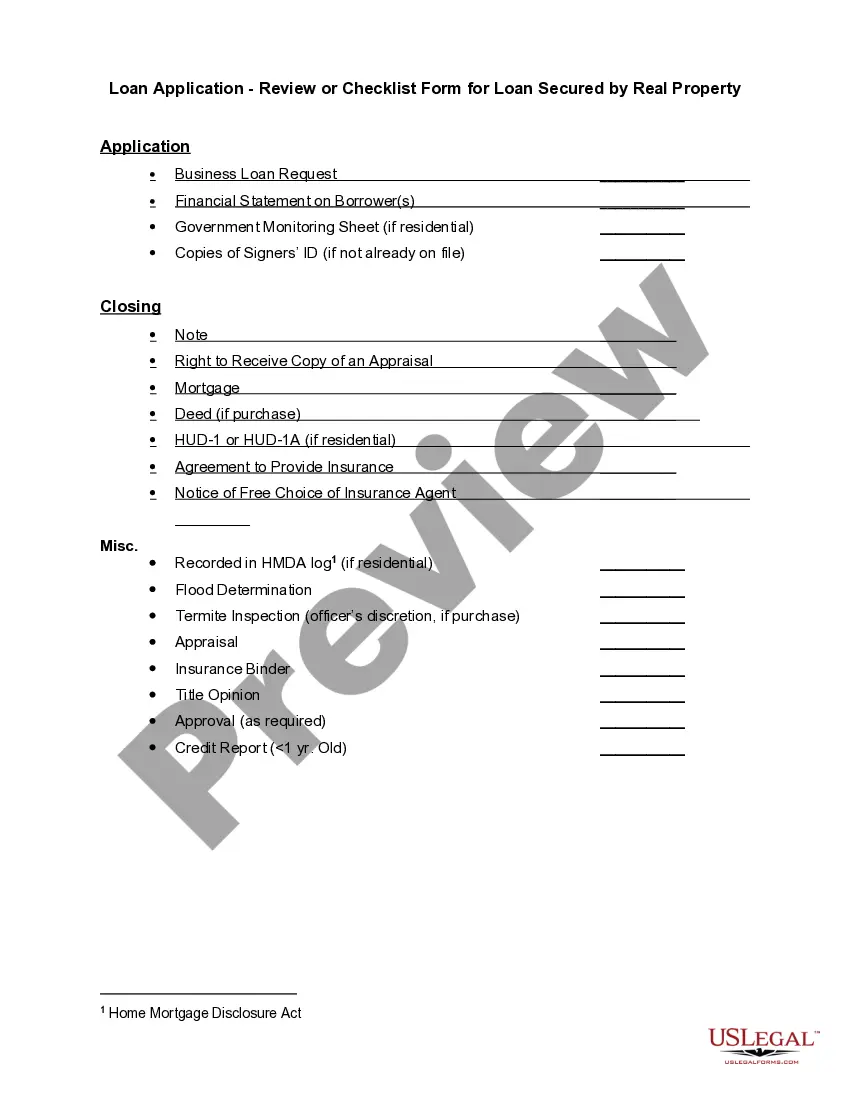

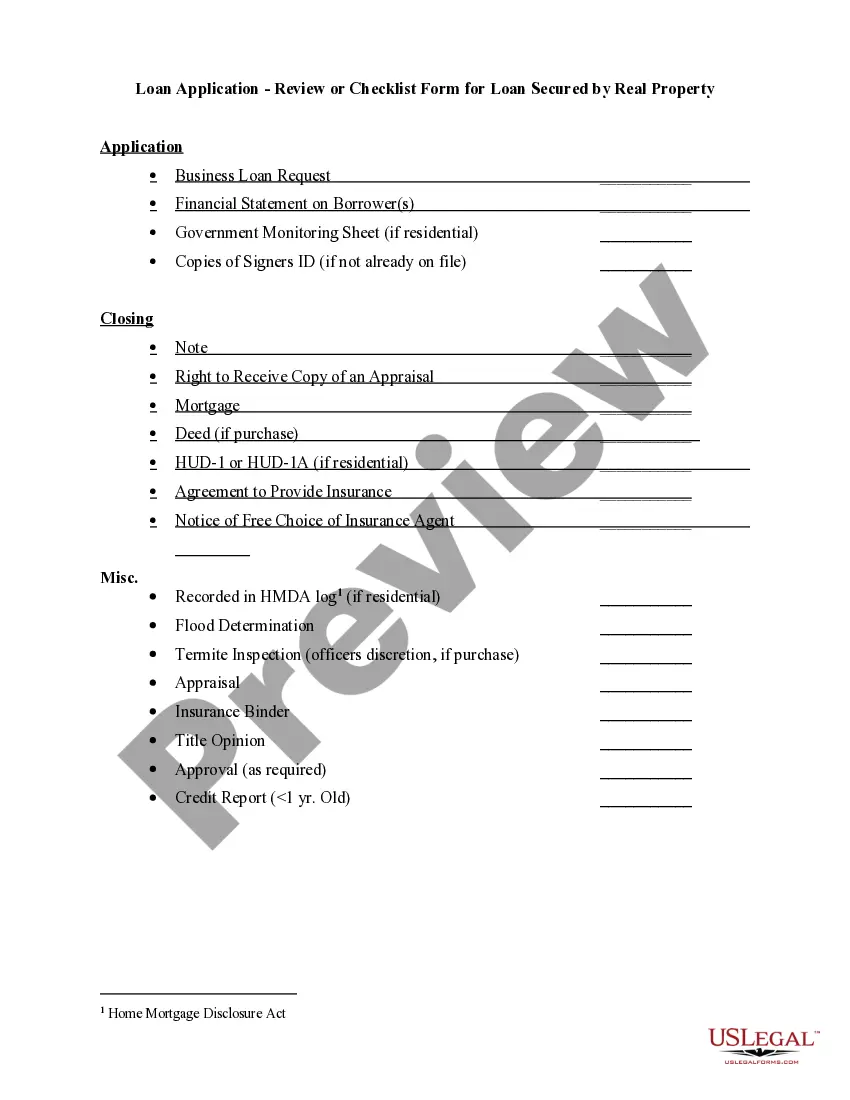

Checklist for Business Loans Secured by Real Estate

Understanding this form

The Checklist for Business Loans Secured by Real Estate is a comprehensive guide designed to facilitate the preparation and submission of a commercial loan application where real property is the primary form of collateral. This form stands apart by providing a detailed checklist of essential documents and requirements specific to real estate-secured business loans.

