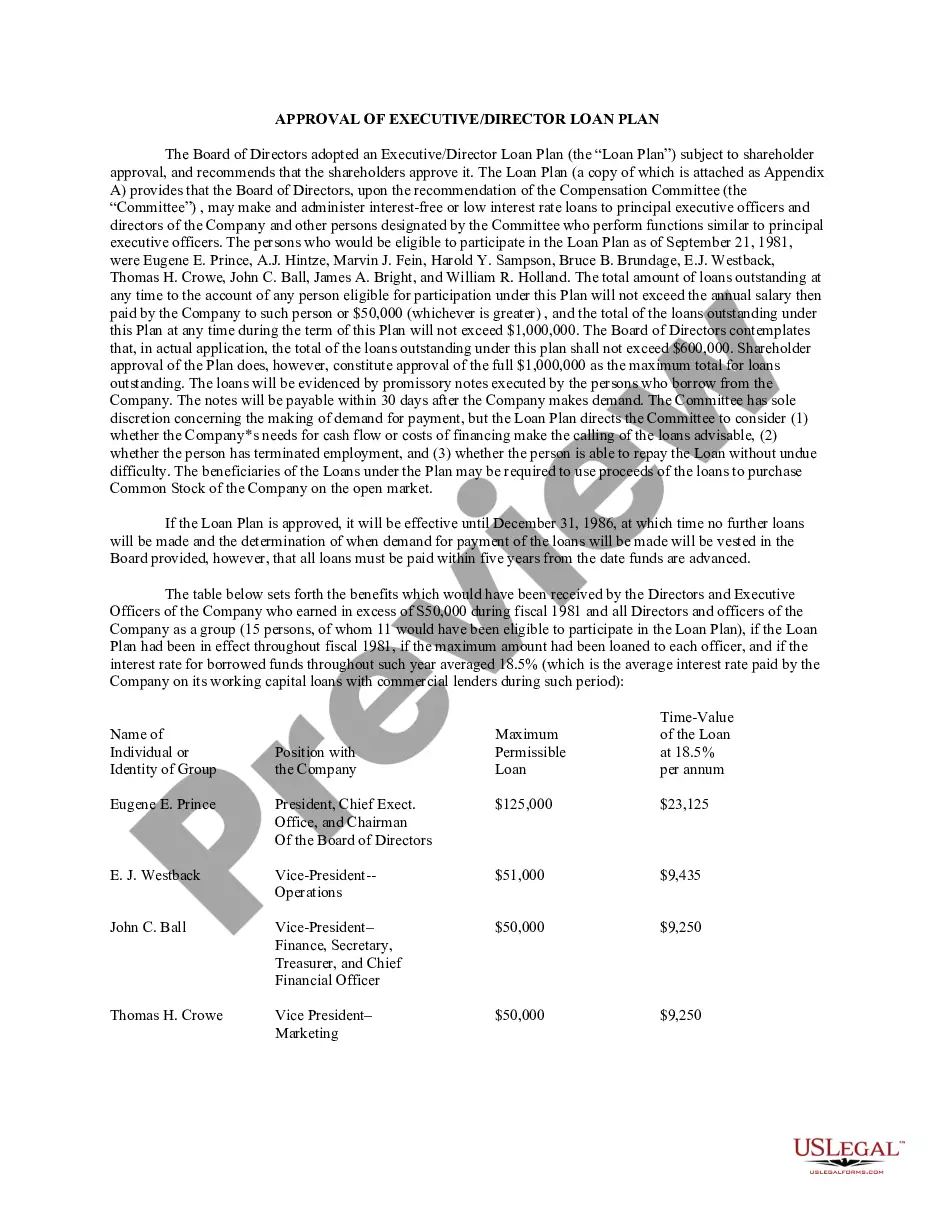

- Objective: Establishes the purpose of the loans as incentives for executives and directors.

- Eligibility: Defines who can participate in the loan program.

- Granting of Loans: Outlines how loans will be recommended and approved by the corporate board.

- Terms of Loans: Specifies loan documentation and payment conditions, including interest rates.

- Limitation on Loans: Describes the maximum loan amounts based on salary and total loan cap.

- Administration: Clarifies the roles of the Board and Committee in managing the plan.

Situations where this form applies

This form is needed when a corporation wants to implement a loan program specifically for its executives and directors. It is particularly useful during recruitment, retention, or as part of an incentive package to address competition from similar entities. If your organization aims to provide financial support while motivating leadership, this loan plan can be a critical resource.

Who this form is for

- Corporate boards of directors looking to attract and retain executive talent.

- Human resources departments implementing executive compensation packages.

- Compensation committees evaluating financial benefit programs for leadership.

How to prepare this document

- Identify the corporate parties involved in the loan plan, including the executives or directors eligible for loans.

- Specify the loan terms, including amount, interest rate, and payment conditions as decided by the Board.

- Ensure the promissory note is attached as an exhibit and complete any necessary documentation.

- Review and gain approval from the Board based on recommendations from the Compensation Committee.

- Communicate the approved loans to the participants and have them execute the promissory note.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly define eligibility criteria, leading to confusion over who can participate.

- Not specifying the repayment terms adequately, which can lead to disputes later on.

- Ignoring state laws that might impose additional requirements on corporate loans.

- Neglecting to obtain board approval for loan grants before issuing the funds.

Benefits of using this form online

- Convenient access: Download and customize the form easily to fit specific corporate needs.

- Editability: Modify the template to reflect unique terms or conditions relevant to your organization.

- Reliable legal framework: Crafted by licensed attorneys, ensuring the form meets applicable legal standards.

What to keep in mind

- The Executive Director Loan Plan serves as a strategic tool for corporations to incentivize leadership.

- Understanding the eligibility and terms of the plan is crucial for effective implementation.

- Proper completion of the form can help prevent common pitfalls associated with corporate loans.

Looking for another form?

Form popularity

FAQ

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Even if a promissory note is lost, the legal obligation to repay the loan remains. The lender has a right to re-establish the note legally as long as it has not sold or transferred the note to another party.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

What is the difference between a Promissory Note and a Loan Agreement? Both contracts evidence a debt owed from the Borrower to the Lender, but the Loan Agreement contains more extensive clauses than the Promissory Note. Further, only the Borrower signs the promissory note while both parties sign a loan agreement.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

A promissory note, in simplest terms, is the acknowledgment of a debt.Even if a promissory note is lost, the legal obligation to repay the loan remains. The lender has a right to re-establish the note legally as long as it has not sold or transferred the note to another party.

The lender can provide copies of the documents signed at closing. If the loan has changed hands, contact the most current servicer for a copy of your mortgage or deed of trust documents. A lender is required under the Federal Servicer Act to provide you copies of your loan documents if you submit a written request.

"A promissory note is enforceable through an ordinary breach of contract claim." In other words, it's not required that the loan be secured; an unsecured loan is still enforceable as long as the promissory note is fully completed. Lender and borrower information.