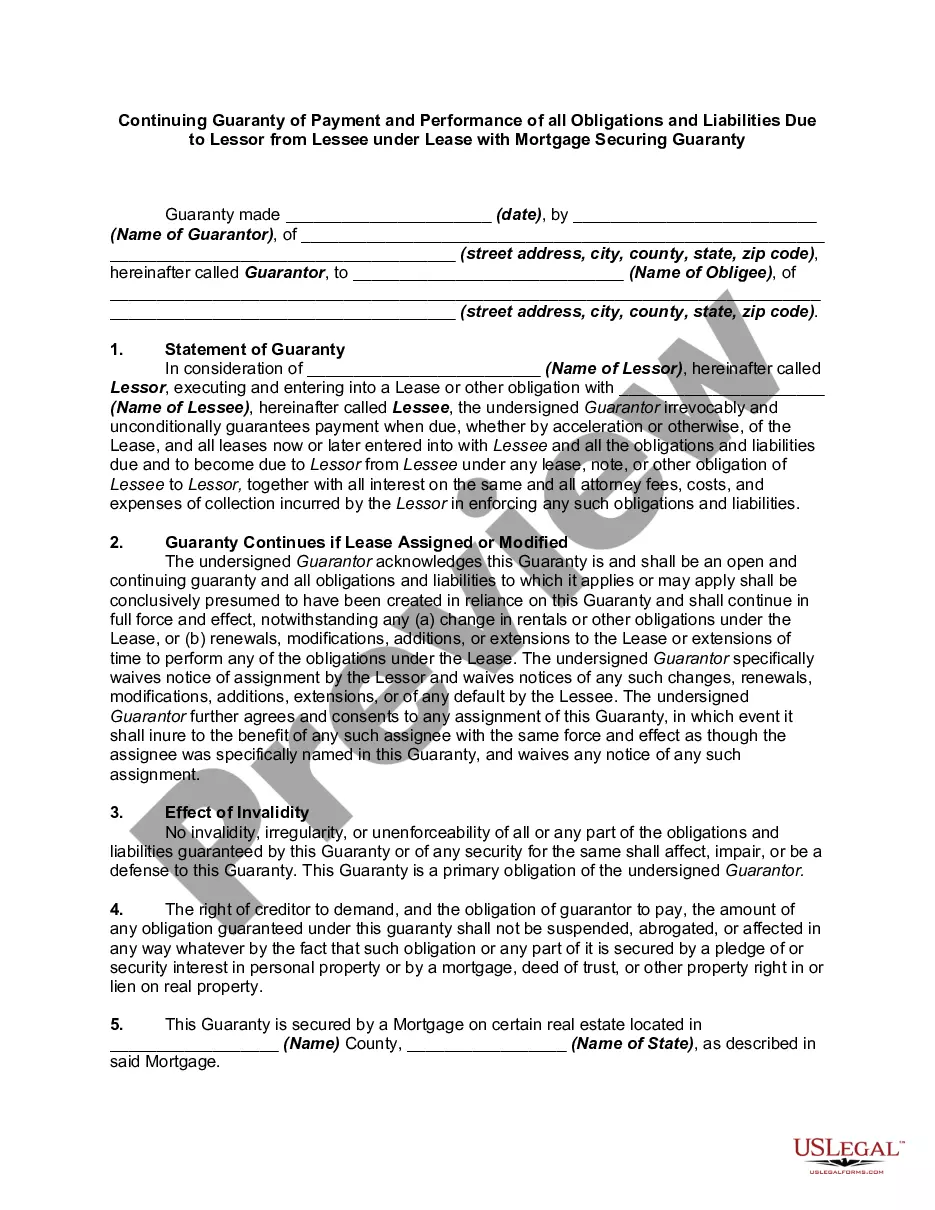

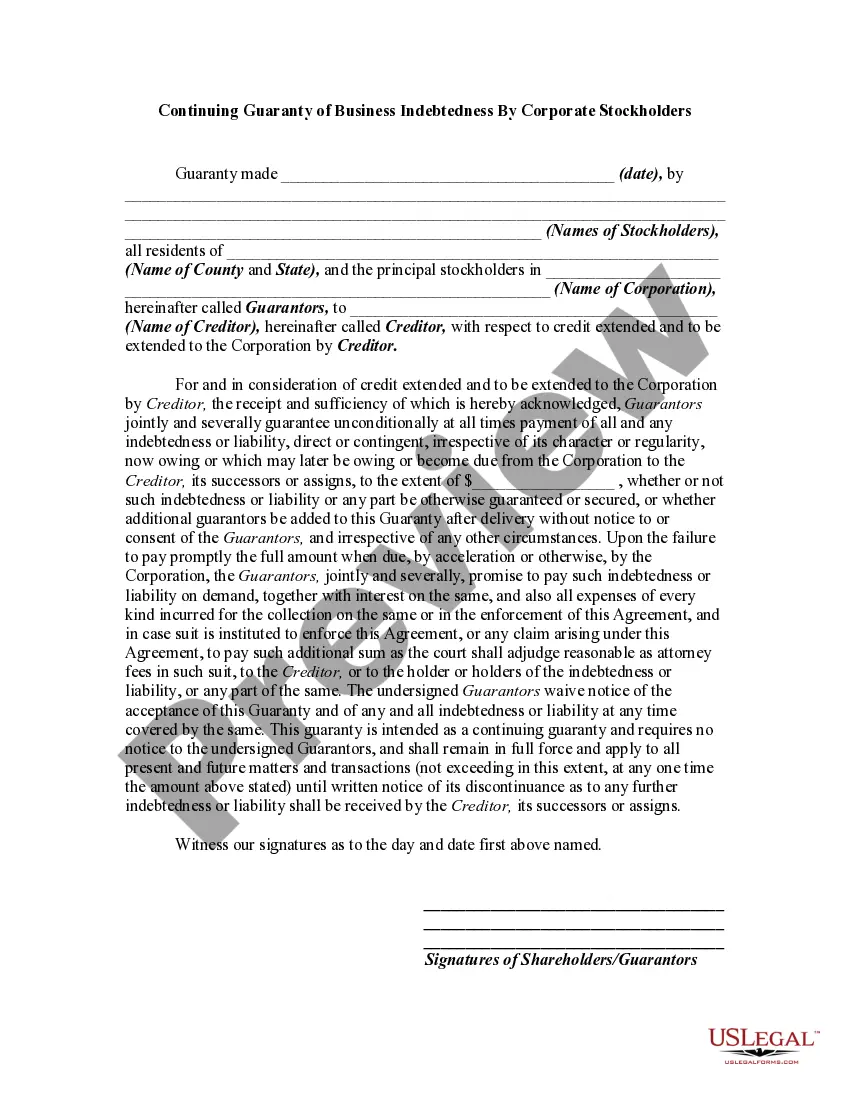

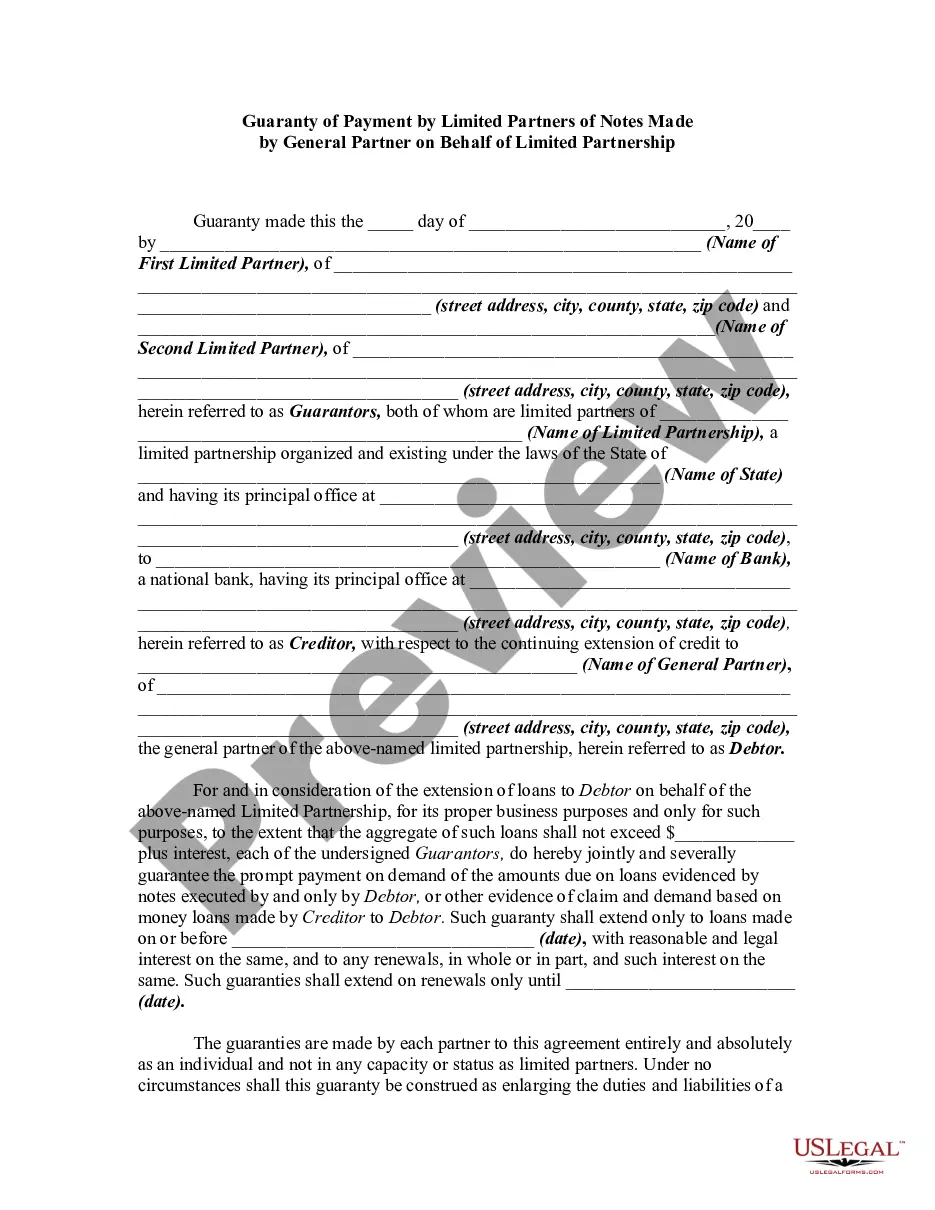

Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability

What this document covers

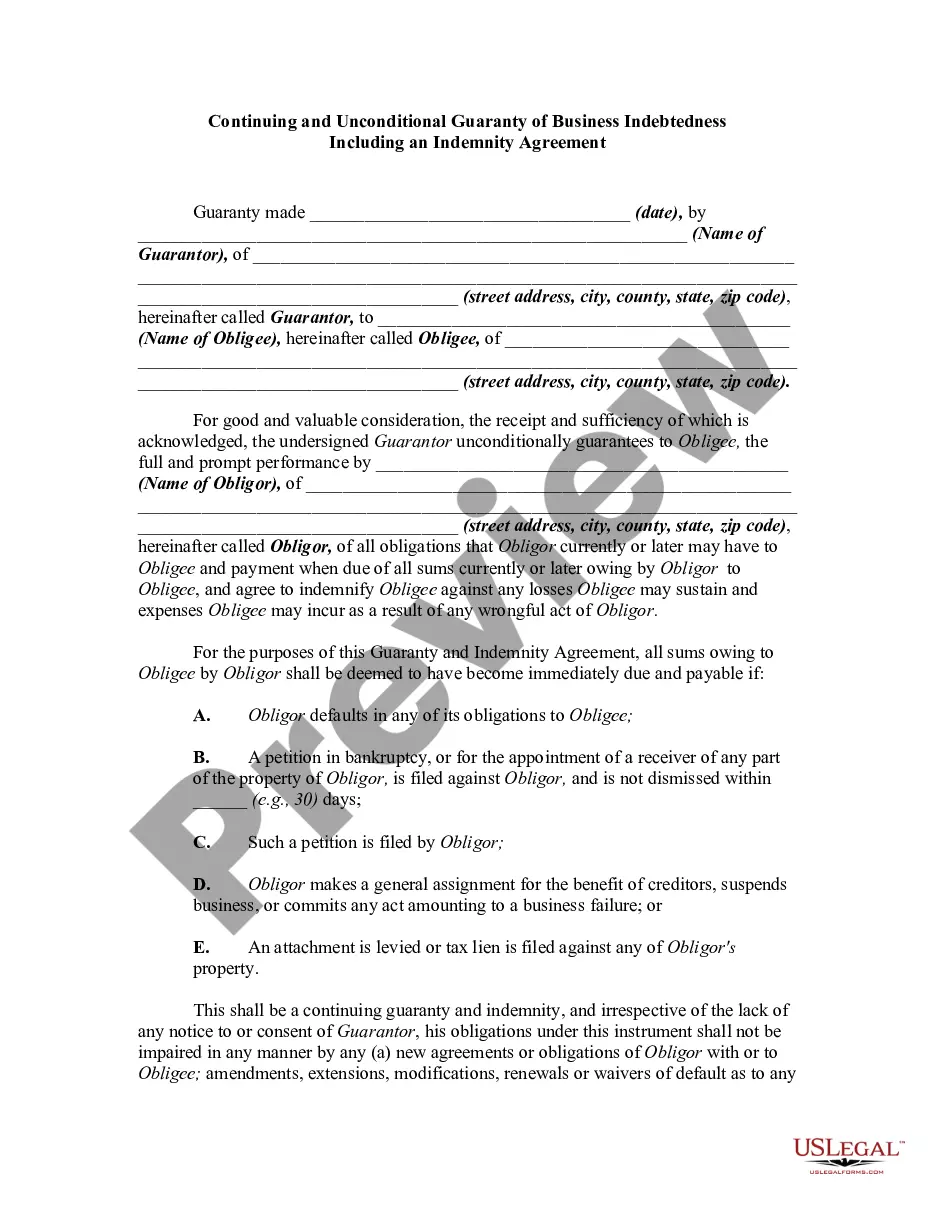

The Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal agreement where a guarantor agrees to take responsibility for a debtor's obligations in case of default. Unlike other guaranty forms, this document explicitly outlines the limitations of the guarantor's liability. It is important for creditors to ensure the obligations of the debtor are met without fully exposing the guarantor's personal assets.

Form components explained

- Identification of the Creditor, Debtor, and Guarantor.

- Specification of the obligations guaranteed by the Guarantor.

- Terms regarding the continuing nature of the guaranty.

- Clauses waiving the requirement for notice of acceptance and defaults.

- Limitations on the Guarantor's liability.

- Provisions related to legal fees and expenses in case of default.

