Waiver of Qualified Joint and Survivor Annuity - QJSA

What this document covers

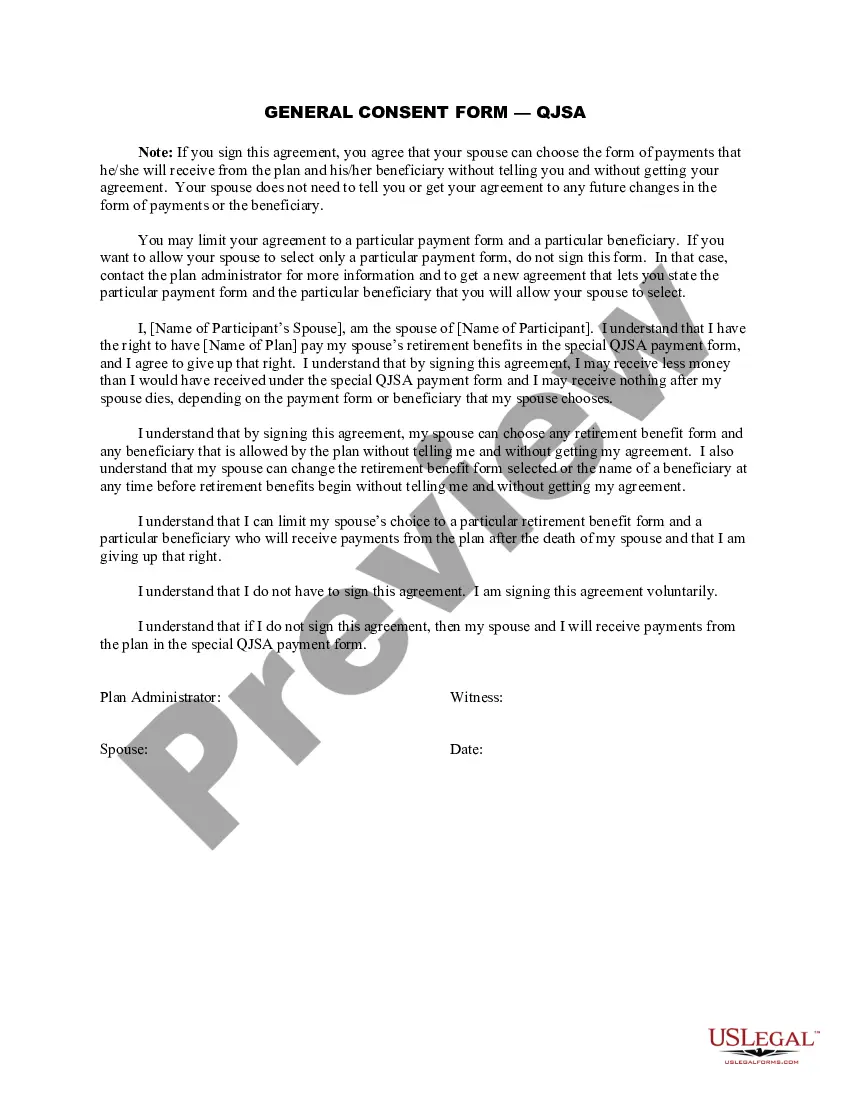

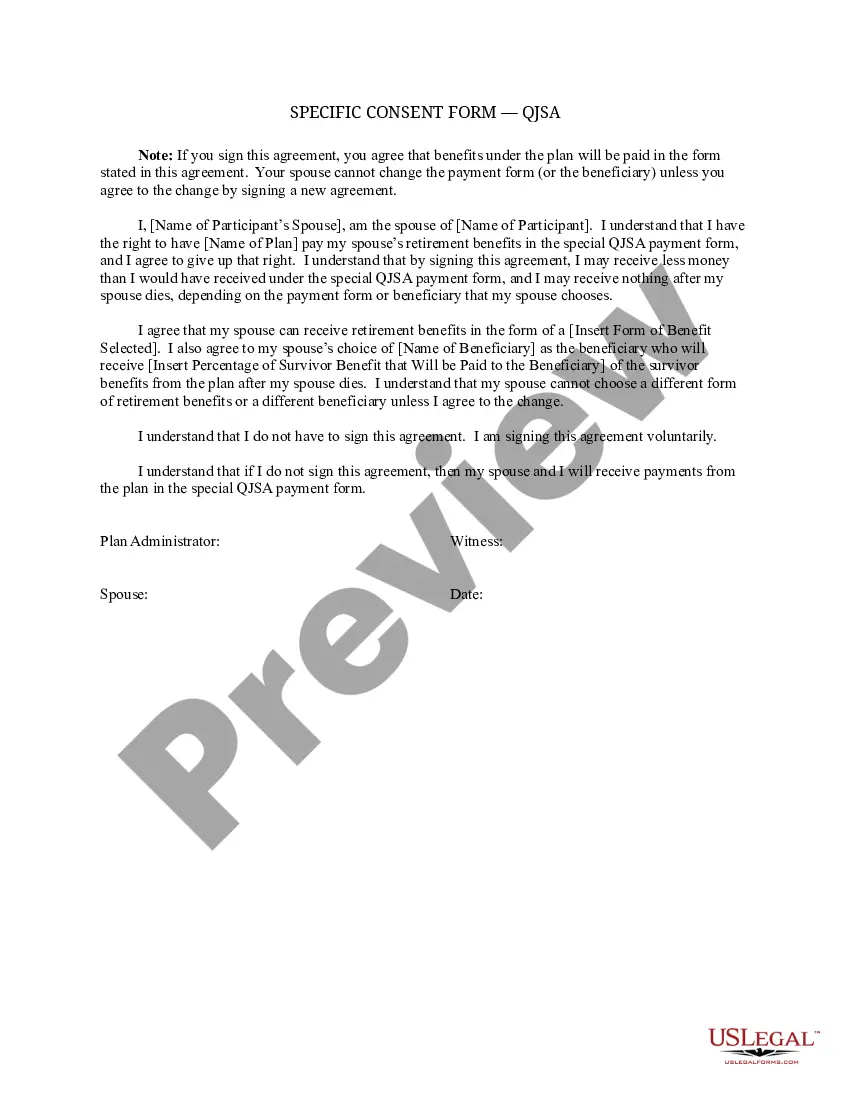

The Waiver of Qualified Joint and Survivor Annuity (QJSA) is a legal document used by retirement plan participants who wish to waive their rights to benefits in the form of a QJSA. This form is crucial for individuals who want to allow their spouses the flexibility to select alternate retirement benefit forms without their agreement. By completing this form, participants can waive both the distribution of plan benefits as a QJSA and the associated notice period, enabling a smoother transition during retirement planning.

Form components explained

- Participant Information: Includes the employer plan number and name.

- Waiver Declaration: A statement where the participant waives the distribution of benefits in the form of a QJSA.

- Spousal Consent: Acknowledgment that the spouse waives rights to be informed about the retirement benefit selections made by the participant.

- Signature Lines: Spaces for the participant's and spouse's signatures and dates of consent.

When to use this form

This form should be submitted no later than 90 days prior to the beginning payment date of the participantâs initial distribution or loan request. You will need this form when you prefer to waive your right to a QJSA, enabling your spouse to choose any retirement benefit form available under the plan independently.

Who should use this form

- Retirement plan participants who wish to waive their rights to a Qualified Joint and Survivor Annuity.

- Individuals planning for retirement who want flexible benefit options for their spouses.

- Spouses of retirement plan participants who desire to understand their rights regarding retirement benefits.

Instructions for completing this form

- Enter your employer plan number and name at the top of the form.

- Read the waiver declaration carefully, then sign to indicate your agreement to waive the QJSA.

- If applicable, have your spouse read the spousal consent section, then sign and date the form.

- Submit the completed form within the required 90-day window before your distribution or loan request.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to submit the form within the 90-day timeframe.

- Not having both parties sign the form, leading to a lack of consent.

- Overlooking to review terms of the waiver, which could affect benefit choices.

Benefits of using this form online

- Convenience of downloading and completing the form at your own pace.

- Editability to fit your specific needs without going through a lawyer.

- Reliability of professionally drafted templates to ensure compliance with legal standards.

Key takeaways

- The QJSA waiver allows your spouse to choose retirement benefits without your agreement.

- Submitting the form on time is crucial to avoid complications in retirement benefit distributions.

- Both participant and spouse must consent to the waiver for it to be valid.

Looking for another form?

