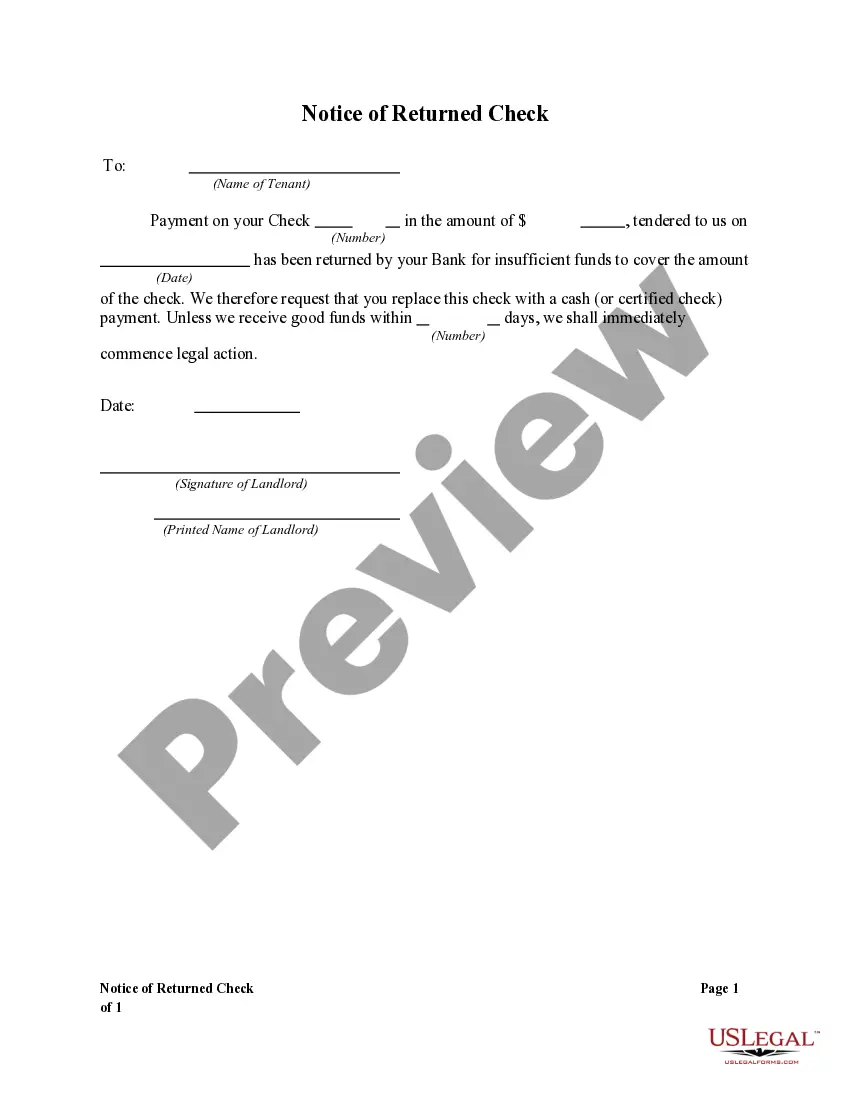

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

Middlesex Massachusetts Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

County:

Middlesex

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

Drafting legal documents can be challenging.

Moreover, if you choose to engage a lawyer to create a business contract, paperwork for ownership transfer, premarital arrangement, divorce documentation, or the Middlesex Notice to Debt Collector - Submitting a Postdated Check Before the Scheduled Date, it might cost you a significant amount.

Peruse the page and confirm there is a template for your area.

- So what is the most practical method to conserve time and funds while generating valid forms that fully adhere to your state and local statutes and regulations.

- US Legal Forms is an ideal solution, regardless if you seek templates for personal or commercial purposes.

- US Legal Forms boasts the largest online collection of state-specific legal documents, offering users with the current and professionally validated forms for any application gathered all in one location.

- Thus, if you require the most recent edition of the Middlesex Notice to Debt Collector - Submitting a Postdated Check Before the Scheduled Date, you can effortlessly locate it on our platform.

- Acquiring the documents takes a minimal amount of time.

- Individuals who already possess an account should verify their subscription status, Log In, and choose the template using the Download button.

- If you have yet to subscribe, here's how you can obtain the Middlesex Notice to Debt Collector - Submitting a Postdated Check Before the Scheduled Date.

Form popularity

FAQ

Post-dated checks are perfectly legal. If they weren't, pay day lenders, and other crude forms of credit, couldn't exist. Only properly payable checks are supposed to be cashed by banks. But just about anything with the right signature on it is properly payable, including post-dated and overdrawn checks.

Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice. Contact your bank or credit union to learn what its policies are.

It is legal for an individual to postdate a check, as well as for a bank to cash or deposit it.

The FDCPA says that it's illegal for a debt collector to take a check that is postdated by more than five days, unless the consumer is notified in writing of the debt collector's intent to deposit the check between 10 and three days prior to the deposit.

In most cases, when you receive a postdated check, you can deposit or cash a postdated check at any time. Debt collectors may be prohibited from processing a check before the date on the check, but most individuals are free to take postdated checks to the bank immediately.

Postdated checks can usually be cashed or deposited at any time unless the person who wrote the check specifically told their bank not to honor the check until a certain date. Rather than writing a postdated check, it may be better to use online payment services or coordinate with your biller to move back the due date.

A signed check immediately becomes legal tender that a bank can deposit or cash before the indicated date on the check. Therefore, a bank will be able to accept a check if it is dated and signed. Ask your bank or credit union for their specific policy for postdated checks in their account disclosures.

Although it is legal to post-date a check, the bank to which the check is presented for payment may charge the payor's account even before the date of the check and even if doing so creates an overdraft.

A signed check immediately becomes legal tender that a bank can deposit or cash before the indicated date on the check. Therefore, a bank will be able to accept a check if it is dated and signed. Ask your bank or credit union for their specific policy for postdated checks in their account disclosures.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.