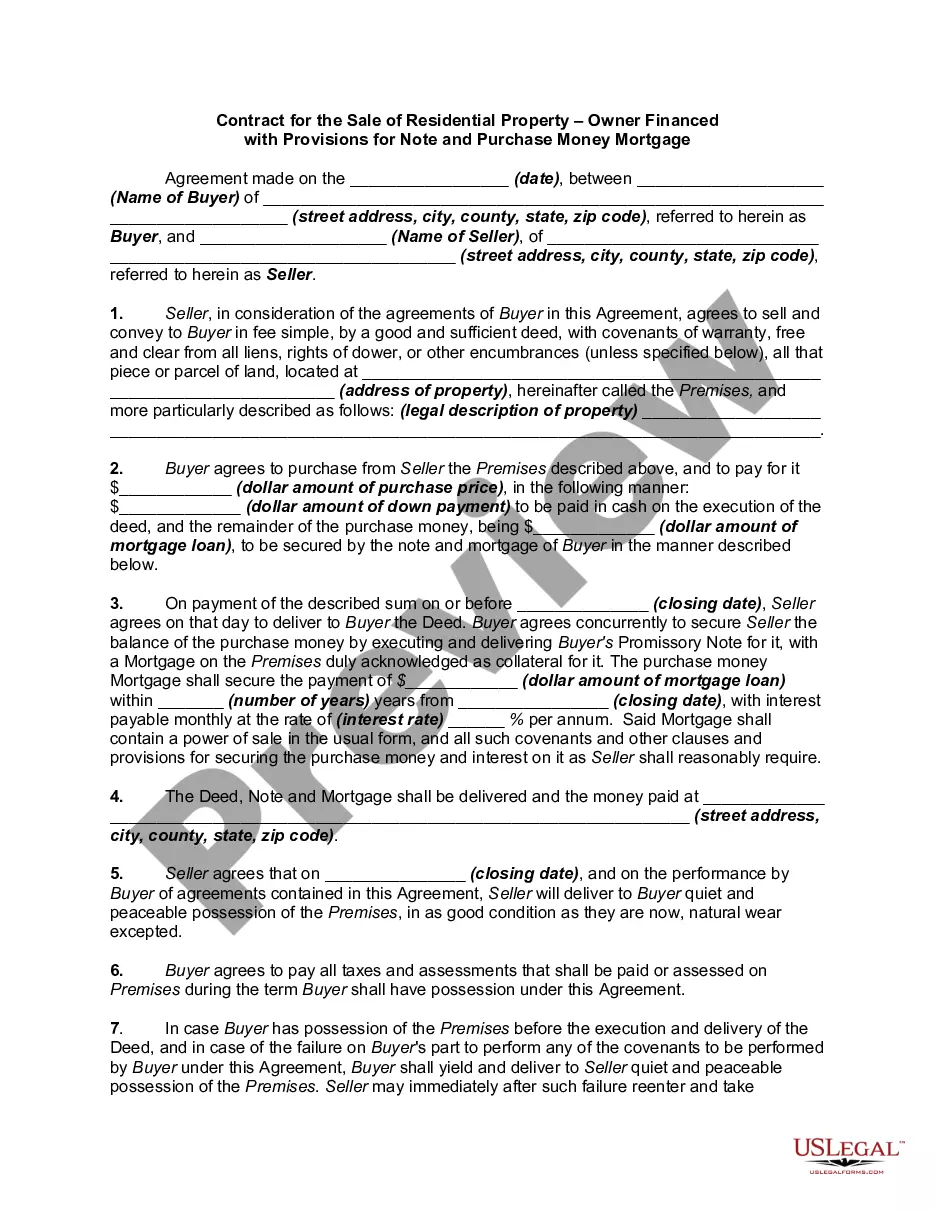

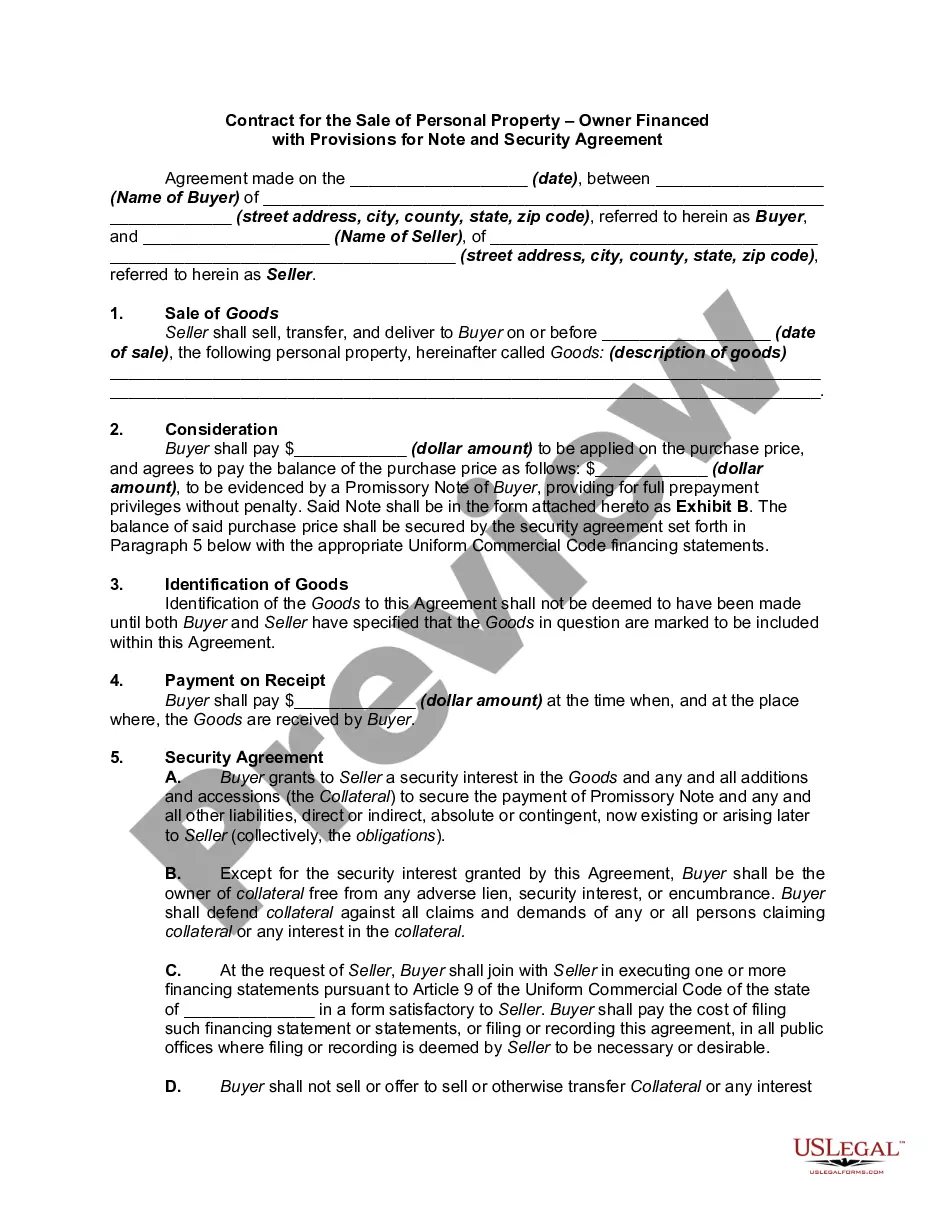

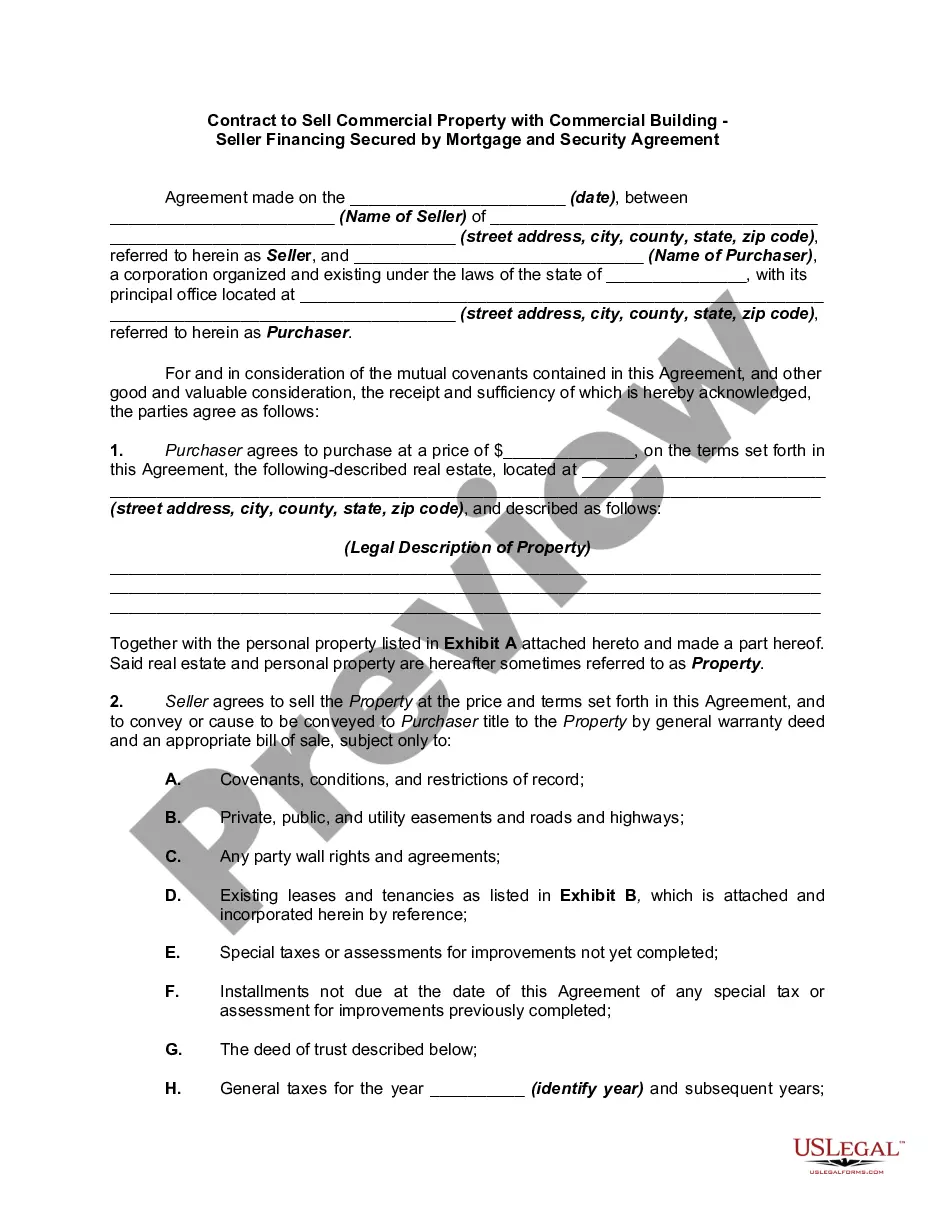

Contract for the Sale of Commercial Property - Owner Financed with Provisions for Note and Purchase Money Mortgage and Security Agreement

What is this form?

This document is a Contract for the Sale of Commercial Property tailored for owner financing. It serves as a legal agreement between a buyer and seller, outlining the terms of purchasing commercial real estate while providing financing directly from the seller. This form is distinct from standard real estate contracts as it includes provisions specifically for a purchase money mortgage and security agreement. This allows buyers who may not qualify for traditional financing to purchase property through seller financing, making the transaction mutually beneficial.

Key parts of this document

- Details of the buyer and seller, including corporation names and addresses.

- Describes the real estate and personal property being sold.

- Outlines the purchase price and payment terms, including earnest money and mortgage details.

- Defines conditions related to title transfer and any exceptions to title.

- Specifies required documents, such as a title commitment and plat of survey.

- Includes clauses about default, dispute resolution, and the overall governing law.

When this form is needed

This contract is useful when a buyer wishes to purchase commercial property without traditional financing and the seller is willing to provide owner financing. It is particularly applicable in scenarios where either party prefers a more personalized agreement, enabling flexible terms suitable to both parties. The agreement can also be vital in commercial transactions where conventional loan options are limited.

Who should use this form

- Business owners seeking to buy commercial property with direct financing from the seller.