Situations where this form applies

This form is typically used in business contexts where a creditor requires additional security from a third party. It may be needed when a business applies for credit, loans, or financing that could be guaranteed by a personal or corporate entity. This agreement ensures that the creditor has a fallback mechanism to secure debts owed by the debtor.

Who this form is for

- Creditors seeking additional security on business loans.

- Business owners needing to secure financing with a guarantor.

- Guarantors who are willing to limit their liability while backing the debtor.

- Entities involved in business transactions requiring financial assurance.

Completing this form step by step

- Identify the parties involved by filling out the Creditor, Debtor, and Guarantor details.

- Clearly outline the nature of the obligations the Guarantor is agreeing to back.

- Specify the maximum principal amount that the Guarantor will be liable for.

- Include any waivers of notice regarding acceptance and obligations under the guaranty.

- Sign and date the document to formalize the agreement.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, having a notarized document can add an extra layer of legal protection by verifying the identities of the parties involved.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to accurately identify all parties involved.

- Not specifying the limitations of the Guarantor's liability.

- Omitting signatures or dates, which can invalidate the agreement.

- Assuming oral agreements are sufficient alongside the written form.

Why complete this form online

- Convenient access to legal templates that can be easily downloaded and customized.

- Quick editing allows for accurate information input without delays.

- Reliability of forms drafted by licensed attorneys, ensuring legal compliance.

- Availability of guidance from legal experts if needed during completion.

Legal use & context

- This guaranty helps protect the creditor by ensuring another party is liable if the debtor defaults.

- It is enforceable as long as it conforms with contract law principles.

- Limitations and specific provisions can affect the effectiveness and enforceability of the guaranty.

Key takeaways

- The Continuing Guaranty of Business Indebtedness protects creditors by holding guarantors liable for debts incurred by the debtor.

- Properly filling out this form can provide financial security and peace of mind for both lenders and borrowers.

- Review the form carefully to ensure compliance with local laws and to understand the responsibilities it imposes.

Looking for another form?

Form popularity

FAQ

A Guarantor's obligations A guarantor may be bound to maintain repayments on a borrower's loan in circumstances where the borrower defaults on repayments. Alternatively they may be called upon to repay the loan in full.

A limited guarantee is a way to reduce the risks associated with being a guarantor while still receiving the full benefits of a guarantor loan. With this arrangement, the guarantor only secures part of the borrower's mortgage rather than the entire loan amount.

