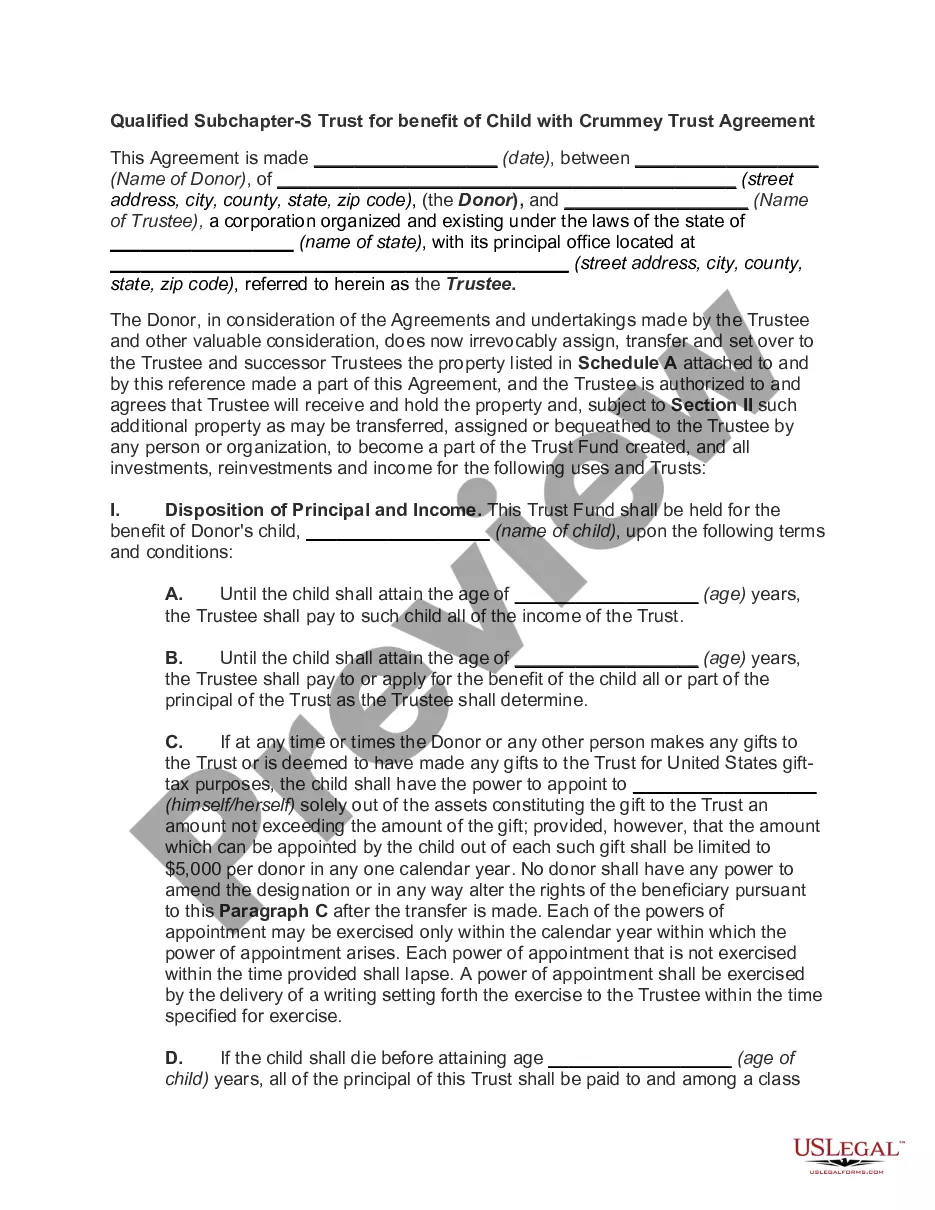

Sprinkling Trust for Children During Grantor's Life, and for Surviving Spouse and Children after Grantor's Death - Crummey Trust Agreement

What this document covers

This form is a Sprinkling Trust for Children During Grantor's Life, often referred to as a Crummey Trust Agreement. It is an irrevocable trust designed to provide financial support for the grantor's minor children during their lifetime and for the surviving spouse and children after the grantor's death. This trust includes special provisions known as Crummey Powers, allowing beneficiaries to withdraw contributions for a limited time, which helps qualify these contributions for the annual federal gift tax exclusion. This trust setup is particularly beneficial for those looking to manage their estate and protect assets while minimizing tax liabilities.

