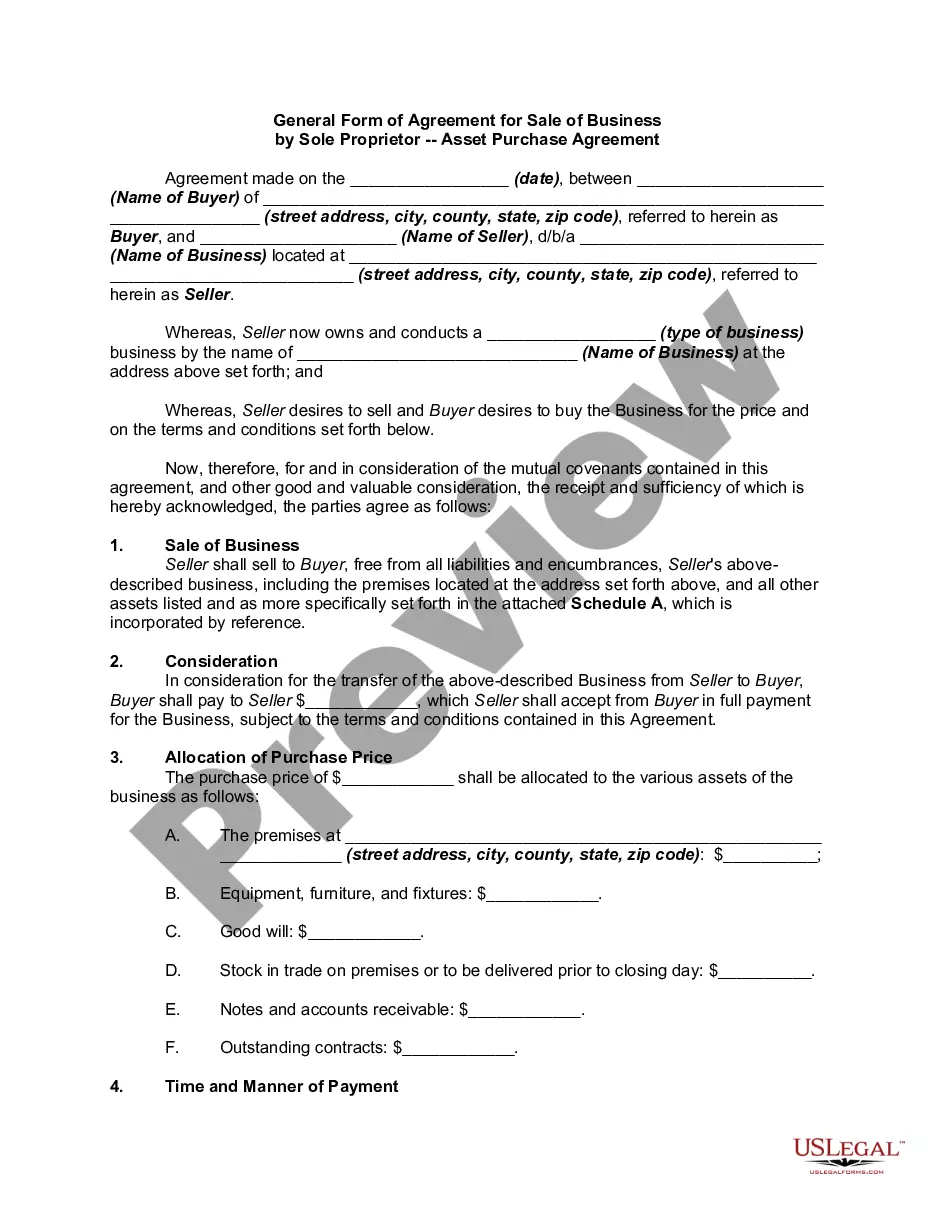

Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company

What this document covers

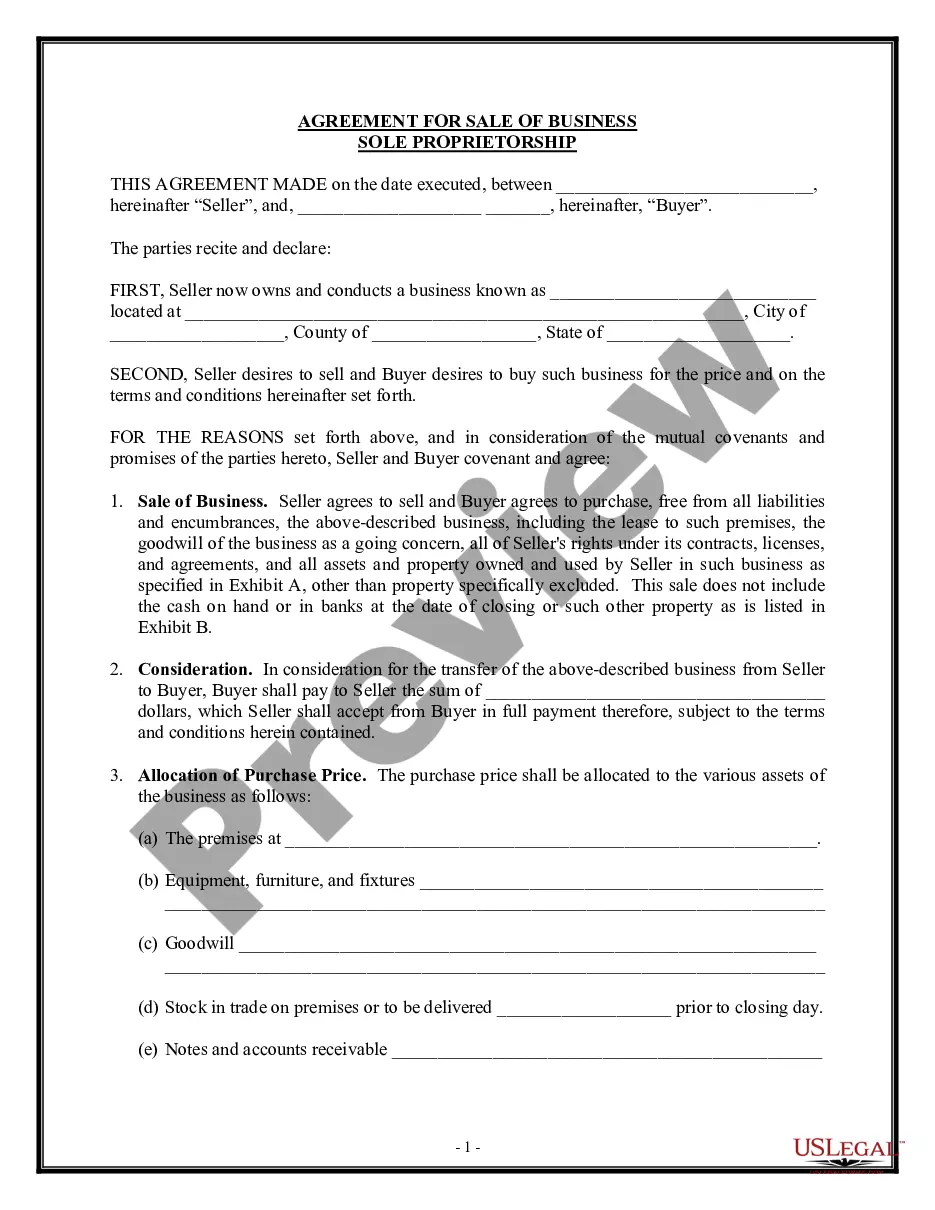

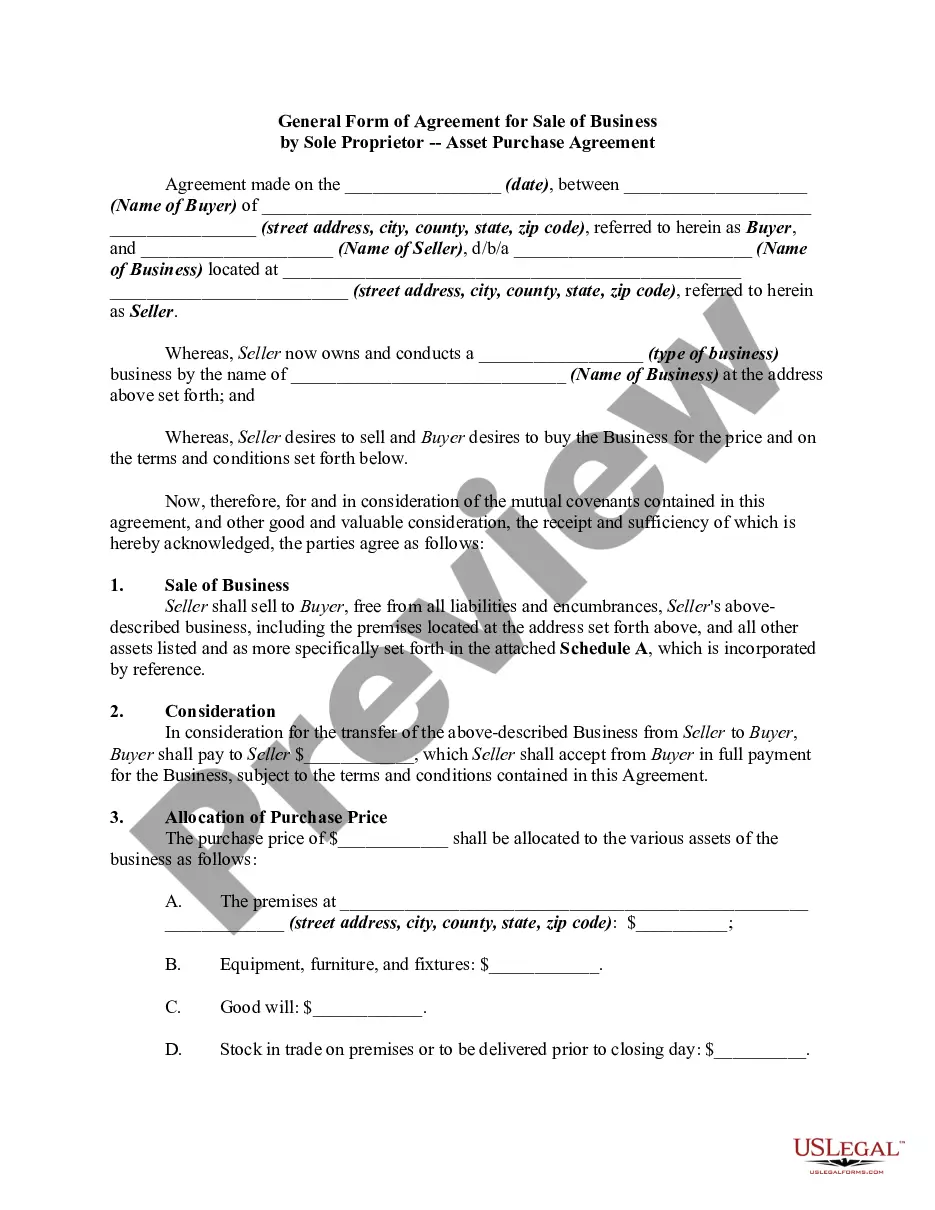

This Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company is a legal document that formalizes the sale of a business owned by a sole proprietorship to a limited liability company (LLC). It outlines the terms of the sale, including payment, assets included, and responsibilities of both the seller and buyer. This form is important as it ensures compliance with applicable laws and protects both parties' interests during the transaction, which may involve complexities such as debts, liabilities, and regulatory approvals.

Key parts of this document

- Identification of parties: Names and addresses of the seller (sole proprietorship) and buyer (LLC).

- Description of the business: Type and location of the business being sold.

- Assets to be sold: Detailed list of what is included in the sale, such as customer lists and intellectual property.

- Consideration: Payment terms, including any customer-based calculations for sale price.

- Representations and warranties: Assurances provided by the seller regarding ownership and compliance with laws.

- Covenant not to compete: Seller's agreement to refrain from operating a similar business within a specified area for a defined time.

When this form is needed

This form is useful when a sole proprietor wishes to sell their business to an LLC. It is necessary for ensuring that all parties understand their rights and obligations during the sale process. This form may be utilized in various contexts, including the transition of ownership of retail stores, service-based businesses, or any entity operating under a sole proprietorship that is being sold in full or part to an LLC.

Who can use this document

