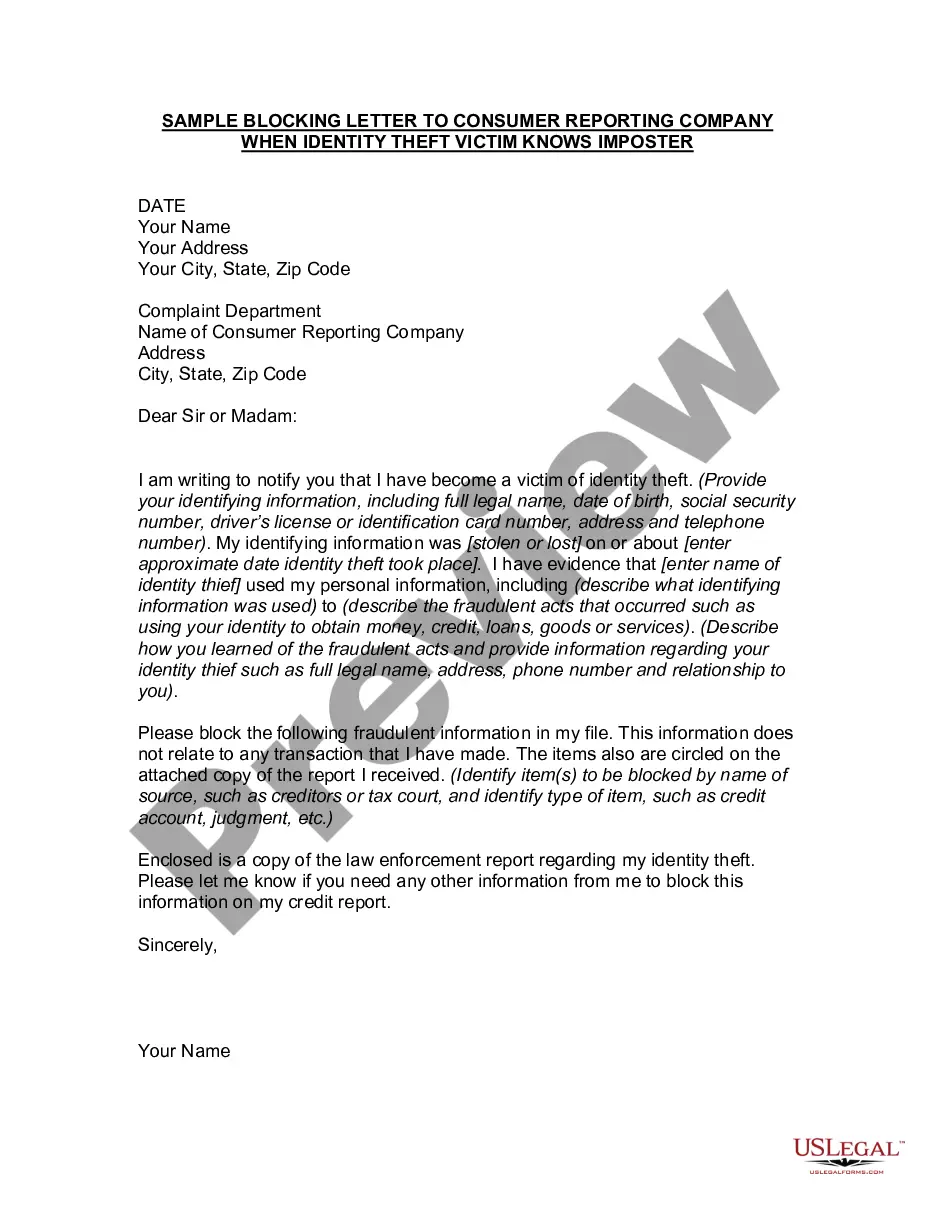

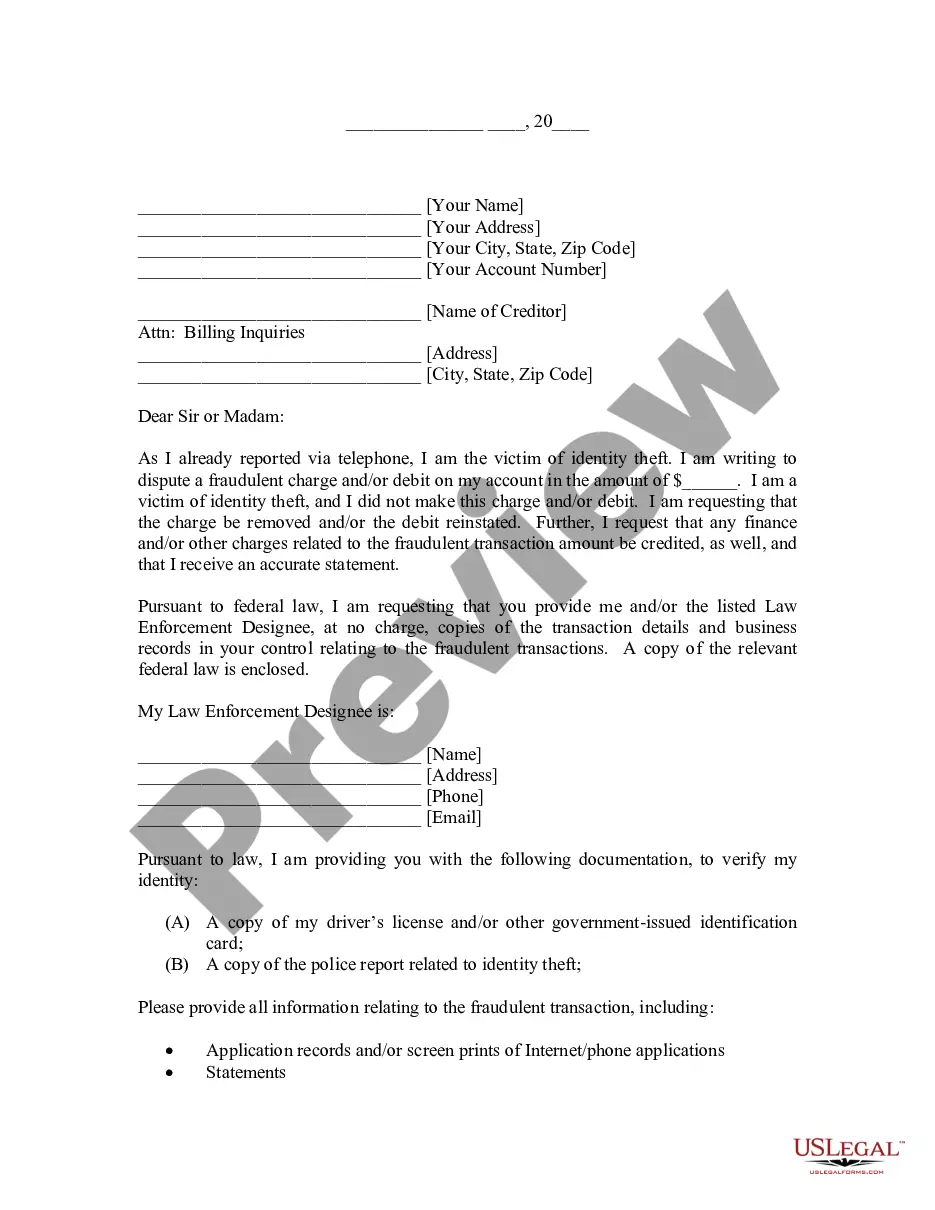

Sample Letter to Credit Reporting Bureau or Agency to Help Prevent Identity Theft

What is this form?

The Sample Letter to Credit Reporting Bureau or Agency to Help Prevent Identity Theft is a legal document used to request a copy of your credit report while taking necessary precautions against identity theft. This letter not only requests your report but also asks the credit bureau to implement protective measures, such as adding a consumer alert and restricting access to your personal information. This form is distinct in that it combines both a request for the credit report and a proactive approach to safeguarding your identity.

Key components of this form

- Date of the request

- Your personal information, including name and address

- Details of the consumer reporting company

- Request for a copy of your credit report

- Actions required to prevent identity theft, including a consumer alert and removal from marketing lists

- Enclosures for verification such as a current utility bill

When this form is needed

You should use this form if you suspect that your credit information may be at risk of misuse or if you want to take proactive steps to protect yourself from identity theft. It is also beneficial after experiencing a data breach or receiving notice of unauthorized transactions. Additionally, this form is helpful if you want to ensure that any creditor must contact you directly before issuing any credit in your name.

Who needs this form

- Individuals concerned about identity theft

- Anyone who has experienced suspicious credit activity

- Consumers who wish to take precautionary measures with their credit reporting

- People looking to obtain a copy of their credit report for review

Instructions for completing this form

- Enter the date at the top of the letter.

- Fill in your full name and current address.

- Add the name and address of the consumer reporting company you are contacting.

- Clearly state your request for your credit report and include any necessary payment.

- List the specific actions you ask the credit bureau to take regarding your file.

- Enclose a current utility bill for address verification and any other specified documents.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. You can complete and submit it as a standard letter to the credit reporting agency.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include payment for the credit report.

- Not specifying the actions requested clearly.

- Omitting necessary personal identification verifications.

