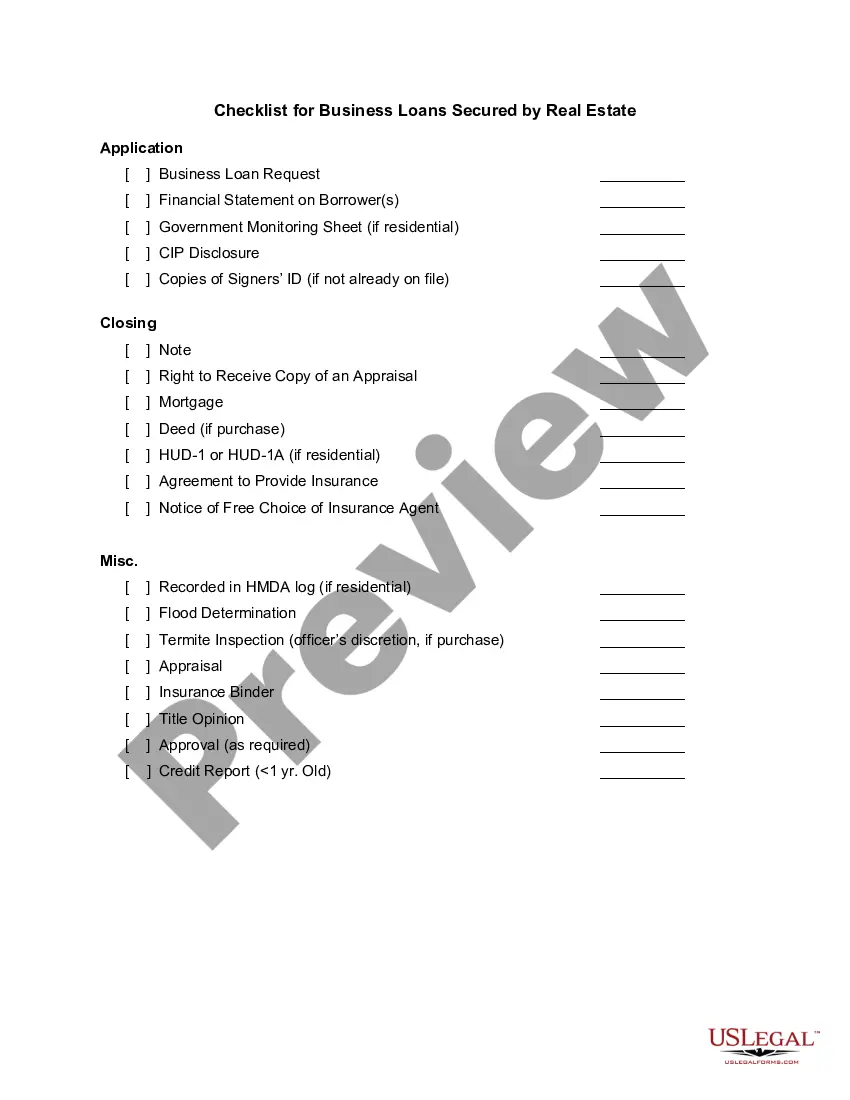

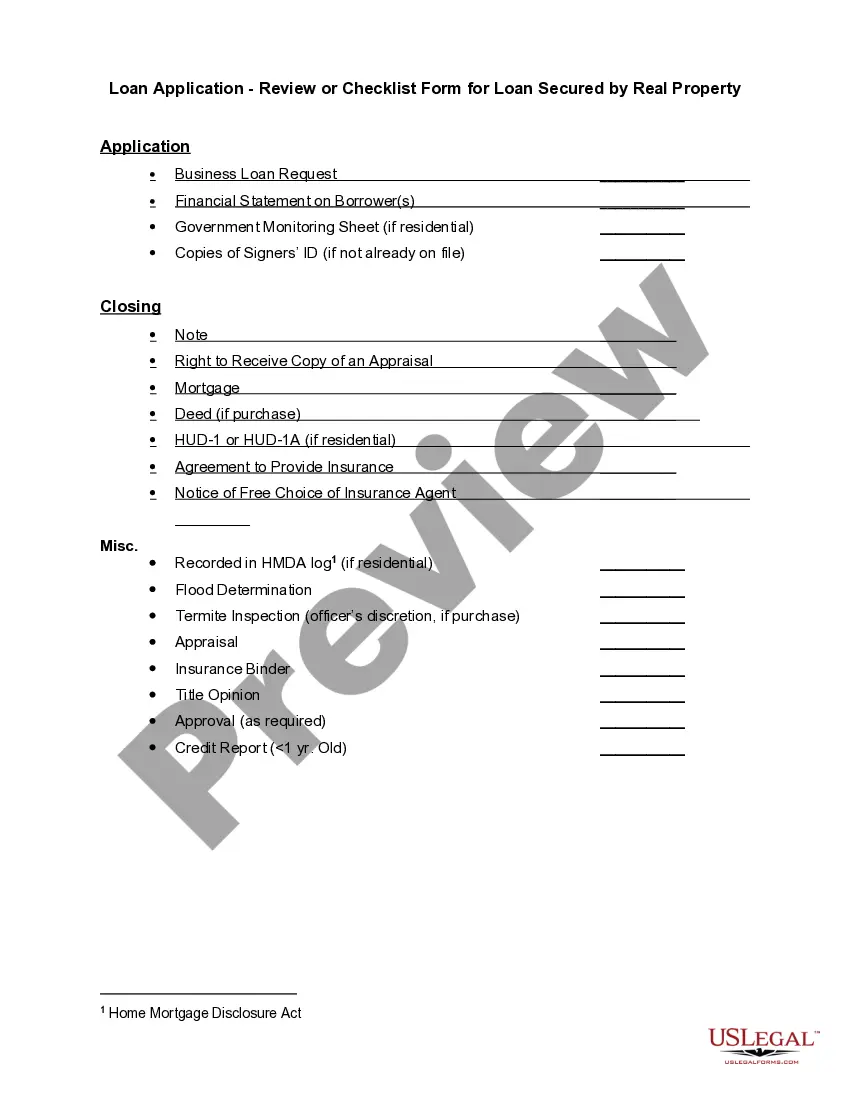

Checklist for Real Estate Loans

What this document covers

The Checklist for Real Estate Loans is a comprehensive tool designed to guide lenders and borrowers through the critical steps involved in real estate loan transactions. Unlike standard loan documents, this checklist categorizes various lender-specific requirements and borrower responsibilities, ensuring all parties are thoroughly prepared for the loan process. It incorporates detailed checklist items that apply to different types of real estate loans, from mortgages to construction financing.

Key components of this form

- General lender checklist for all types of mortgages.

- Specific checklists for construction lenders and loan modifications.

- Borrowers' checklists detailing required documentation and timelines.

- Checklists for different loan structures, such as leasehold mortgages and wraparound loans.

- Guidelines for lender requirements in various state laws.

When to use this form

This checklist should be used when engaging in any real estate lending process, especially for complex transactions involving multiple parties or issues. It is particularly useful for lenders preparing to issue loans, borrowers looking to understand their obligations, or professionals involved in real estate financing who need a structured approach to ensure compliance and minimize risks.

Intended users of this form

- Lenders issuing various types of real estate loans.

- Borrowers seeking loans for home purchases, construction projects, or refinancing.

- Real estate professionals, including attorneys and agents, aiding in loan transactions.

How to complete this form

- Start by identifying the type of loan and relevant parties involved.

- Review each specific checklist section corresponding to the loan type being utilized.

- Gather required documentation as outlined for both lenders and borrowers.

- Ensure all checklists relevant to the transaction are completed and addressed.

- Finalize the documents and secure necessary signatures before proceeding with the loan agreement.

Notarization guidance

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to customize the checklist for specific transaction types.

- Overlooking local legal requirements that could affect the loan structure.

- Missing crucial deadlines for documentation submission.

- Neglecting to confirm the completeness of each checklist item before closing.

Advantages of online completion

- Easy access to downloadable checklists tailored for various real estate transactions.

- Editable templates allow for customization to fit specific needs.

- Increased reliability in following legal standards and requirements.

- Instant updates reflecting the latest legal changes in real estate financing.