- Sole proprietors looking to sell their business fully or partially to an LLC.

- Buyers interested in acquiring a business from a sole proprietor.

- Legal professionals advising clients in business transactions.

- Accountants or financial advisors involved in the sale process.

Instructions for completing this form

- Identify and enter the names and addresses of both the seller and buyer.

- Describe the business and list all assets included in the sale.

- Clearly detail the payment structure and any conditions affecting the final sale price.

- Include representations and warranties by the seller regarding ownership and liabilities.

- Ensure both parties sign the form and keep a copy for their records.

Is notarization required?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to disclose all liabilities and debts associated with the business.

- Not specifying the payment terms clearly, leading to confusion later.

- Neglecting state-specific requirements, which can invalidate the agreement.

- Allowing the seller to compete within the terms of the sale without a clear agreement or timeframe.

Why use this form online

- Immediate access to a legally sound template drafted by licensed attorneys.

- Convenient editing options to customize the form according to specific needs.

- 24/7 availability to download and complete the form at your convenience.

Looking for another form?

Form popularity

FAQ

The main advantage of operating as a limited liability company is that there is limited liability for the sole proprietor which means the owner's personal assets are not exposed to the risks and liabilities of their business operations.

The core elements of an LLC operating agreement include provisions relating to equity structure (contributions, capital accounts, allocations of profits, losses and distributions), management, voting, limitation on liability and indemnification, books and records, anti-dilution protections, if any, restrictions on

