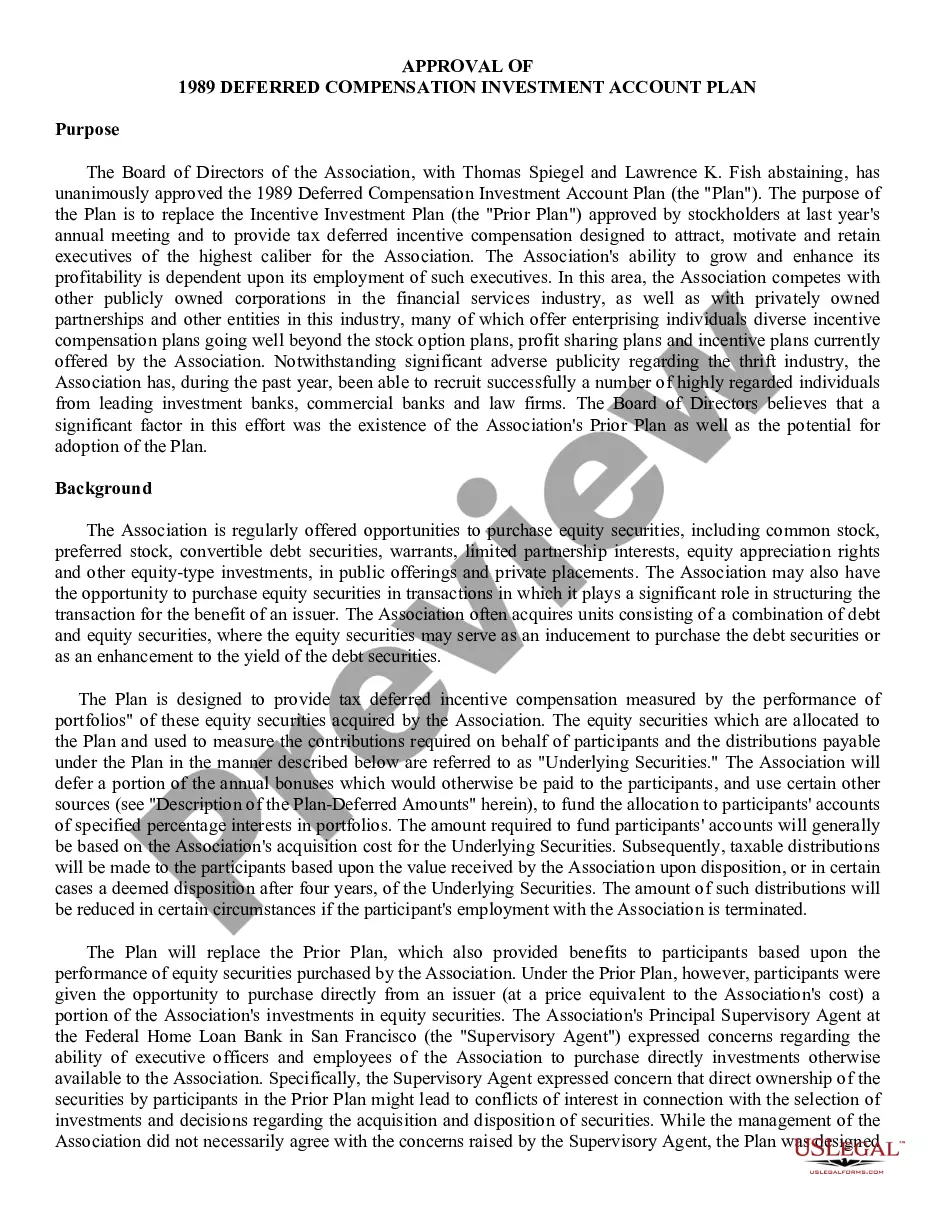

Deferred Compensation Investment Account Plan

About this form

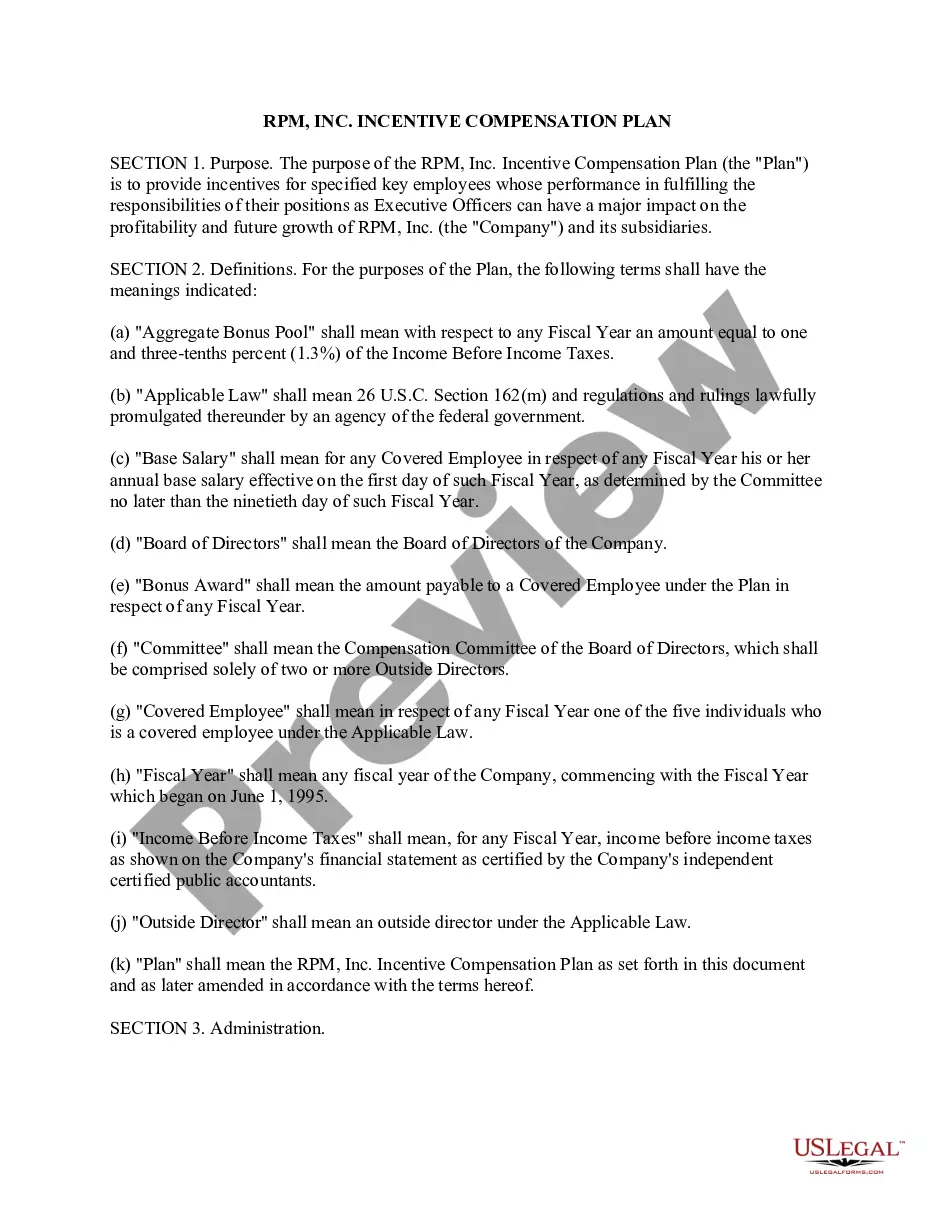

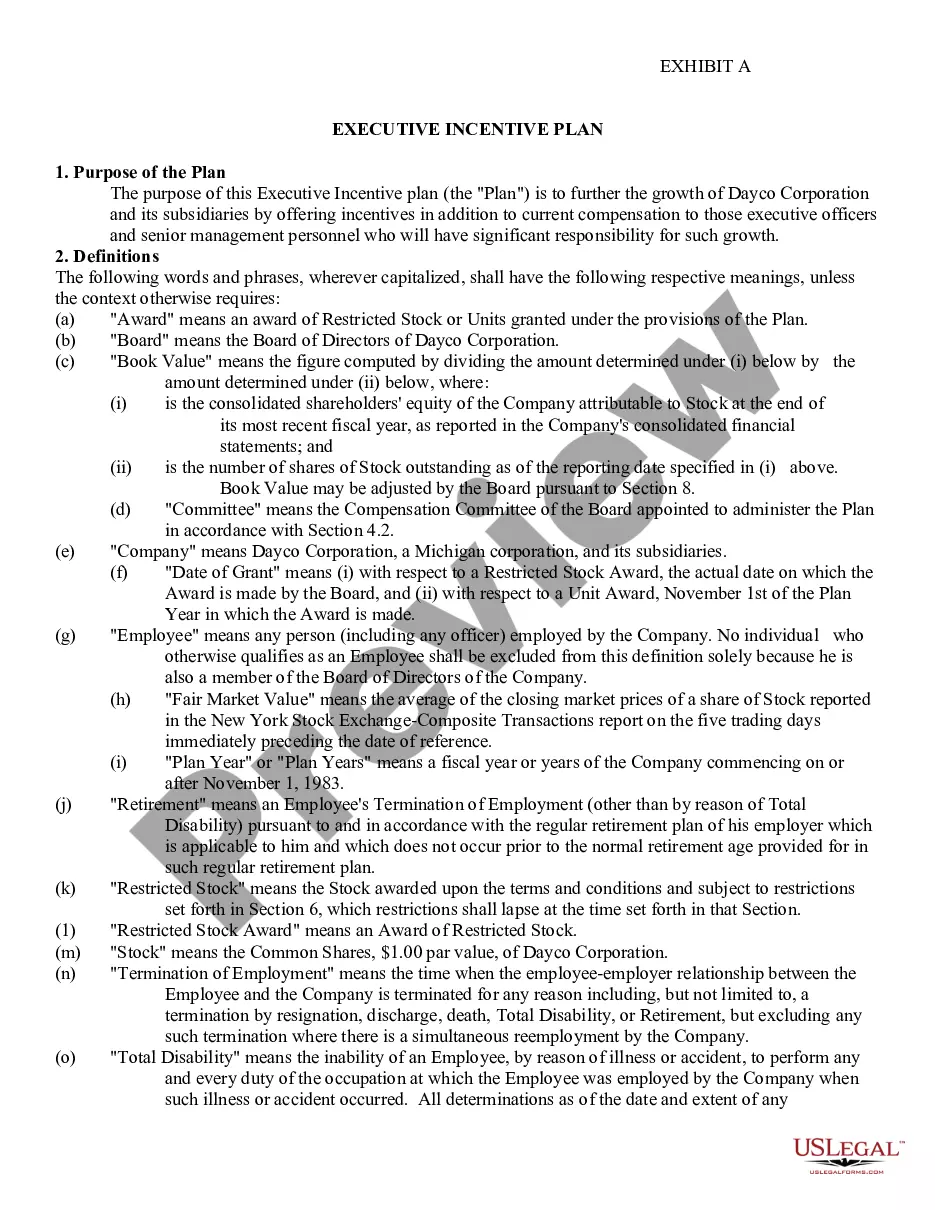

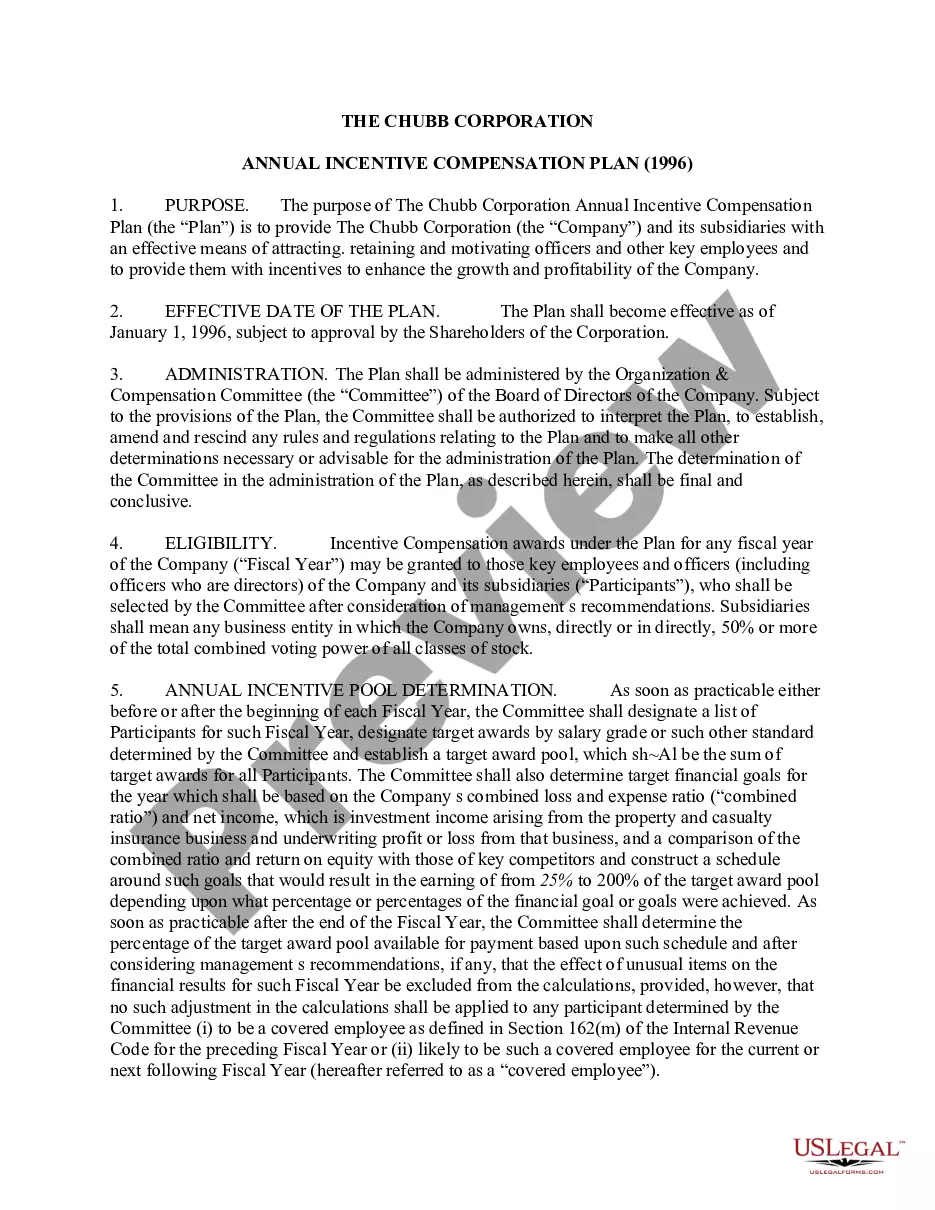

The Deferred Compensation Investment Account Plan is a legal document designed for Savings and Loan Associations to allocate a portion of executive bonuses to a separate investment account. This plan promotes the retention of top executives by linking deferred compensation to the performance of specific equity securities. Unlike other compensation plans, this one allows employees to benefit based on the growth of the Association's investments, providing a long-term financial incentive.

Form components explained

- Purpose: To provide incentives for retaining top executives through deferred compensation.

- Definitions: Key terms such as Account, Deferred Amount, and Distribution are clearly defined.

- Portfolio Composition: Details how the Board of Directors selects the securities for the investment portfolios.

- Distributions: Outlines the mechanics of how and when distributions are made to participants.

- Contribution Sources: Specifies where the deferred amounts come from, including bonus percentages.

When this form is needed