Form components explained

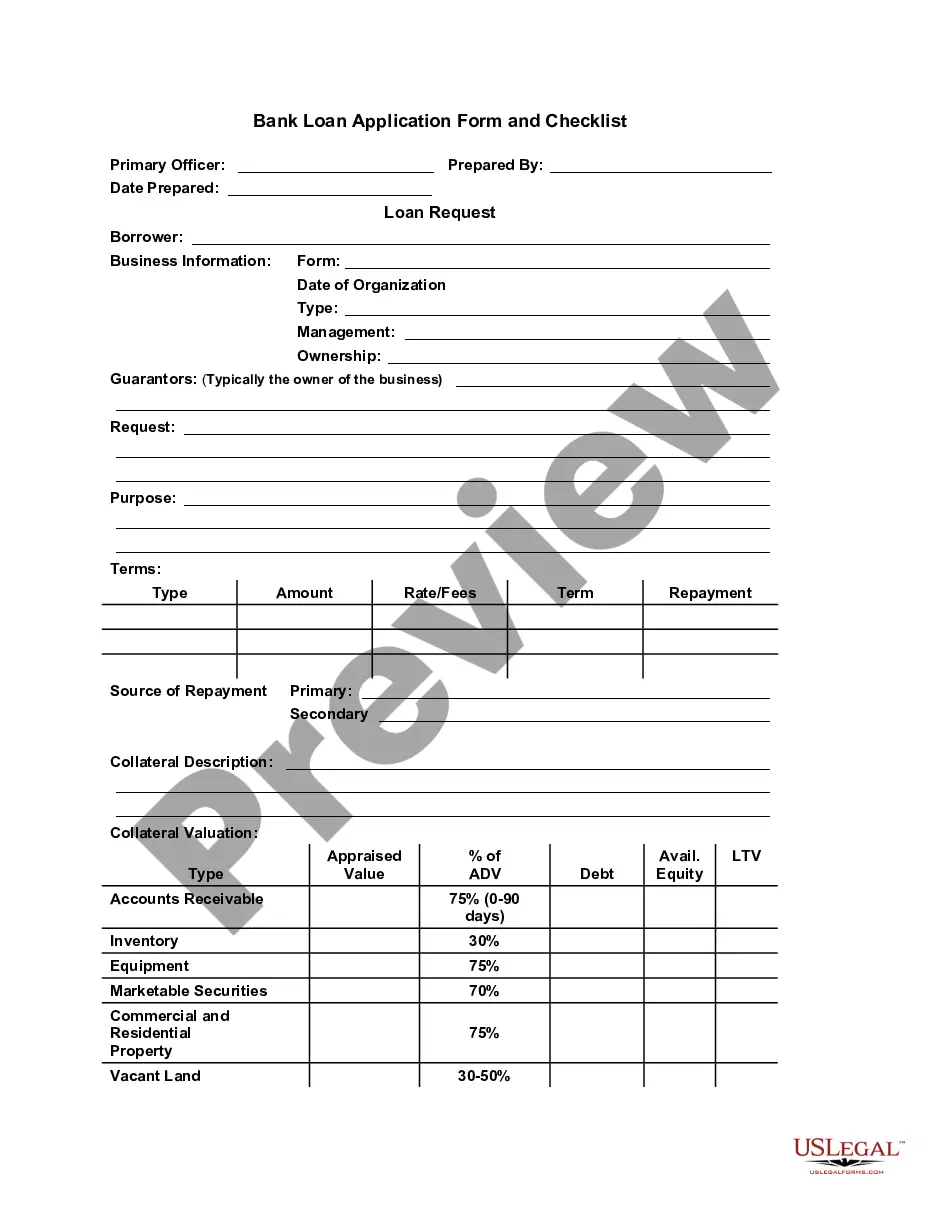

- Application for Business Loan Request

- Financial Statement on Borrower(s)

- Government Monitoring Sheet (if applicable)

- CIP Disclosure

- Copies of Signers ID

- Mortgage Agreement

- Title Opinion

- Credit Report (1 year old)

Situations where this form applies

This form is ideal when a business seeks financing and intends to secure the loan with real estate assets. Use it when preparing to apply for a commercial loan, ensuring all necessary documents and agreements are included to satisfy lender requirements.

Who needs this form

- Business owners seeking loans secured by real estate

- Financial institutions reviewing commercial loan applications

- Attorneys assisting clients in securing loans

- Individuals managing real estate transactions for business purposes

Completing this form step by step

- Identify the business and the borrowers involved in the loan application.

- Compile needed documentation such as financial statements and identification.

- Complete the application form meticulously, ensuring accuracy and completeness.

- Gather secondary required documents, such as the mortgage and appraisal reports.

- Review the checklist to ensure all items are accounted for before submission.

Does this document require notarization?

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Omitting necessary documentation such as financial statements.

- Failing to update records like the credit report.

- Providing incorrect or outdated identification for signers.

- Neglecting to confirm the terms and requirements of the lender before submission.

Benefits of using this form online

- Convenient access to the form at any time for quick downloads.

- Edit and customize the form to fit specific business needs.

- Ensure reliability with forms drafted by licensed attorneys.

- Streamline the application process with an organized checklist format.

Legal use & context

- This checklist is designed to help ensure compliance with lending standards when using real estate as collateral.

- Failure to provide all required documentation may impact the enforceability of the loan agreement.

- Consulting with a legal expert can provide specific guidance based on your stateâs regulations.

Main things to remember

- The Checklist for Business Loans Secured by Real Estate is an essential tool for simplifying loan applications.