Contact Your Lender. Form an LLC. Obtain a Tax ID Number and Open an LLC Bank Account. Obtain a Form for a Deed. Fill out the Warranty or Quitclaim Deed Form. Sign the Deed to Transfer Property to the LLC. Record the Deed. Change Your Lease.

Transferring Assets to an LLC The sole proprietor can opt to treat the asset transfer as an equity contributionwhich would establish some ownership interest in the LLCas a sale, or as a lease. If he is treating it as a sale or a lease, the LLC must pay him for the transfer.

Unlike the articles of organization, an operating agreement generally is not required in order to form an SMLLC, nor is it filed with the state. Instead, an operating agreement is optionalthough recommended. If you choose to have one, you'll keep it on file at your business's official location.

Technically, there is no such thing as a conversion from a Sole Proprietorship to an LLC. Rather, you are changing over from a Sole Proprietor to an LLC. Meaning, you simply form an LLC and then stop using your Sole Proprietorship.Open a new business bank account for your LLC.

To form a private limited company from a sole proprietorship, the procedure is to first form the private limited company and then take over the sole proprietorship through a Memorandum Of Association (MoA) and transfer all benefits and liabilities to the limited company.

There is no legal requirement that an Operating Agreement be notarized in California.

The transfer process itself can take the form of a contract for transfer/purchase of business assets. In the case of money transfers, these can be done as a loan or by purchasing shares in the other company, or through dividend payments if shares in the transferor company are owned by the recipient company.