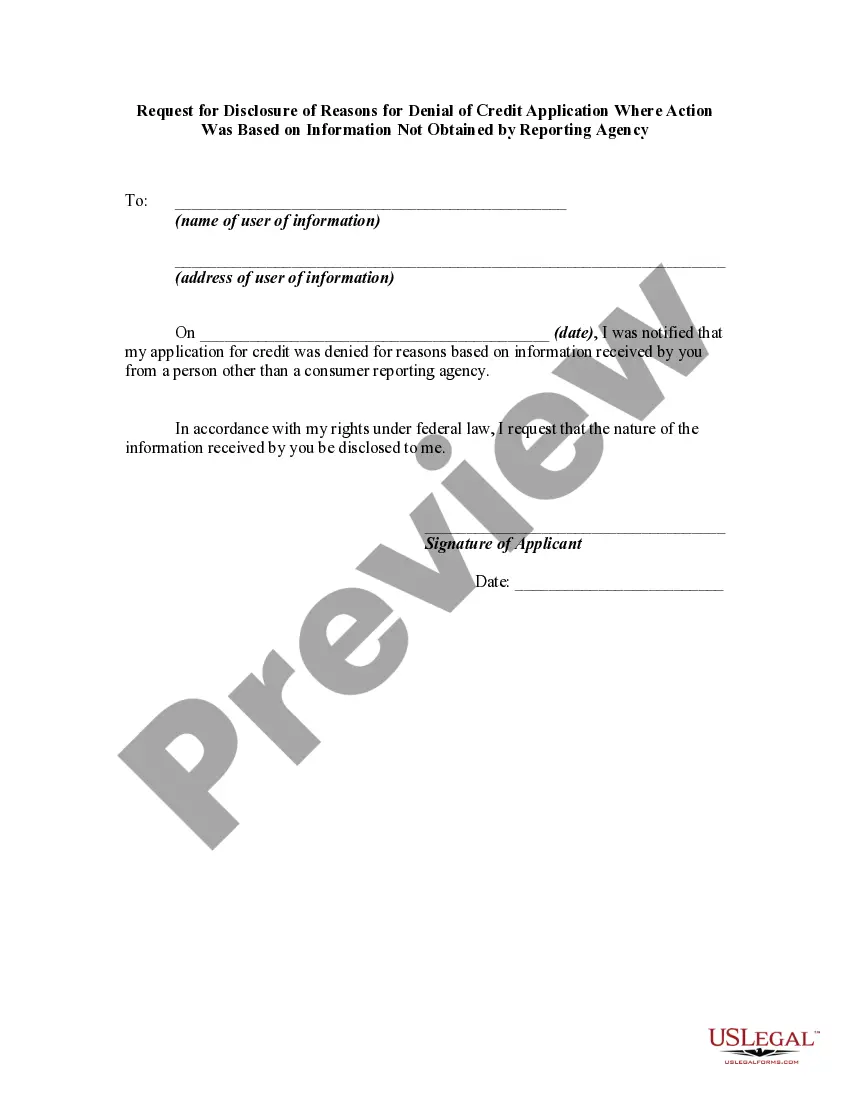

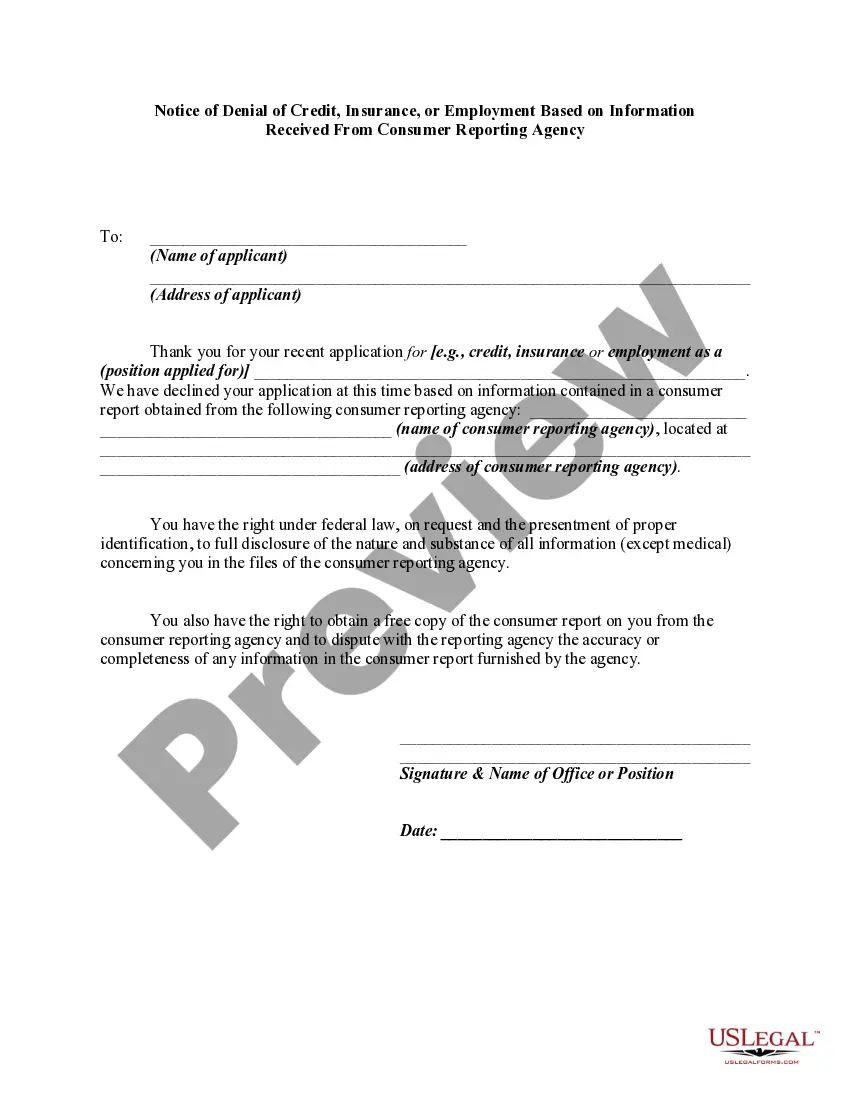

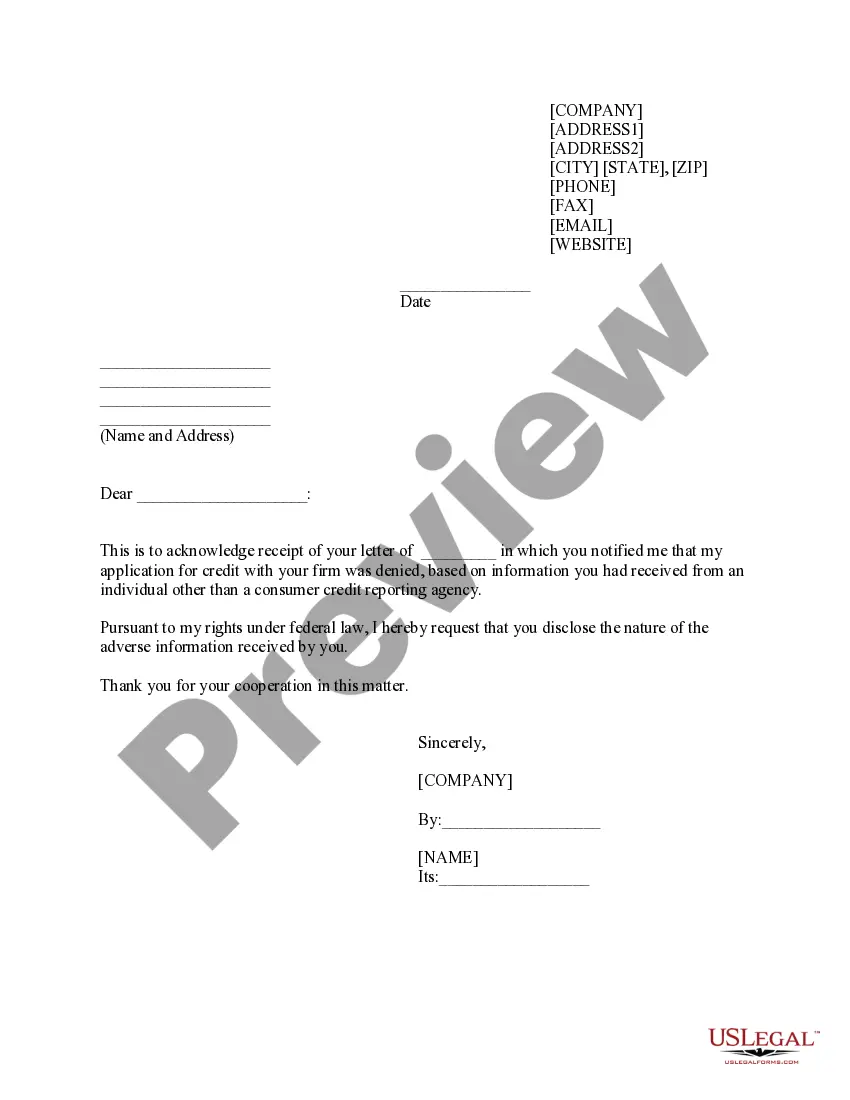

Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency

About this form

The Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document used when a credit application is denied. This form informs the applicant that their credit was declined due to information obtained from sources other than credit reporting agencies. It outlines the applicant's rights, including the right to request the information that led to the denial. This form is distinct from other credit denial notifications, as it specifically references non-agency sources influencing the credit decision.

Form components explained

- Applicant's name and address fields

- Notification of credit denial

- Disclosure of the basis for denial stemming from non-consumer reporting agency sources

- Information regarding the applicant's rights to request further details

- Signature, name of the office or position, and date fields

When to use this form

This form should be used whenever a lender or creditor denies a credit application for personal, family, or household purposes based on information obtained from a person other than a consumer reporting agency. It is essential for maintaining transparency and compliance with federal regulations regarding credit decisions.

Intended users of this form

- Lenders or creditors who deny credit applications.

- Businesses offering credit services for personal, family, or household purposes.

- Financial institutions complying with consumer protection laws.

Steps to complete this form

- Enter the name of the applicant in the designated field.

- Provide the applicant's complete address.

