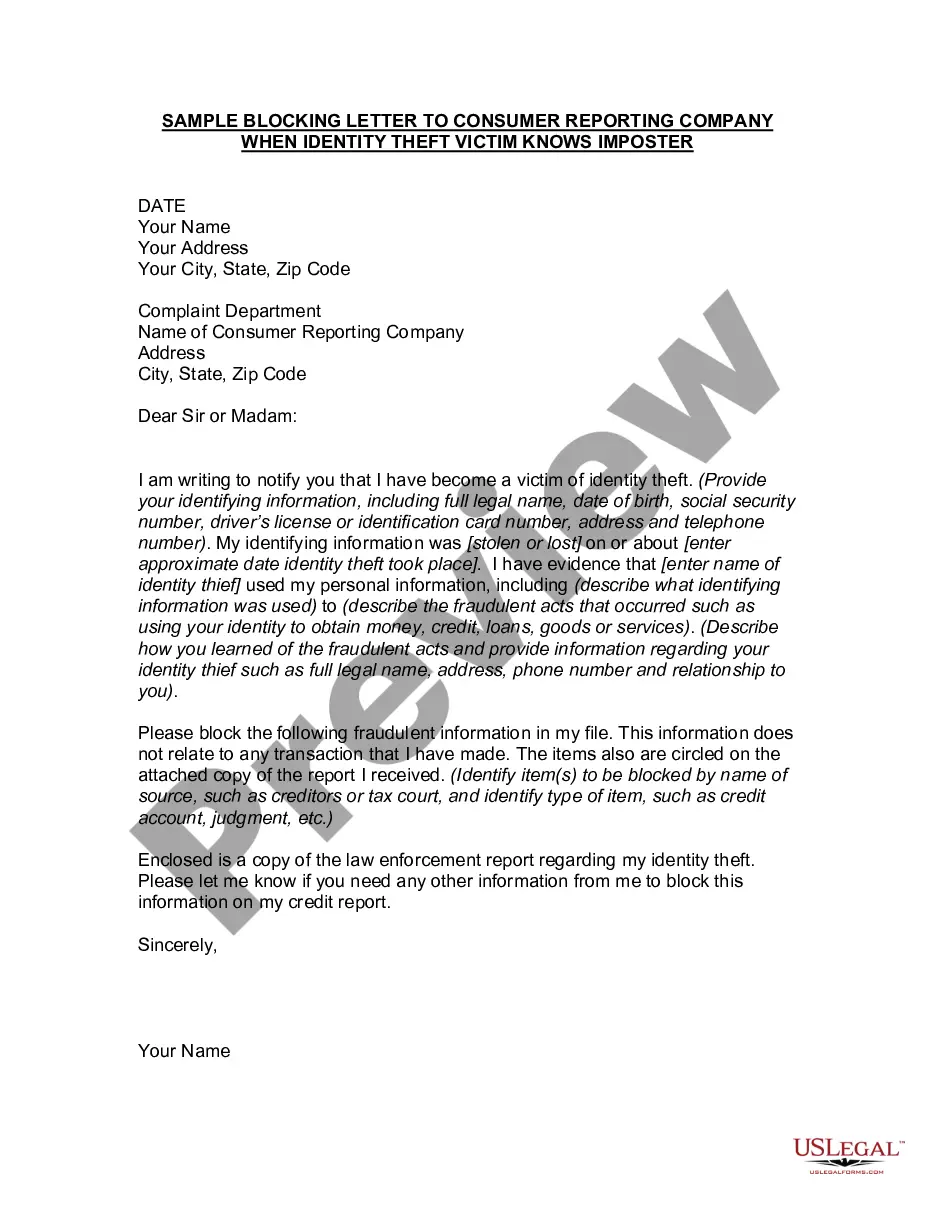

Reporting Company

Description Sample Letter To Credit Bureau To Report Death

How to fill out How To Write A Letter To Credit Bureau?

Aren't you sick and tired of choosing from hundreds of samples every time you want to create a Letter to Credit Reporting Company or Bureau Regarding Known Imposter Identity Theft? US Legal Forms eliminates the wasted time countless American citizens spend surfing around the internet for suitable tax and legal forms. Our expert crew of attorneys is constantly changing the state-specific Samples collection, to ensure that it always offers the appropriate files for your scenarion.

If you’re a US Legal Forms subscriber, just log in to your account and click on the Download button. After that, the form can be found in the My Forms tab.

Visitors who don't have a subscription should complete a few simple actions before having the ability to get access to their Letter to Credit Reporting Company or Bureau Regarding Known Imposter Identity Theft:

- Make use of the Preview function and look at the form description (if available) to make sure that it is the appropriate document for what you are looking for.

- Pay attention to the applicability of the sample, meaning make sure it's the correct template for your state and situation.

- Make use of the Search field at the top of the web page if you want to look for another file.

- Click Buy Now and choose a preferred pricing plan.

- Create an account and pay for the services using a credit card or a PayPal.

- Download your sample in a convenient format to complete, print, and sign the document.

When you have followed the step-by-step guidelines above, you'll always have the capacity to log in and download whatever document you will need for whatever state you need it in. With US Legal Forms, finishing Letter to Credit Reporting Company or Bureau Regarding Known Imposter Identity Theft samples or any other legal paperwork is not difficult. Get started now, and don't forget to recheck your examples with accredited attorneys!