- Sellers of commercial real estate who wish to finance the sale themselves.

- Real estate agents who facilitate owner-financed transactions.

- Lenders considering alternative financing arrangements for business acquisitions.

Steps to complete this form

- Identify and include the names and addresses of both the buyer and seller at the top of the contract.

- Specify the purchase price and terms of payment, including the amount of earnest money.

- Clearly describe the property being sold along with any personal property included in the sale.

- Detail any title exceptions and conditions surrounding the closing process.

- Ensure both parties sign and date the agreement to finalize the contract.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, verifying local regulations is essential for ensuring the document is legally binding.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all necessary parties in the contract.

- Omitting specific details about the property or financing terms.

- Not clarifying the title exceptions, leading to potential disputes.

- Forgetting to attach necessary exhibits, such as the survey or title commitment.

Benefits of completing this form online

- Convenient access to professionally drafted legal documents from your home.

- Immediate download allows for quick use without waiting for physical copies.

- Forms are editable, enabling you to tailor the agreement to your specific needs.

- Reliability through templates that comply with legal standards.

Looking for another form?

Form popularity

FAQ

With owner financing (aka seller financing), the seller doesn't hand over any money to the buyer as a mortgage lender would. Instead, the seller extends enough credit to the buyer to cover the purchase price of the home, less any down payment. Then, the buyer makes regular payments until the amount is paid in full.

