West Virginia Owner Financing Contract for Moblie Home

Description

How to fill out Owner Financing Contract For Moblie Home?

In the event you must obtain thorough, procure, or generate legal document templates, utilize US Legal Forms, the finest range of legal forms available online.

Take advantage of the site's user-friendly and convenient search feature to find the documents you need.

Various templates for business and personal purposes are categorized by types and jurisdictions, or keywords.

Step 4. Once you have located the form you need, click the Buy now button. Choose your preferred pricing plan and enter your details to register for the account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the payment.

- Utilize US Legal Forms to acquire the West Virginia Owner Financing Agreement for Mobile Home in just a few clicks.

- If you are an existing US Legal Forms client, Log In to your account and select the Download button to retrieve the West Virginia Owner Financing Agreement for Mobile Home.

- You can also access forms you have previously saved in the My documents section of your account.

- If this is your first time using US Legal Forms, follow these steps.

- Step 1. Ensure you have selected the form for the correct state/country.

- Step 2. Use the Preview option to review the content of the form. Don't forget to read the details.

- Step 3. If you are not happy with the form, use the Search bar at the top of the screen to find alternative versions of the legal form template.

Form popularity

FAQ

Setting up a seller financing deal begins with determining the terms that will attract buyers while protecting your interests as a seller. Draft a West Virginia Owner Financing Contract for Mobile Home that includes a clear repayment plan, interest rates, and any contingencies. Transparency during negotiations can foster trust. Utilizing a service like uslegalforms can simplify the process by offering templates tailored to your specific needs.

