How to execute a deed with mortgage assumption effectively

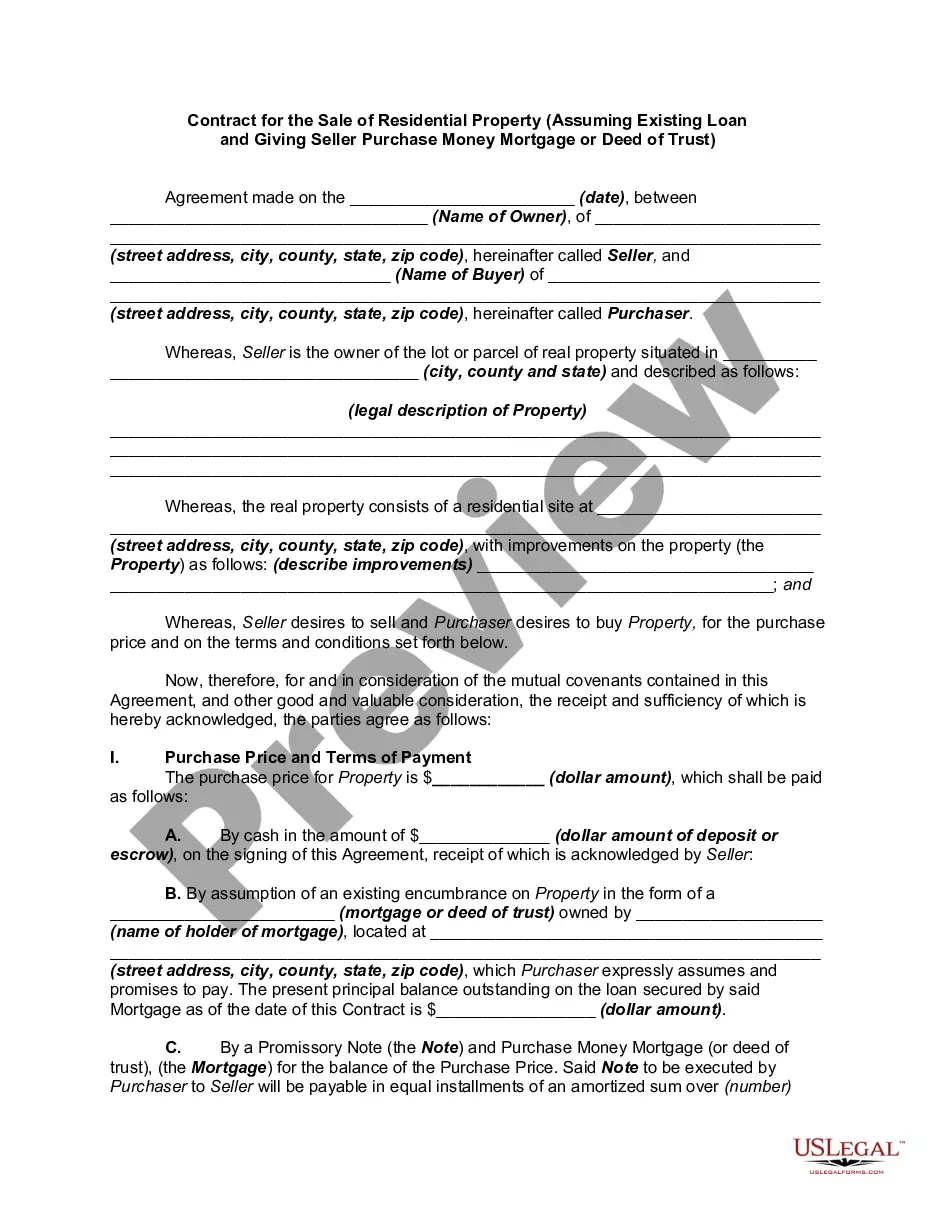

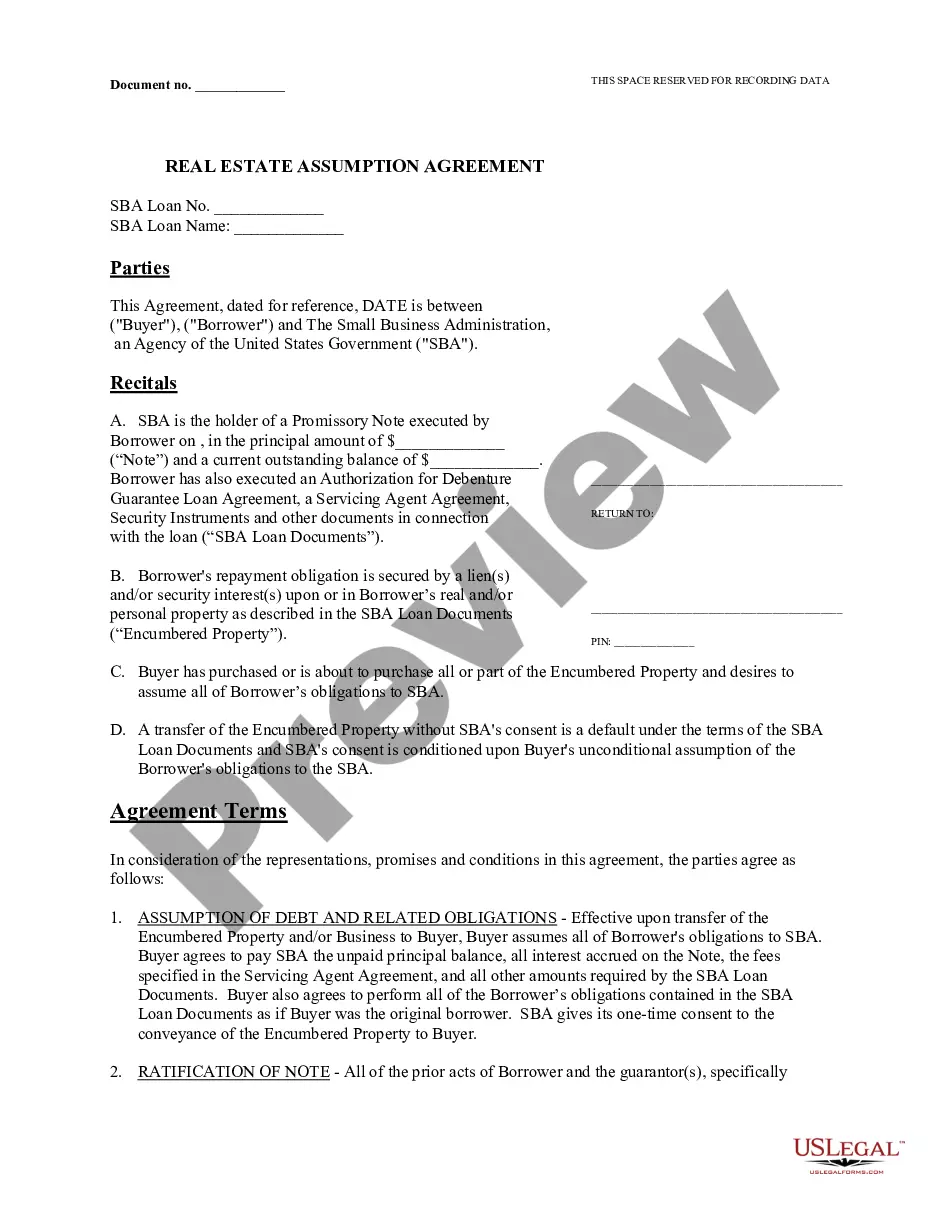

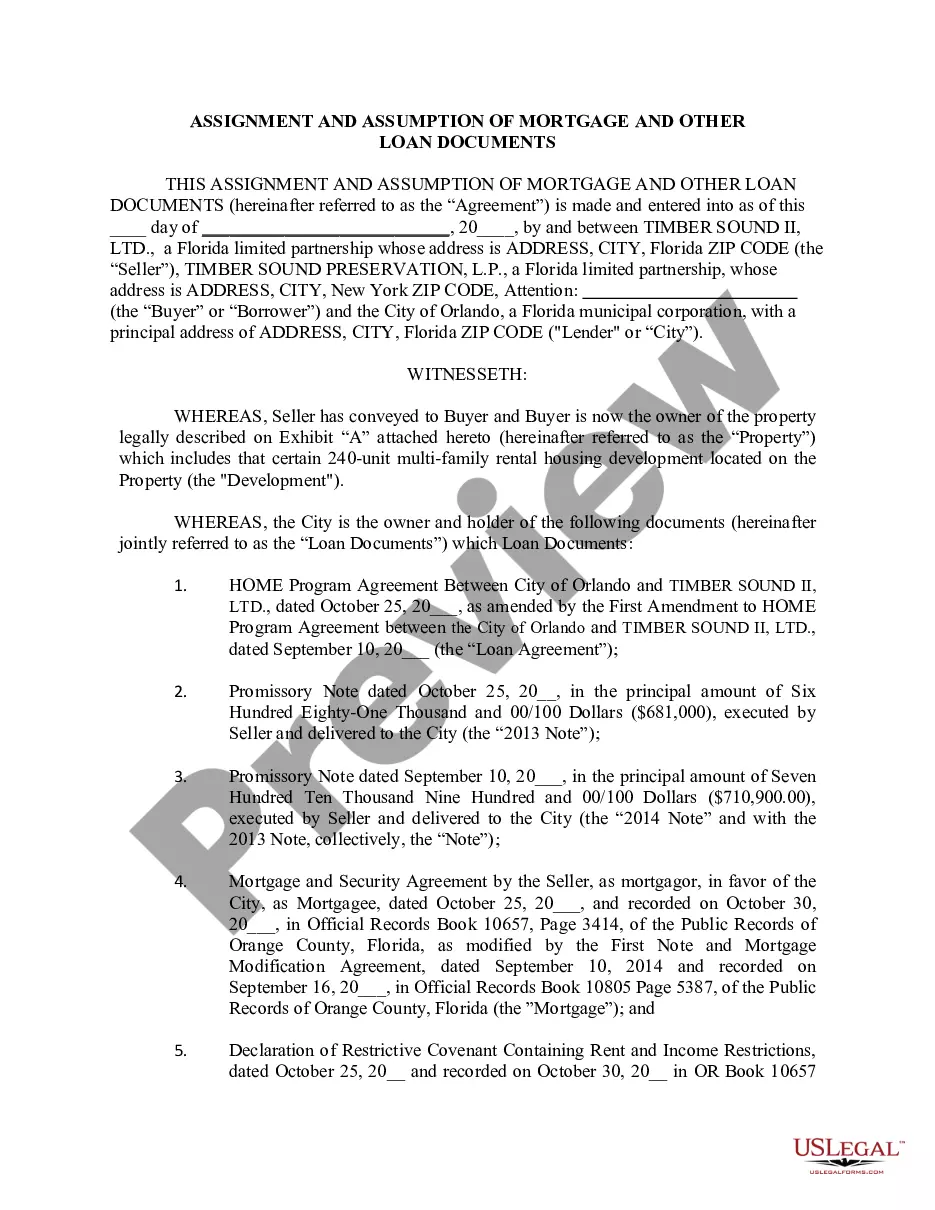

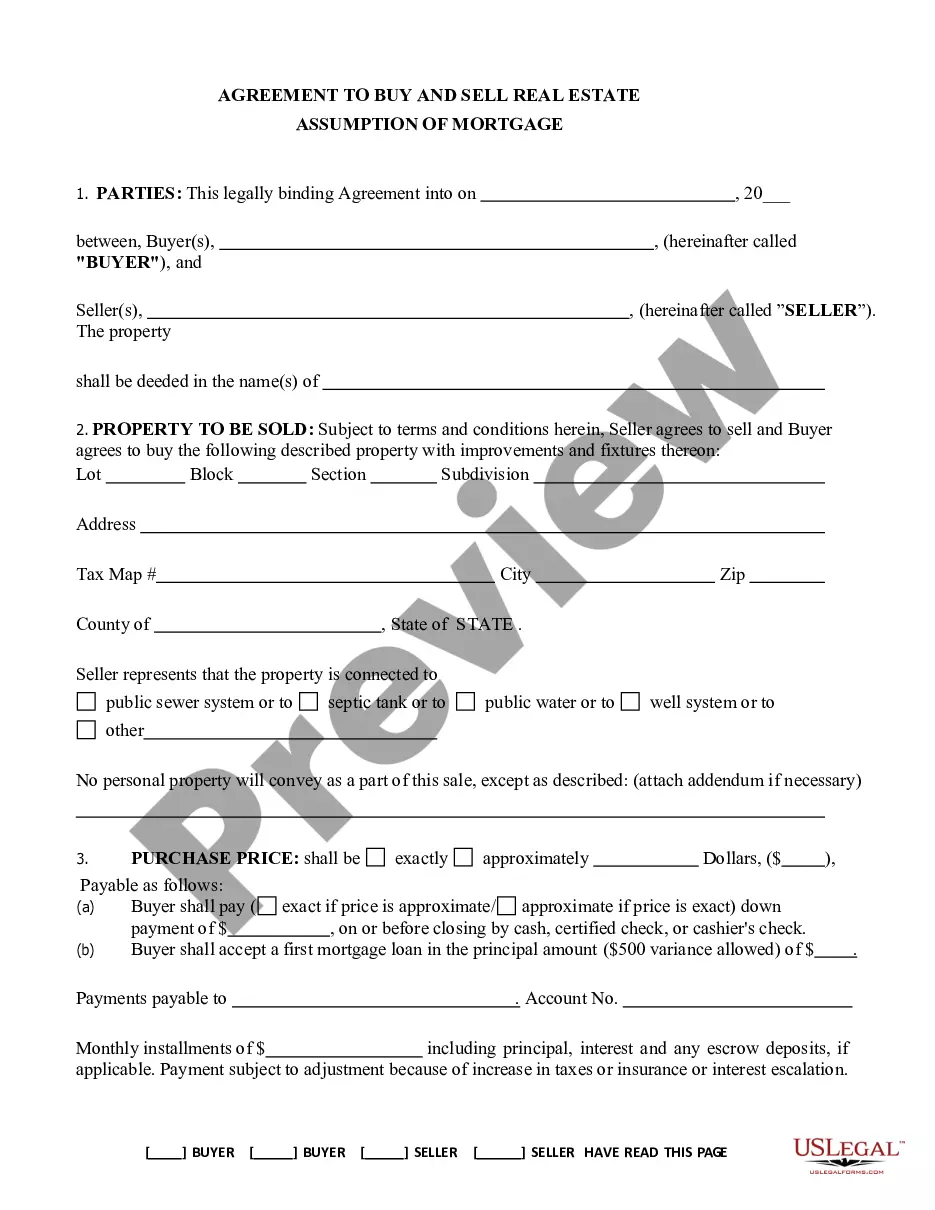

A deed with mortgage assumption is a legal document that transfers ownership of real property while allowing the buyer (grantee) to assume the mortgage obligations of the seller (grantor). This means the grantee agrees to take over the mortgage payments and is responsible for the remaining mortgage debt. Such deeds are commonly used in real estate transactions where property owners want to sell their homes without requiring the buyer to secure a new mortgage.

How to complete a form

To execute a deed with mortgage assumption, follow these steps:

- Begin by identifying the parties involved, including the grantor (current owner) and grantee (buyer).