- Sending the letter to the incorrect address.

Advantages of online completion

- Convenience of downloading and completing the form at your own pace.

- Editable templates that allow you to fill in your personal information easily.

- Reliable format that complies with legal standards.

- Immediate access to the latest template updates reflecting current laws.

Legal use & context

- The provided template serves as a formal request and is legally recognized.

- Using this form can help establish a record of your communication with the credit bureau.

- Fulfilling the requirements in this letter can enhance your protection against identity theft.

Looking for another form?

Form popularity

FAQ

You may want to enclose a copy of your credit report with the items in question circled. Send your letter by certified mail, return receipt requested, so you can document that the credit bureau received your correspondence. Keep copies of your dispute letter and enclosures.

Password-Protect Your Devices. Use a Password Manager. Watch Out for Phishing Attempts. Never Give Out Personal Information Over the Phone. Regularly Check Your Credit Reports. Protect Your Personal Documents. Limit Your Exposure.

To see if your Social Security number is being used by someone else for employment purposes, review your Social Security Statement at www.socialsecurity.gov/myaccount to look for suspicious activity. Finally, you'll want to use additional scrutiny by regularly checking your bank and credit card accounts online.

Equifax. Equifax.com/personal/credit-report-services. 800-685-1111. Experian. Experian.com/help. 888-EXPERIAN (888-397-3742) Transunion. TransUnion.com/credit-help. 888-909-8872.

You have limited liability for fraudulent debts caused by identity theft. Under most state laws, you're not responsible for any debt incurred on fraudulent new accounts opened in your name without your permission. Under federal law, the amount you have to pay for unauthorized use of your credit card is limited to $50.

Check all your financial accounts for errors or suspicious activity. Enroll in a credit monitoring service. Place a fraud alert on your credit reports. Consider freezing your credit. Alert the authorities. Always use strong passwords and be aware of information you give out.

Here's the truth about a 609 letter: they absolutely do work in many cases. But, just like with credit report disputes, there's no guarantee it will actually work.

The cost of identity theft protection is a personal expense and is not tax deductible.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.