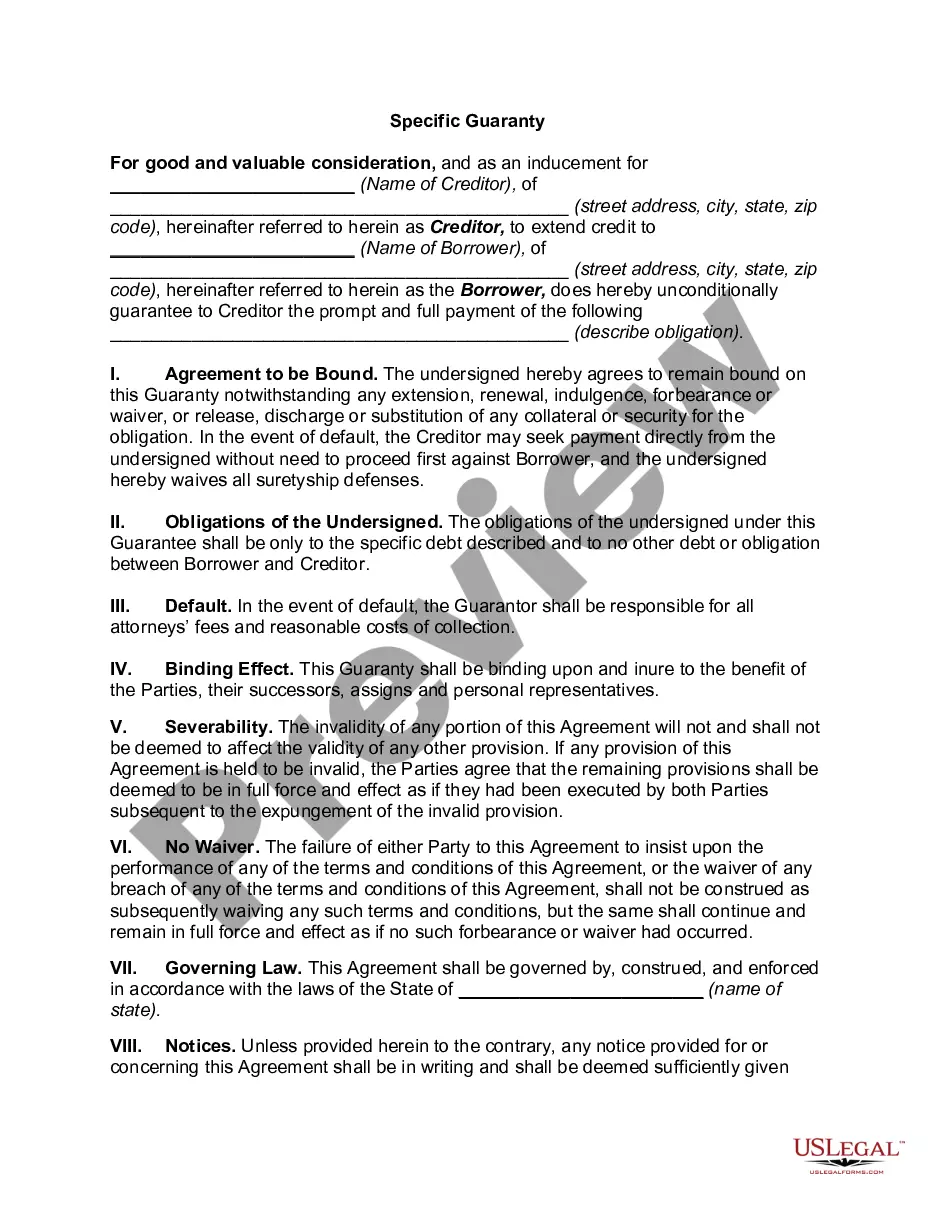

A continuing guaranty is an agreement by the guarantor to be liable for the obligations of someone else to the lender, even if there are several different obligations that are made, renewed or repaid over time. In contrast, a specific guaranty is limited only to one individual transaction.

A limited guarantor may also only be responsible for backing a certain percentage of the loan, referred to as a penal sum. This differs from unlimited guarantors, who are liable for the entire amount of the loan throughout the entire duration of the contract.

You're guaranteeing the full amount for the length of the agreement the tenant is signing for. Tenants often sign up for six to 12 months on a new agreement. After this time there will be rolling notice period, which can vary. As a guarantor, you have full responsibility to pay what's owed.

When your business needs to take out a loan, you, as the owner, may be asked to provide a personal guaranty. This guaranty makes you, as the guarantor, personally responsible for the business debt if it goes into default.

While a co-signer is responsible for the rent at the moment it is due, a guarantor only has to pay once the person on the agreement fails to do so. A guarantor won't have any right to live in the apartment "because you are only going to be liable for anything if the tenant stops paying," says Cohen.

A guarantor is someone who signs a guarantee on behalf of a borrower when they apply for a loan. By doing so, they become legally responsible for paying back the lender if the borrower defaults on the loan. This is different from a co-borrower, who signs a loan with someone and is jointly responsible for repayments.

A guarantor for rent on a residential tenancy is somebody who acts as surety by legally agreeing to take over the financial obligations of the lease in the event that the tenant defaults. This often means that a guarantor is liable for any rent or property damage that the leaseholder has failed to cover.