Contract for the Sale of Motor Vehicle - Owner Financed with Provisions for Note and Security Agreement

What this document covers

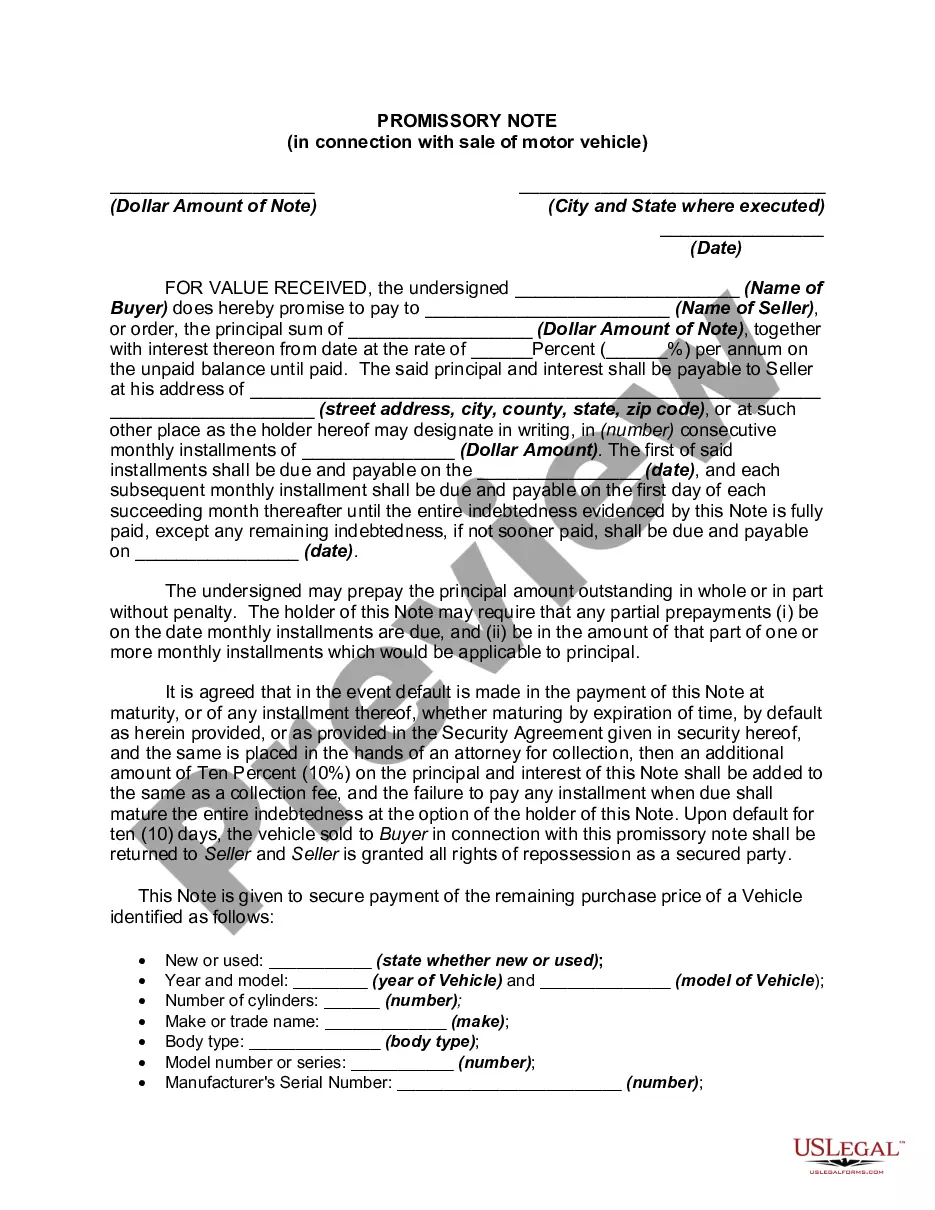

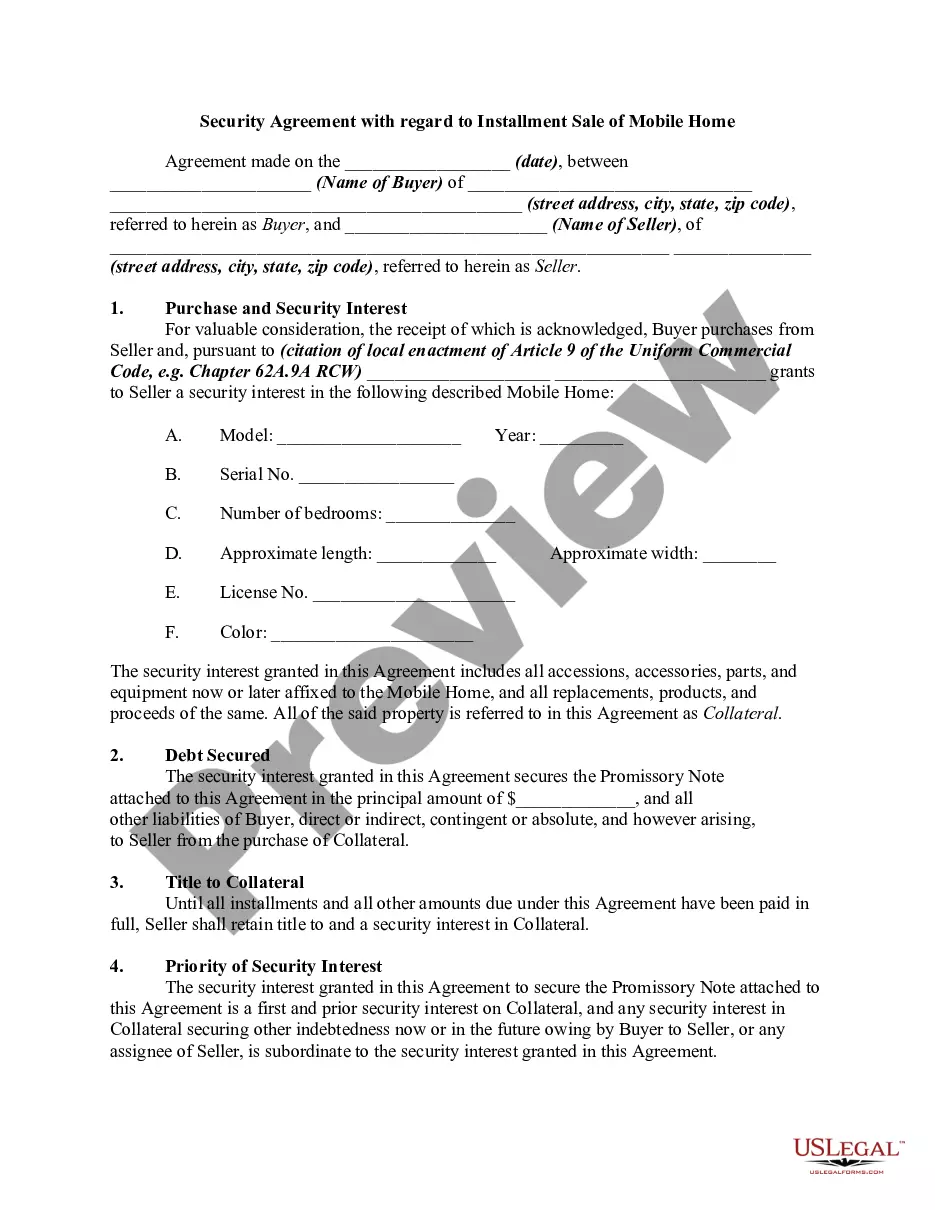

The Contract for the Sale of Motor Vehicle - Owner Financed with Provisions for Note and Security Agreement is a legal document used to outline the terms of a vehicle sale between a buyer and a seller without the involvement of a dealer. This form differs from typical vehicle sales contracts as it includes provisions for owner financing, securing the transaction with a promissory note and a security agreement. This ensures that the seller has a secured interest in the vehicle until full payment is made.

Key parts of this document

- Details of the parties involved, including names and addresses.

- Specifics about the motor vehicle being sold, including make, model, year, and identification numbers.

- Purchase price and payment terms, including down payments and payment schedules.

- Provisions for a security agreement, outlining the seller's rights in case of buyer default.

- Clauses addressing warranties, risk of loss, and inspection rights of the buyer.

- Conditions for default and remedies available to the seller.

When to use this form

This form is useful when an individual is selling a motor vehicle and wishes to offer financing directly to the buyer rather than requiring full payment upfront. It's appropriate for private sales where the seller retains an interest in the vehicle until the loan is repaid, ensuring they have legal recourse in case of default on payments.

Who this form is for

This contract is intended for:

- Individual sellers who want to provide financing options to the buyer.

- Buyers who wish to purchase a vehicle with an installment payment plan.

- Anyone who desires a clear and legally binding agreement to protect their interests in a motor vehicle sale.

Steps to complete this form

- Identify the buyer and seller, including their complete contact details.

- Specify the details of the motor vehicle, such as make, model, year, and identification numbers.

- Enter the sale price, down payment amount, and terms of payment for the remaining balance.

- Include the provisions for the promissory note and security agreement as they relate to the transaction.

- Both parties must sign and date the agreement, and if required, ensure appropriate acknowledgement or notarization is obtained.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. It is advisable to consult relevant local regulations or legal counsel to confirm whether notarization is necessary for enforceability in your state.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include clear payment terms or not specifying the total sale price.