The seller financing addendum outlines the terms at which the seller of the property agrees to loan the money to the buyer in order to purchase their property.Once complete, this addendum should be signed and attached to the purchase agreement made between the parties.

Owner financing allows buyers who wouldn't otherwise be able to enter the market to participate. It also helps buyers spread out the cost of the land over a number of monthly payments, which can then be offset by using creative ways to make money from raw land.

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan).

Purchase price. Down payment. Interest rate. Number of monthly installments. Responsibilities of the buyer and seller. Legal remedies for the seller if the buyer does not make payments.

Step 1: Obtain the current principal balance and interest rate from the land contract or promissory note. Step 2: Times the balance by the interest rate. Step 3: Divide by 12. Step 1: A seller-financed note has a balance of 100,000 at 8% interest. Step 2: $100,000 x 8% (or .08) = $8,000 (interest for the year)

Advantages of buying an owner-financed home In a seller-financed transaction there are no closing costs such as loan origination fees, discount points and mortgage insurance premiums. Because you won't have to wait for bank approvals, closing can happen much quicker than with traditional financing.

Interest rateInterest rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk by holding financing, and he or she may charge a higher interest rate to offset this risk. It's not uncommon to see interest rates from 4% to 10%.

Complete the addendum, including your name, the purchaser's name and a description of the property. Include the type of financing that you are providing, such as first mortgage, second mortgage or deed of trust. List the terms of the loan.