- Clearly state the reason for the credit denial based on non-agency information.

- Sign and date the form, including the name of the office or position of the signer.

- Send the completed form to the applicant within the required time frame.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to provide the applicant's complete address.

- Not including the specific reason for denial based on non-agency information.

- Neglecting to inform the applicant of their rights regarding information disclosure.

- Inadequate signatures or missing date fields.

Advantages of online completion

- Immediate access to a legally vetted template.

- Easy to fill out and customize for individual circumstances.

- Downloadable format allows for easy printing and distribution.

- Ensures compliance with federal regulations regarding credit denial notifications.

Looking for another form?

Form popularity

FAQ

Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include:a refusal to grant credit in the amount or terms requested. a negative change in account terms in connection with an unfavorable review of a consumer's account 5 U.S.C. § 1691(d)(6); FCRA A§ 603(k)

Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include: a denial or revocation of credit. a refusal to grant credit in the amount or terms requested. a negative change in account terms in connection with an unfavorable review of a consumer's account 5 U.S.C. § 1691(d)(6); FCRA A§ 603(k)

Give notice of the adverse action; Give the name, address, and telephone number of the credit reporting agency which provided the credit report (the telephone number must be toll free if the agency compiles and maintains consumer files on a nationwide basis);

Whenever a statement of a dispute is filed, unless there is rear sonable grounds to believe that it is frivolous or irrelevant, the consumer reporing agency shall, in any subsequent report containing the informaion in quesion, clearly note that it is disputed by the consumer and provide either the consumer s statement

Common violations of the FCRA include: Creditors give reporting agencies inaccurate financial information about you. Reporting agencies mixing up one person's information with another's because of similar (or same) last name or social security number. Agencies fail to follow guidelines for handling disputes.

In the hiring process, adverse action means a company is considering not hiring the applicant or that they may withdraw an offer. Usually, this is based on an adverse report on a consumer report or background check.

An adverse action occurs when an employer behaves in a way that puts an individual or a group of people at a disadvantage as far as equal employment opportunities go. For example, take an employee who files a lawsuit against his or her employer.

If applicable, financial institutions can provide a combined notice of adverse action to all consumer applicants to comply with multiple-applicant requirements under the FCRA, provided a credit score is not required for the adverse action notice because a score was not relied upon in taking adverse action.

A statement of action taken by the creditor. Either a statement of the specific reasons for the action taken or a disclosure of the applicant's right to a statement of specific reasons and the name, address, and telephone number of the person or office from which this information can be obtained.