- Clearly describe the property being transferred, including its legal description.

- Indicate the consideration, which is often a nominal amount, to validate the transaction.

- Include the mortgage details the grantee will assume, specifying the lender and the amount owed.

- Both parties should sign the document in the presence of a notary public to ensure legal validity.

Who should use this form

This form is suitable for individuals involved in real estate transactions where one party wishes to buy property and take over an existing mortgage. Common users include:

- Homebuyers looking for a straightforward way to purchase property.

- Property owners aiming to sell while retaining existing financing.

- Investors who are assessing properties with existing mortgage obligations.

Key components of the form

A deed with mortgage assumption typically includes the following components:

- Identification of parties: Names and addresses of the grantor and grantee.

- Description of property: A clear legal description of the property being transferred.

- Consideration: A statement of the amount exchanged for the property.

- Mortgage specificities: Details about the mortgage being assumed, including amount and lender.

- Signatures: Required signatures of both parties and a notary acknowledgment for legal validation.

Common mistakes to avoid when using this form

When using the deed with mortgage assumption, be mindful of the following common errors:

- Failing to accurately describe the property involved, leading to potential disputes.

- Not including necessary signatures or notary acknowledgment, rendering the document invalid.

- Overlooking specific mortgage details, which could affect the assumption process.

- Neglecting to have the form reviewed by a legal professional to ensure compliance with local laws.

What documents you may need alongside this one

In addition to the deed with mortgage assumption, you may need to prepare or gather the following documents:

- Mortgage statement: Current statement from the lender detailing the mortgage balance.

- Title search report: To confirm the property title is clear of other claims.

- Notary acknowledgment form: To ensure the signatures are validly witnessed.

- Purchase and sale agreement: If this transaction is part of a larger real estate deal.

What to expect during notarization or witnessing

During the notarization process, the following typically occurs:

- The grantor and grantee present valid identification to the notary.

- Both parties sign the deed in the presence of the notary.

- The notary will complete the acknowledgment section, sign, and affix their seal to the document.

- This process ensures the authenticity of signatures and prevents fraudulent claims.