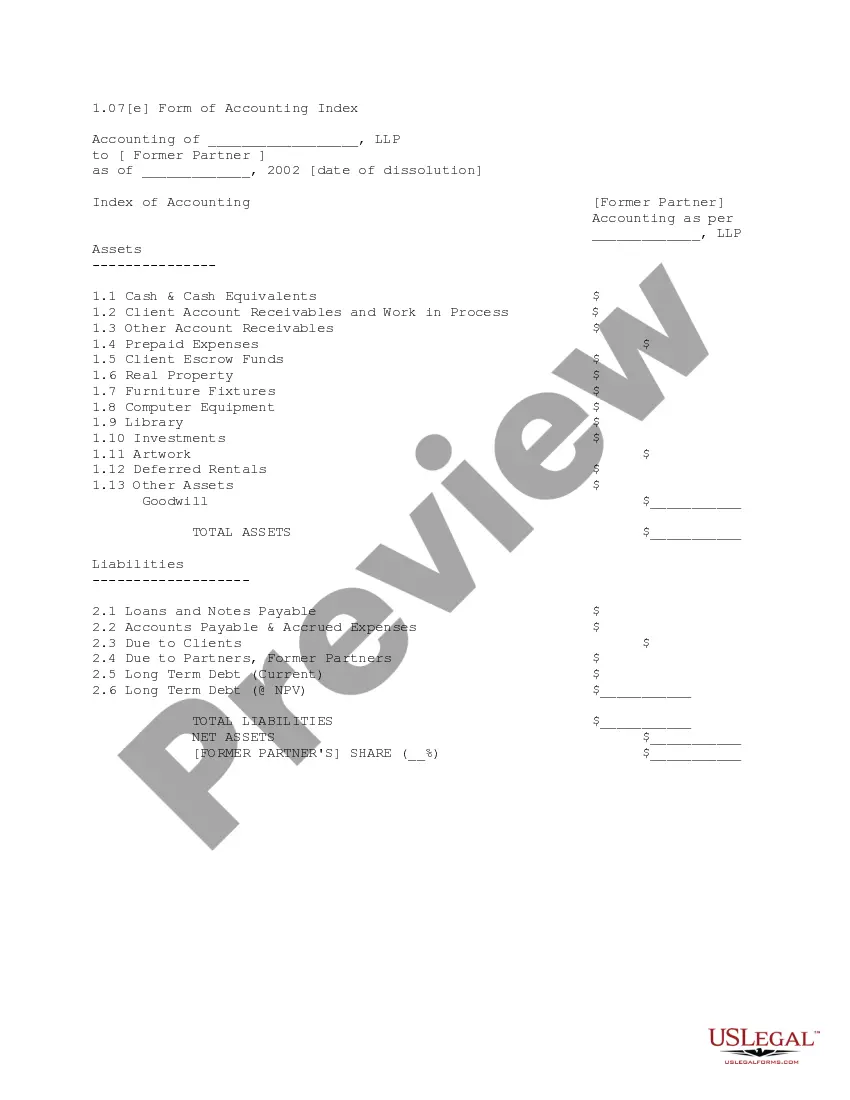

Anchorage Alaska Profit and Loss Statement

Category:

State:

Multi-State

City:

Anchorage

Control #:

US-SB-6

Format:

Word;

Rich Text

Instant download

Description

Profit and Loss Statement: This is a general Statement of Profits and Losses for a company. It lists in detail, all profits, or gains, as well as all losses the business may have suffered. This form can be used by any type of company, whether a corporation or a sole proprietor.