Form popularity

FAQ

A QJSA is when retirement benefits are paid as a life annuity (a series of payments, usually monthly, for life) to the participant and a survivor annuity over the life of the participant's surviving spouse (or a former spouse, child or dependent who must be treated as a surviving spouse under a QDRO) following the

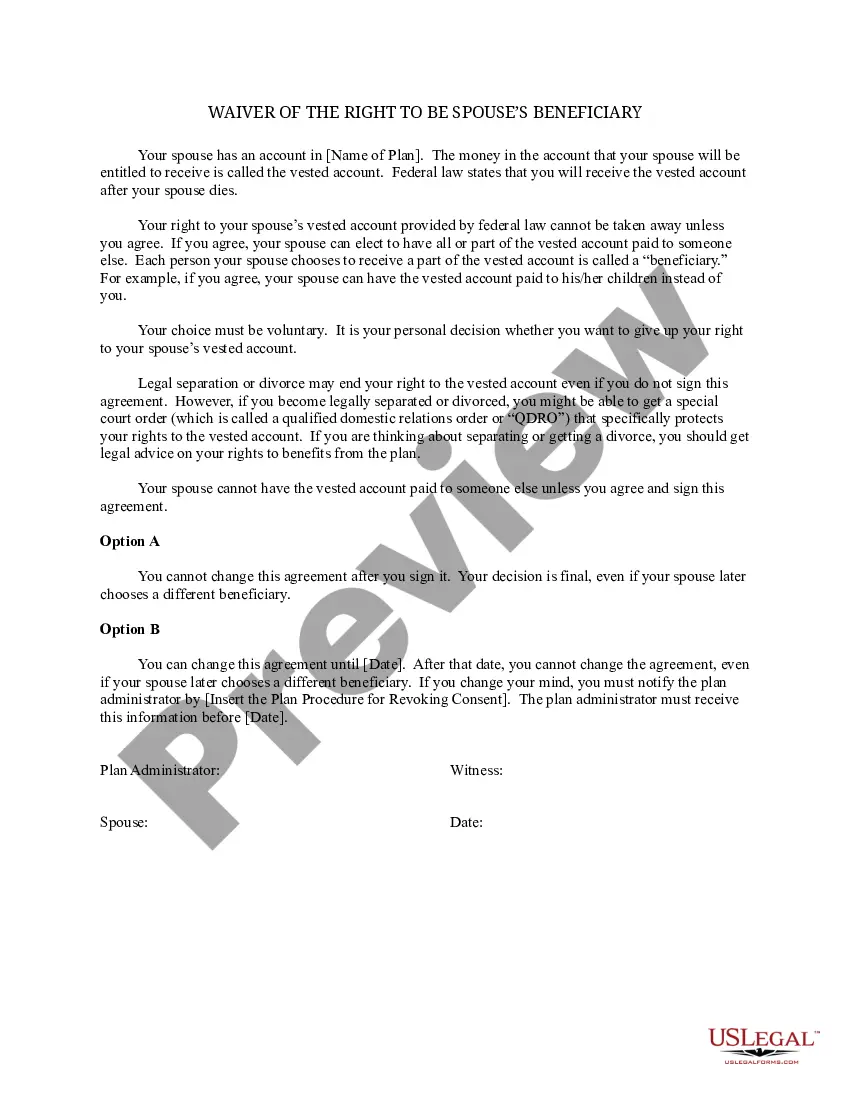

If you do not waive the QPSA, after your death the Plan will pay your spouse the QPSA unless your spouse elects another benefit form. The QPSA will not pay benefits to other beneficiaries after your spouse dies. If you waive the QPSA, the Plan will pay your account to your designated beneficiary.

A qualified joint and survivor annuity (QJSA) provides a lifetime payment to an annuitant and spouse, child, or dependent from a qualified plan. QJSA rules apply to money-purchase pension plans, defined benefit plans, and target benefits.

Qualified Joint and Survivor Annuity If your spouse consents to change the way the Plan's retirement benefits are paid, your spouse gives up his or her right to the QJSA payments. This is referred to as a waiver of the QJSA payment form.

A QJSA is when retirement benefits are paid as a life annuity (a series of payments, usually monthly, for life) to the participant and a survivor annuity over the life of the participant's surviving spouse (or a former spouse, child or dependent who must be treated as a surviving spouse under a QDRO) following the

Crisis waivers are annuity contract features that allow the annuity holder to withdraw money without triggering surrender charges. Some insurance companies classify waivers as riders, but the two aren't synonymous.

A joint-and-survivor annuity pays you during your lifetime and then continues to pay your spouse or other named beneficiary. You might be able to choose either a 100, 75, or 50 percent joint-and-survivor annuity. The 100 percent option gives your survivor the same monthly benefit that you received.

A joint and survivor annuity is an annuity that pays out for the remainder of two people's lives.And a 75 percent joint and survivor annuity will pay three-quarters of that amount to the surviving annuitant. The higher the percentage the surviving annuitant is guaranteed, the lower the initial payments will be.