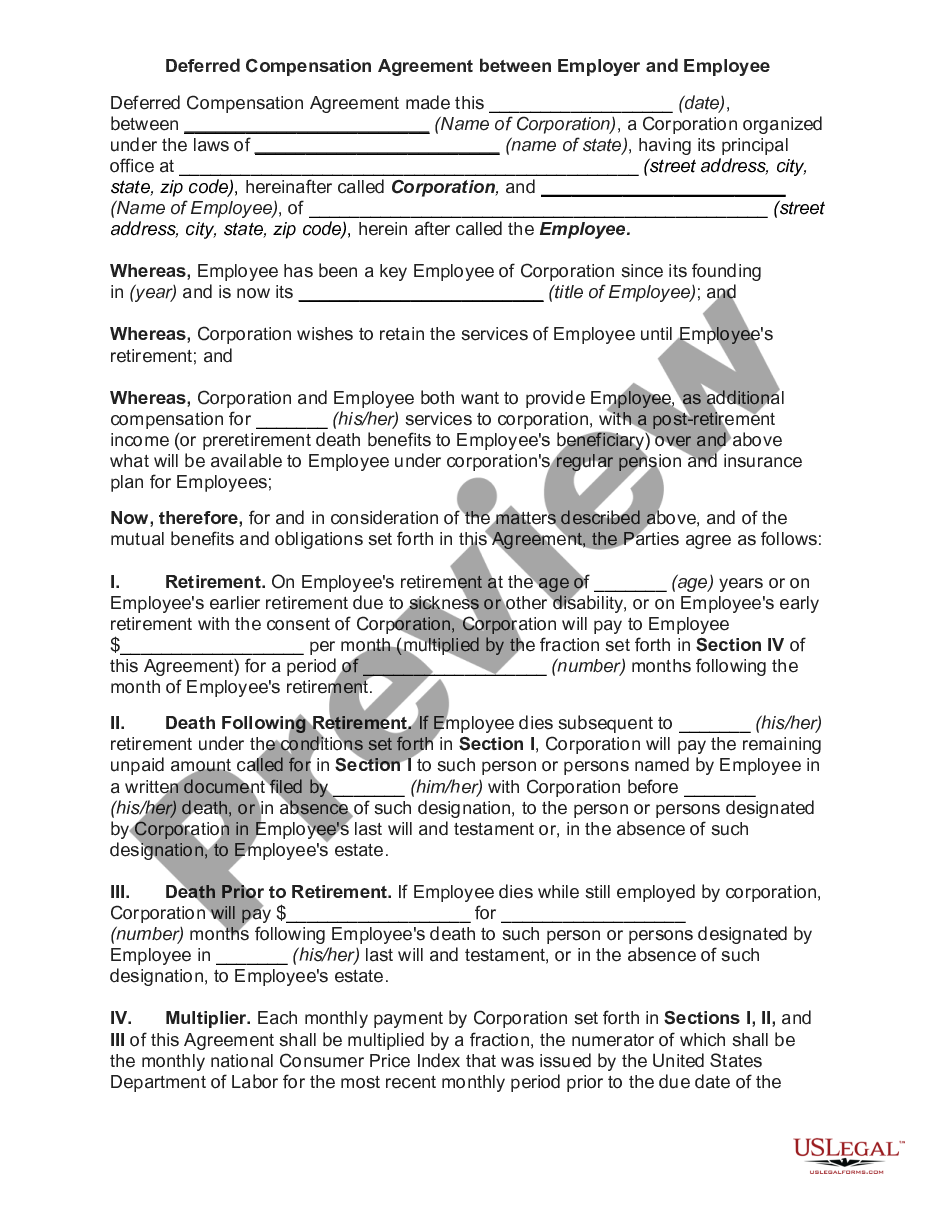

Deferred Compensation Agreement - Short Form

About this form

A Deferred Compensation Agreement is a legal document that outlines an arrangement where part of an employee's income is paid at a future date, usually after retirement. This type of agreement is important for both employees and employers as it provides a method for employees to earn additional income post-retirement while deferring tax liability. Unlike standard employment contracts, a Deferred Compensation Agreement allows for compensation to be received after services have been rendered, often tailored to assist with financial planning during retirement.

Form components explained

- Identification of the employer and employee involved in the agreement.

- Terms of the deferred compensation, including the amount and payment schedule.

- Conditions under which payments will begin, such as retirement, disability, or other agreed-upon events.

- Provisions regarding the security of compensation, ensuring obligations are outlined.

- Signatures of both parties to validate the agreement.

When to use this document

This form is typically used when an employer wishes to provide an incentive for an employee or independent contractor to remain with the company until retirement or when certain conditions arise. It is ideal for organizations looking to plan for employee retention, particularly in cases where they anticipate the employee's contributions will be beneficial until retirement. It may also be relevant for personal financial planning to optimize tax liabilities associated with future income.

Who needs this form

- Employers seeking to incentivize employee retention until retirement.

- Employees or independent contractors who wish to arrange for post-retirement income.

- Human resource professionals managing employee compensation packages.

Instructions for completing this form

- Identify the parties involved by entering the names of the employer and employee.

- Specify the amount of deferred compensation to be paid and the timeline for payments.

- Detail the conditions that will trigger the commencement of payments.

- Include any clauses regarding the security of the deferred compensation.

- Sign and date the agreement at the end to finalize it.

Is notarization required?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly specify the conditions under which payments begin.

- Not detailing the payment amounts and schedule accurately.

- Neglecting to obtain signatures from all parties involved.

Benefits of using this form online

- Convenience of accessing and customizing the form from anywhere at any time.

- Editability allows users to tailor the agreement to their specific needs.

- Reliable resources ensure the form is compliant with current legal standards.

Main things to remember

- The Deferred Compensation Agreement is essential for planning post-retirement income.

- It encourages employee retention by providing incentives tied to future payments.

- Proper completion is crucial to ensure legal enforceability and compliance with applicable laws.

Looking for another form?

Form popularity

FAQ

A Deferred Compensation Agreement - Short Form is a legal document that records an arrangement where part of an employee’s income is paid at a future date, usually after retirement. It helps employers retain key staff and gives employees post-retirement income while deferring some tax liability. The short form focuses on essential terms and signatures.

Payout occurs according to the agreement’s terms: the amount and payment schedule are defined in the contract, and payments typically begin when a specified event occurs, such as retirement or disability, or another mutually agreed event. The document sets the timing and method, ensuring a clear payment path.

An example is an employer promising to pay a fixed amount annually starting at retirement, with the exact dollar amount and schedule spelled out in the contract. This ensures the employee receives post-retirement income while the employer’s obligation and payout timing are clearly defined.

The form does not prescribe a universal percentage; the amount is negotiated between the employer and the employee and documented in the agreement. It should align with retirement planning, tax considerations, and the company’s compensation strategy. People typically tailor it to long-term goals and cash flow.

In general, taxes are due when the deferred amount is paid, not when it's earned. The Deferred Compensation Agreement - Short Form defers tax liability until payout according to the agreement’s terms. Consult a licensed tax professional for guidance on your situation.

The Short Form covers core elements only—employer and employee identification, the amount and payment schedule, payout conditions, security provisions, and signatures—providing a streamlined document. A longer version would typically include additional terms or customization beyond these essential components. This difference matters for users seeking a quick deployment or simpler review, while lawyers might seek broader language in a full form to address unusual scenarios or risk management.