- Omitting details about the vehicle, such as identification numbers and condition.

- Not addressing the default terms or remedies available to the seller.

- Neglecting to have both parties sign and date the agreement.

Why use this form online

- Instant access to professionally drafted legal templates that save time and reduce the hassle of document preparation.

- Easy customization of the form to fit the specific needs of your vehicle sale.

- Compliance with legal standards and terms that are clear and understandable.

Looking for another form?

Form popularity

FAQ

Used for private vehicle sales where the seller provides financing, this contract sets out the terms of the sale between buyer and seller without a dealer. It includes a promissory note and a security agreement to secure the seller's interest until the purchase price is fully paid, and to define default remedies.

The promissory note in this form is the buyer's written promise to repay the agreed purchase price in installments as part of an owner-financed sale. It works with the security agreement to create a lender's recourse if payments are late or missed, helping protect the seller's financial interest.

Use this Contract for the Sale of Motor Vehicle - Owner Financed with Provisions for Note and Security Agreement to document a private car sale with seller financing. It captures the parties, vehicle details, price, down payment, payment schedule, and the security interest, creating a legally binding agreement.

This contract includes default provisions and remedies available to the seller, outlining recourse if the buyer misses payments or breaches the agreement. These terms help protect the vehicle until full payment is received while the buyer retains rights defined elsewhere, such as warranties, risk of loss, and inspection rights.

Individual sellers who want to provide financing, buyers who want an installment purchase, and anyone seeking a clear, legally binding motor vehicle sale agreement should use this form. It reflects the intended users in the description and supports a private sale with defined terms and protections.

This form is specifically designed for owner-financed sales and includes explicit provisions for a promissory note and a security agreement to secure the seller's interest. A standard car sale contract typically does not include those financing provisions or the same security structure.