This form is used by Savings and Loan Associations when establishing or updating a Deferred Compensation Investment Account Plan for their executives. It is applicable when an organization seeks to incentivize and retain key leadership through a structured investment plan that directly ties rewards to company performance. This form is also needed during annual meetings where such plans are discussed and approved by the Board of Directors.

Who can use this document

- Members of the Board of Directors for Savings and Loan Associations.

- Executive compensation committees responsible for designing incentive plans.

- Human resources personnel involved in executive compensation policies.

- Senior executives eligible to participate in the compensation plan.

How to complete this form

- Identify the Board members who will oversee the plan.

- Define the specific executive positions eligible for participation.

- Specify the percentage of annual bonuses to be deferred into the plan.

- List the types of portfolios and equity securities that will be included.

- Outline the distribution methods and timelines for payouts to participants.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly define roles for plan administration can lead to confusion.

- Not regularly updating investment portfolios as needed based on performance.

- Inadequately communicating the details of the plan to all eligible participants.

Benefits of using this form online

- Convenience of access and download without the need for physical copies.

- Ability to edit and tailor the form to meet specific organizational needs.

- Reliable and secure certification of the legal document if needed.

Looking for another form?

Form popularity

FAQ

That said, if you are happy with your employer's financial situation, the NG-457 offers good investment options, AND the distribution options are reasonable2026 then this may be a good way to fill the gap before age 59.5 when you can access your 401K/403B.

If you invest in a 457(b) plan, you'll have access to certain advantages like tax-deferred growth and the opportunity to choose how to invest funds. There are also potential disadvantages to keep in mind, including fees that may be higher than other types of investments and no employer match.

Early Withdrawals from a 457 Plan (Notice I said former). By rolling into the IRA, you lose the ability to cash out early to avoid the penalty in case you need access to your funds. There is no penalty for an early withdrawal, but be prepared to pay income tax on any money you withdraw from a 457 plan (at any age).

Deferred compensation plans can be a great savings vehicle, especially for employees who are maximizing their 401(k) contributions and have additional savings for investment, but they also come with lots of strings attached.Like 401(k) plans, participants must elect how to invest their contributions.

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump-sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, retirement plans, and employee stock options.

You can transfer or roll over assets tax-free from your 457 plan to a traditional IRA as often as you want after you leave your job. However, your plan may require you to move your balance to your new employer's 457 if you change jobs.

You Can Max out Both a 457 and a Roth IRA If tax rates are a lot higher when you retire, you will have significantly benefited from your Roth IRA because your withdrawals are tax-free. If tax rates are lower when you retire, your 457 will have been the more tax-efficient account.

To help manage the risk, Mr. Reeves suggested limiting deferred compensation to no more than 10 percent of overall assets, including other retirement accounts, taxable investments and even emergency cash funds. Typically, employees must choose how much to defer and when they would like to receive the payout.

Peter, with that much income, a deferred-compensation plan is definitely worth considering. Unlike a 401(k) or other qualified plan, that $50,000 remains an asset of the company.The plan may allow you to direct the investment of the funds, but it is still technically part of the company's assets.