What’s included in this form

- Identification of parties involved, including the grantor and co-trustees.

- Specification of primary beneficiaries who will benefit from the trust.

- Establishment of rights for beneficiaries to withdraw funds under certain conditions.

- Distribution guidelines for both during and after the grantor's lifetime.

- Provisions for managing and investing trust assets by the trustees.

- Terms regarding the irrevocability of the trust and powers of the trustee.

Common use cases

This form should be used when an individual seeks to establish a trust to support their minor children while providing ongoing financial security for the spouse and adult children after their death. It is particularly useful for parents who want to ensure that asset distributions are managed and controlled according to their wishes, providing for the needs of their family members in a structured manner while potentially minimizing tax exposure.

Who can use this document

- Parents or guardians wishing to create a trust for the benefit of their children.

- Individuals concerned about ensuring financial support for a surviving spouse.

- Those looking to manage their estate efficiently while taking advantage of gift tax exclusions.

- Families with minor children who want to provide inheritance in a structured manner.

How to complete this form

- Identify and enter the names and addresses of the grantor and co-trustees.

- Specify the primary beneficiaries of the trust, including their dates of birth and relationship to the grantor.

- Outline the initial contributions to the trust and any additional properties or assets to be included.

- Detail the distribution preferences and guidelines for the trustee regarding income and principal management.

- Sign and date the document, ensuring all involved parties acknowledge their roles.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, having the document notarized can add an extra layer of authenticity and may be beneficial in ensuring its acceptance by financial institutions or for regulatory purposes.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to clearly identify all parties involved, particularly co-trustees.

- Overlooking the specific rights granted to beneficiaries regarding withdrawals.

- Not specifying distribution preferences adequately, leading to potential disputes later.

- Neglecting to keep the list of trust properties updated as assets change.

Benefits of using this form online

- Convenient access to legal documents tailored to individual needs.

- Editability allows users to customize trust details before finalizing.

- Reliability ensured by having templates drafted by licensed attorneys.

- Quick downloads save time compared to traditional legal routes.

- The trust agreement is legally binding once properly executed by all involved parties.

- Beneficiaries' rights to trust assets must comply with the specific provisions outlined in the trust.

- The irrevocability of the trust means that once established, the terms cannot be altered or revoked easily by the grantor.

What to keep in mind

- The Crummey Trust Agreement allows for strategic tax benefits while providing for minor children and a surviving spouse.

- This form contains specific withdrawal rights for beneficiaries, making it unique among trust options.

- Proper completion of this form is crucial to ensure its legality and effectiveness.

Looking for another form?

Form popularity

FAQ

There can also be tax advantages to a sprinkling trust: Beneficiaries pay income taxes on the trust funds they receive. If the beneficiaries are in widely different tax brackets, the trustee may be able to keep more trust money in the family by distributing more to the beneficiaries in the lower tax brackets.

In the case of a good Trustee, the Trust should be fully distributed within twelve to eighteen months after the Trust administration begins. But that presumes there are no problems, such as a lawsuit or inheritance fights.

Administering a living trust after your death is not cost-free. Even if probate is avoided, the successor trustee should usually seek help from a lawyer in making sure that your debts are paid, all of the necessary tax forms filed and the assets in your trust legally distributed to your beneficiaries.

The procedure for settling a trust after death entails: Step 1: Get death certificate copies. Step 2: Inventory the assets in the estate. Step 3: Work with a trust attorney to understand the grantor's distribution wishes, timelines, and fiduciary responsibilities. Step 4: Asset appraisal. Step 5: Pay taxes.

Yes, the surviving spouse may serve as trustee of the credit shelter trust.All of the assets in the credit shelter trust, including any appreciation in value during the surviving spouse's lifetime, pass free of estate tax to the beneficiaries.

A marital trust starts as a revocable living trust. A surviving spouse can be its trustee.

Some trusts are set up so that on the death of the Life Tenant, the trust assets remain held in discretionary trusts for a range of beneficiaries. It is then up to the Trustees to decide which beneficiaries receive trust assets, and when this happens.

Most Trusts take 12 months to 18 months to settle and distribute assets to the beneficiaries and heirs.

One of the main tasks of the successor trustee is to distribute the assets of the trust to the designated beneficiaries.