- Gather all required documents early in the process to avoid delays.

- Understanding state-specific regulations can help ensure compliance and a smoother transaction.

Looking for another form?

Form popularity

FAQ

These include checking accounts, savings accounts, mortgages, debit cards, credit cards, and personal loans., he may use his car or the title of a piece of property as collateral. If he fails to repay the loan, the collateral may be seized by the bank, based on the two parties' agreement.

Truth-in-Lending Act (TILA) Generally, no. TILA does not apply to business-purpose loans (including loans to acquire, improve or maintain non-owner occupied rental property) or loans made to entities. Real Estate Settlement Procedures Act (RESPA) Generally, no.

How much collateral do I need for a business loan? Most lenders want collateral that's worth at least as much as the loan you hope to secure. So if you're looking to borrow $50,000 for your business, the assets to secure it must have a cash value of at least $50,000.

Documents Needed for the Business Loan Application SBA Form 413, Personal Financial Statement. SBA Form 1919, Borrower Information. SBA Form 912, Statement of Personal History. 3 years of federal personal tax returns.

For a business loan, business assets such as equipment, vehicles, buildings, and inventory can be used as collateral. Accounts receivables can also be used as collateral. Any business asset that has value and can be sold by the lender to pay off the loan if necessary can be considered collateral.

Understanding Regulation U It applies to entities other than broker-dealers such as commercial banks, savings and loan associations, federal savings banks, credit unions, production credit associations, insurance companies and companies that have employee stock option plans.

Figure out how much money you need. Decide what type of loan best fits your needs. Check your credit scores. Put together the required documents. Assess the value of your collateral. Shop around for the best business loan terms. Apply for a business loan.

While you may be able to get a small business loan without having to offer collateral, that doesn't mean the lender won't ask for other conditions. Specifically, you may be asked to sign a personal guarantee or agree to a Uniform Commercial Code (UCC) lien.