Legal use & context

- This checklist aids in minimizing risks associated with loan transactions.

- It serves as a framework for compliance with federal and state regulations.

- Proper use of this checklist can enhance the enforceability of the underlying loan agreements.

What to keep in mind

- The Checklist for Real Estate Loans ensures thorough preparation for lenders and borrowers.

- It categorizes requirements to streamline the lending process.

- Use this form to minimize risks and adhere to legal standards in real estate transactions.

Looking for another form?

Form popularity

FAQ

A closing agent prepares the closing statement, which is settlement sheet. It's a comprehensive list of every expense that the buyer and seller must pay to complete the real estate transaction. Fees listed on this sheet include commissions, mortgage insurance, and property tax deposits.

Which Type of Loan Is Best for You? What Is the Interest Rate and Annual Percentage Rate? How Much of a Down Payment Is Required? What Are the Discount Points and Origination Fees? What Are All the Costs? Can You Get a Loan Rate Lock? Is There a Prepayment Penalty? How Much Time Do You Need to Fund?

Loan terms. Projected loan payments. Cash to close. Closing cost breakdown & total. Comparison of initial Loan Estimate quote versus Closing Disclosure. Summary of purchase and loan details. Additional details such as assumption, prepayment options, escrow explanations, and more.

ID and Social Security number. Pay stubs from the last 30 days. W-2s or I-9s from the past 2 years. Proof of any other sources of income. Federal tax returns. Recent bank statements. Details on long term debts such as car or student loans. Real estate property information.

In a Nutshell Depending on your unique financial situation, there are several documents you might need when you apply for a home loan, including your tax returns, pay stubs, bank statements and credit history.

ESCROW HOLDERPrepares final closing by handling loan documents and making sure they are returned to the lender, records deed, delivers deed to Buyers, deliver funds due Sellers per instruction and issues closing statements.

Apply for a Loan. Prepare to Pay Closing Fees. Examine the Title. Get a Home Appraisal. Schedule a Home Inspection. Get Homeowner's Insurance. Transfer Utilities. Take a Final Walk-Through.

Get all contingencies squared away. Clear the title. Get final mortgage approval. Review your closing disclosure. Do a final walk-through. Bring the necessary documentation to closing.

Banks assess a borrower's income, other loans and living expenses to calculate how much money can be put towards home loan repayments. In the current market, lenders are looking much harder at borrowers' expenses by analysing credit card statements, transaction accounts and any recurring spending patterns.