Delinquent Account Collection History

What is this form?

The Delinquent Account Collection History form is designed to help businesses track the status of overdue accounts and document collection efforts. This form differs from other collection forms by providing a comprehensive overview of all actions taken to recover the outstanding debts, making it easier to manage delinquent accounts efficiently.

Key parts of this document

- Name of Debtor: section to identify the accountable party.

- Contact Information: includes phone number and address for effective communication.

- Date Account Opened: records when the account was established.

- Date Delinquent File Started: marks the beginning of collection efforts.

- Original Balance Due: specifies the amount originally owed.

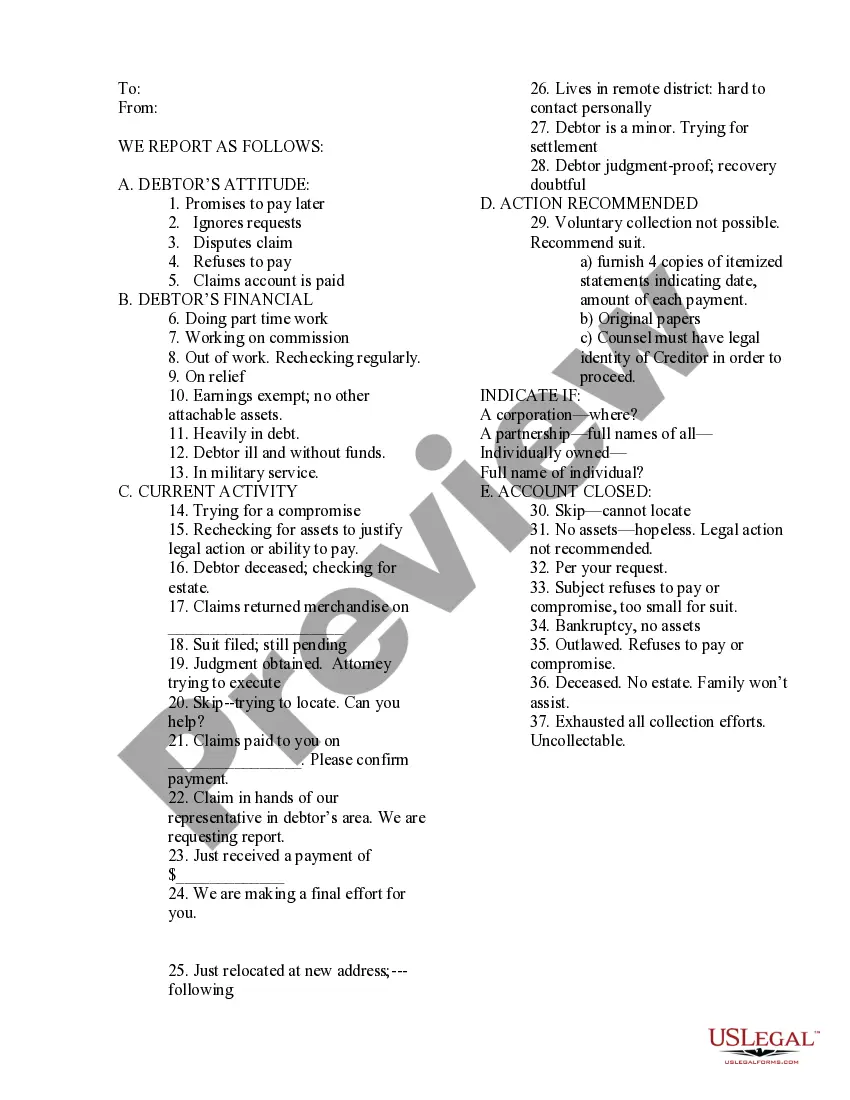

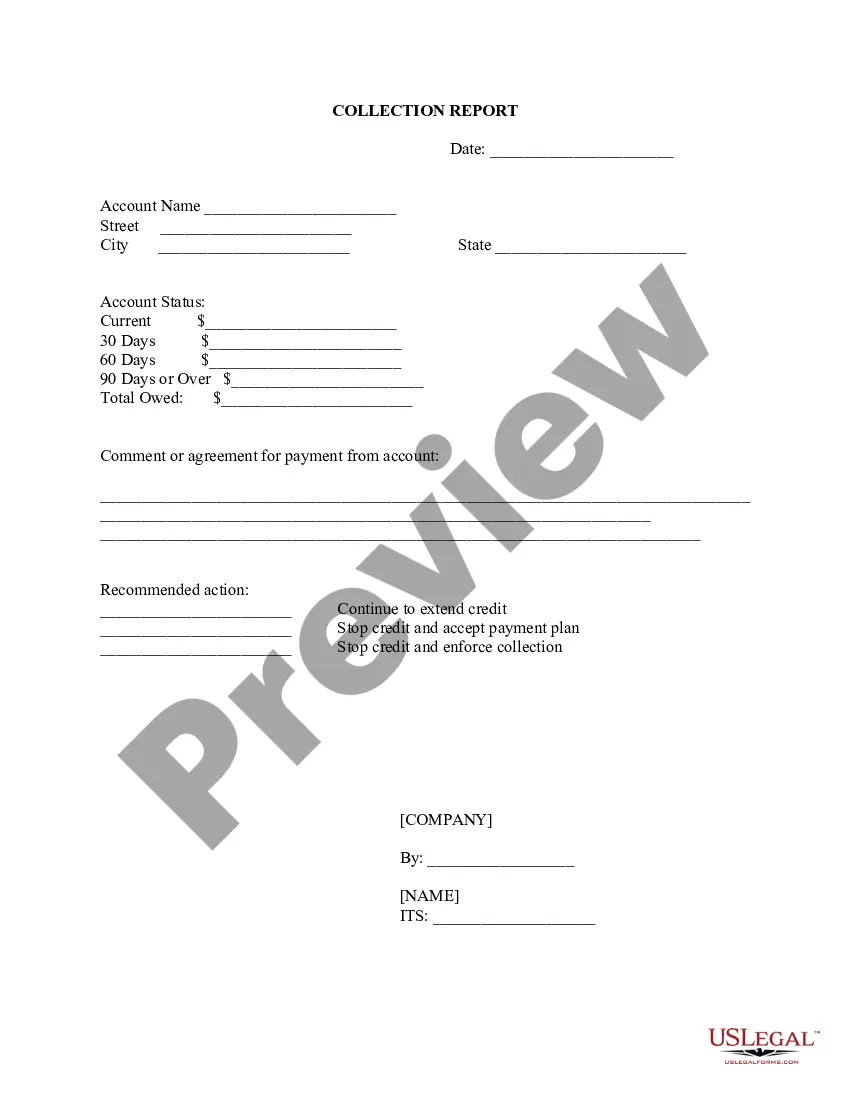

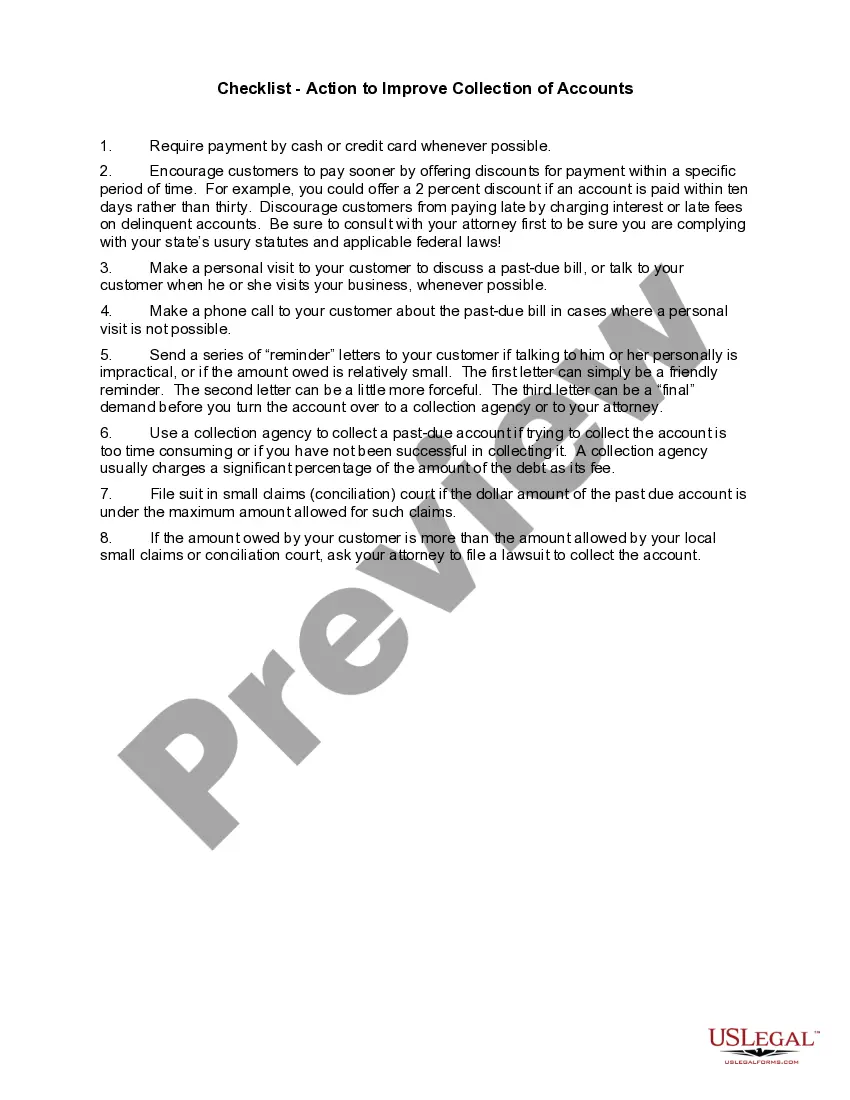

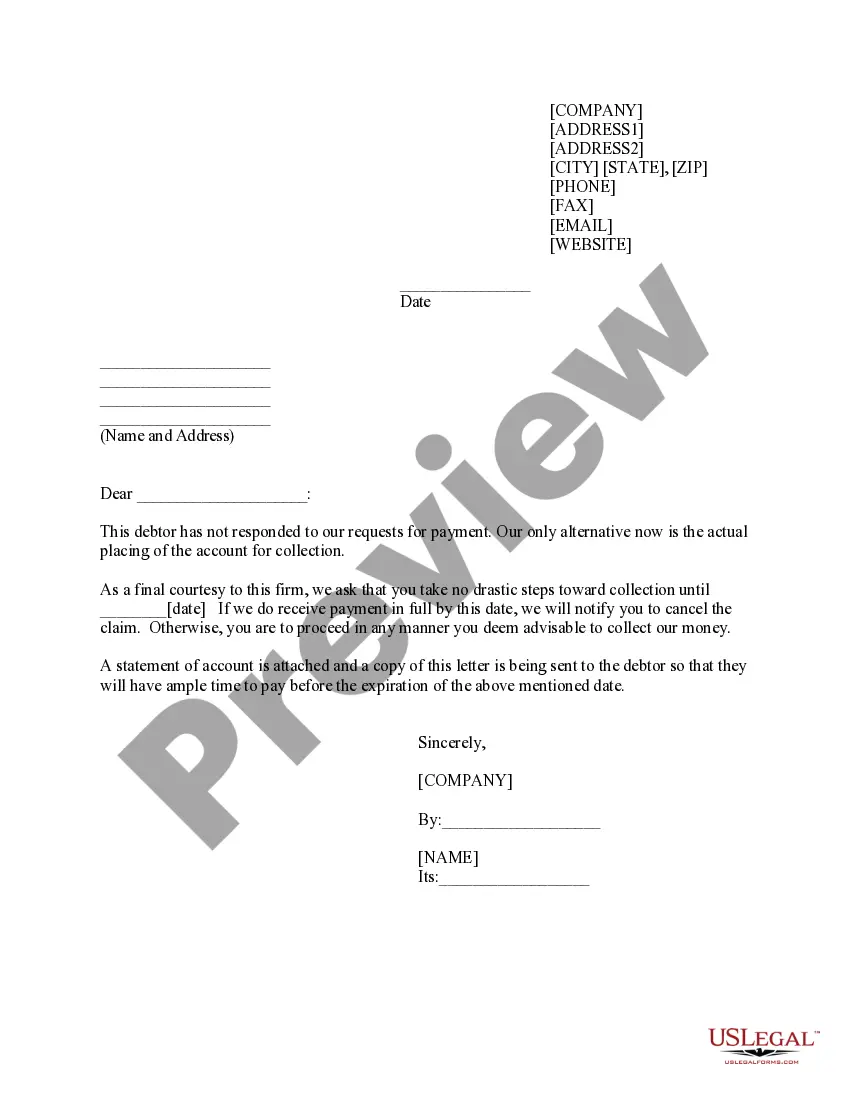

- History of Collection Efforts: detailed section for documenting all attempts to collect the debt, including phone calls and letters.

Situations where this form applies

This form should be used when a customer has failed to make payments for a significant period, and you are initiating collection efforts. It helps track the timeline and methods employed in your attempts to collect the outstanding balance, ensuring that all actions are documented and systematic.

Who needs this form

- Business owners managing accounts receivable.

- Financial professionals involved in debt collection.

- Credit managers who track overdue accounts.

- Accountants responsible for financial reporting related to delinquent accounts.

Instructions for completing this form

- Identify the debtor by entering their name and contact information.

- Specify the date when the account was opened and when collection efforts began.

- Fill in the original balance due and any payments made.

- Document all collection efforts in the provided section, including dates and methods used.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Neglecting to update the balance after payments are made.

- Failing to document all collection attempts thoroughly.

- Not including accurate contact information for the debtor.

Advantages of online completion

- Easy download and access at any time.

- Editable fields allow customization for individual needs.

- Streamlined tracking of collection efforts promotes better financial management.

Quick recap

- This form is essential for documenting collection efforts on delinquent accounts.

- Accurate records can aid in potential legal action if necessary.

- Using this form can simplify communication and tracking of payments with clients.

Looking for another form?

Form popularity

FAQ

Submit a Dispute to the Credit Bureau. Dispute With the Business That Reported to the Credit Bureau. Send a Pay for Delete Offer to Your Creditor. Make a Goodwill Request for Deletion.

How do I remove a delinquent account from my report? As previously stated, delinquent accounts are typically removed seven years after the date of the original delinquency.If you believe a credit bureau has included a delinquency that is inaccurate or outdated, you can file a dispute with the credit bureau.

Each month, you'll have to make a payment by the due date on your account. (With credit cards, your best bet is usually to pay your monthly statement balance in full.) From a lender or card issuer's point of view, if your due date comes and goes without you making a payment, your account is delinquent.

The statute of limitations is a law that limits how long debt collectors can legally sue consumers for unpaid debt. The statute of limitations on debt varies by state and type of debt, ranging from three years to as long as 15 years.

How Long Can a Debt Collector Pursue an Old Debt? Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. In most states, they run between four and six years after the last payment was made on the debt.

If you dispute the incorrect late payment with your creditor, they typically have 30 days to investigate. If the creditor stands by the reported late payment, it won't remove or update the information. But if it agrees that the information is incorrect, the creditor has to tell the credit bureau to update or remove it.

A late payment, also known as a delinquency, will typically fall off your credit reports seven years from the original delinquency date. For example: If you had a 30-day late payment reported in June 2017 and bring the account current in July 2017, the late payment would drop off your reports in June 2024.

Just paying off a delinquent debt isn't likely to affect your credit history in the short term.In a perfect credit reporting world, the account would be updated within 30 days to show that the balance has been zeroed out. However, you shouldn't assume that a creditor or collection agency will do so automatically.