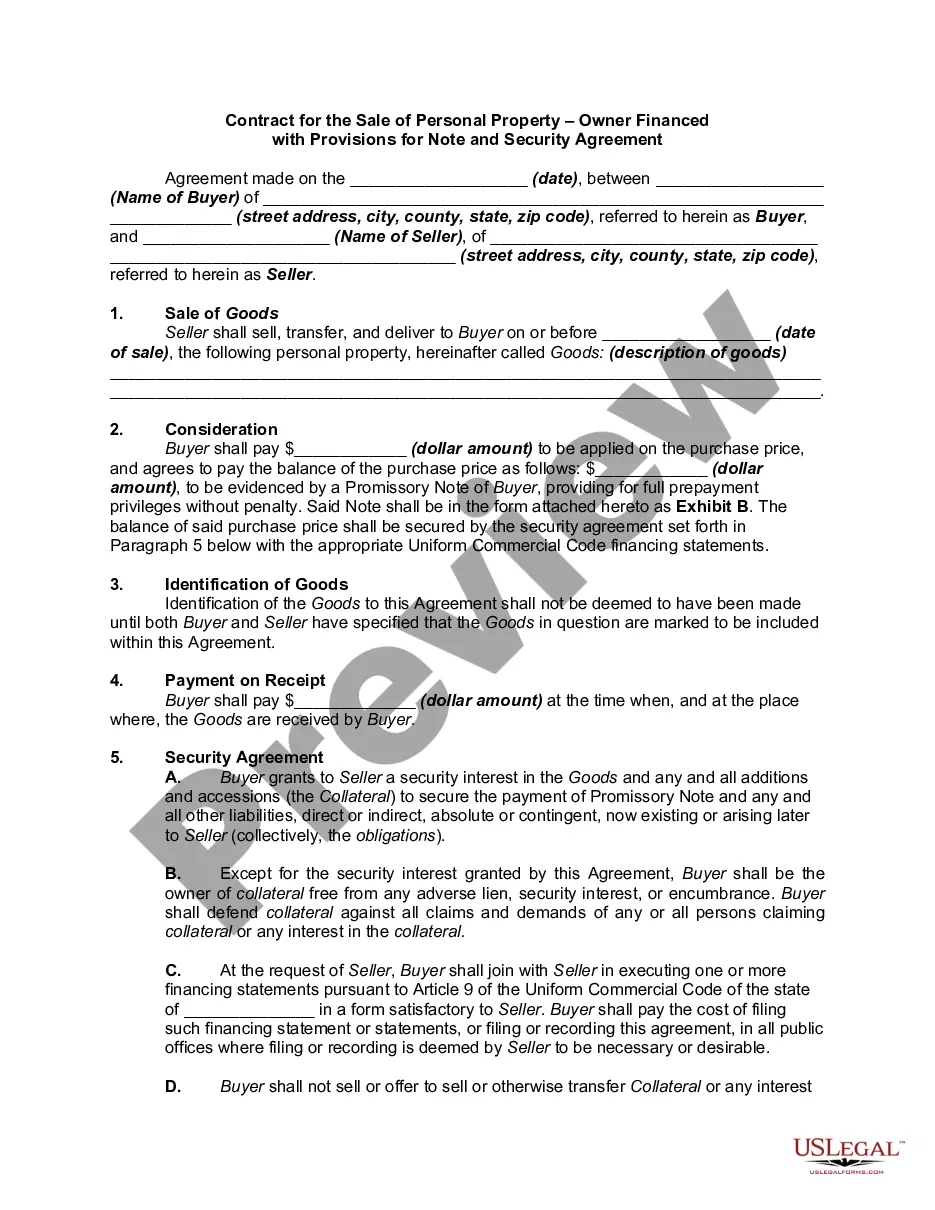

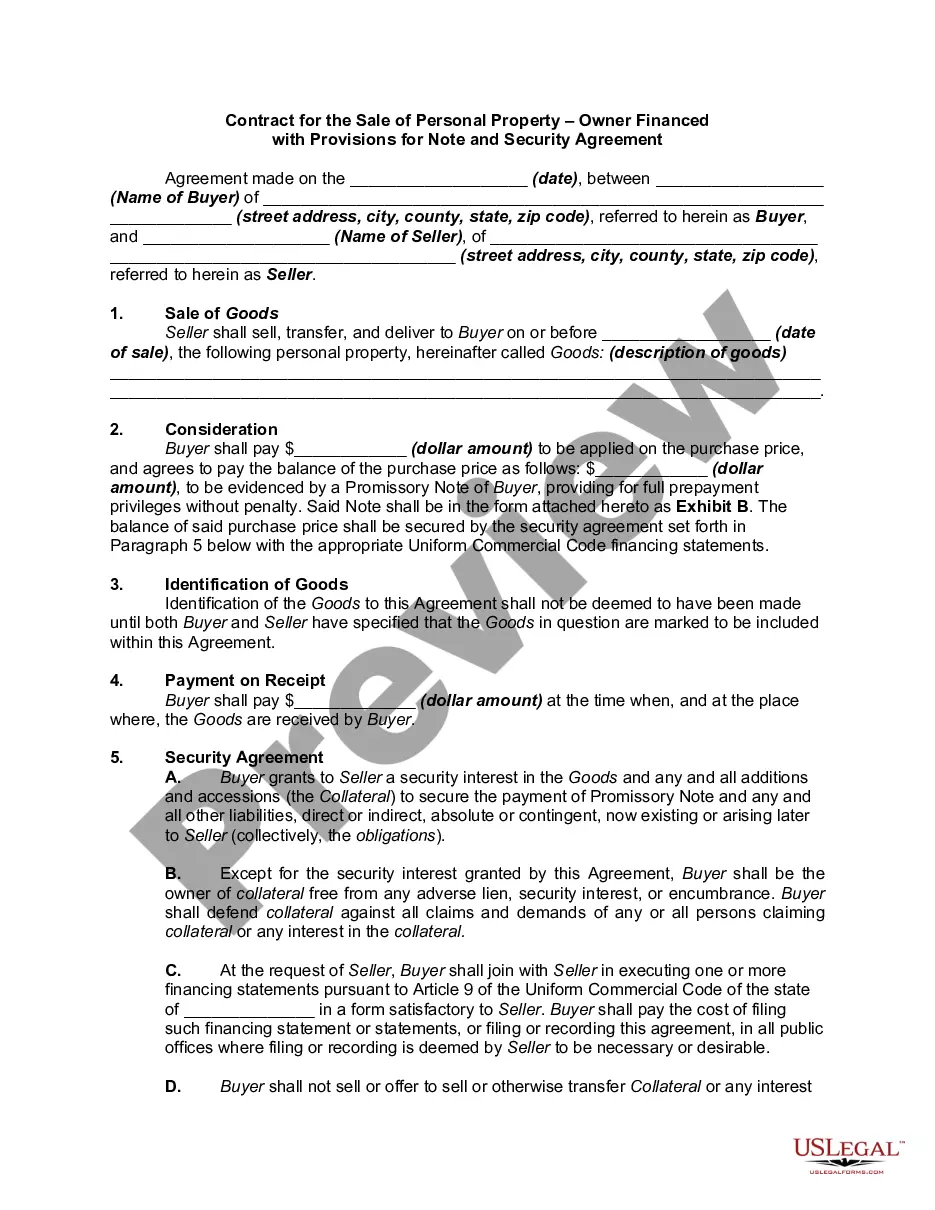

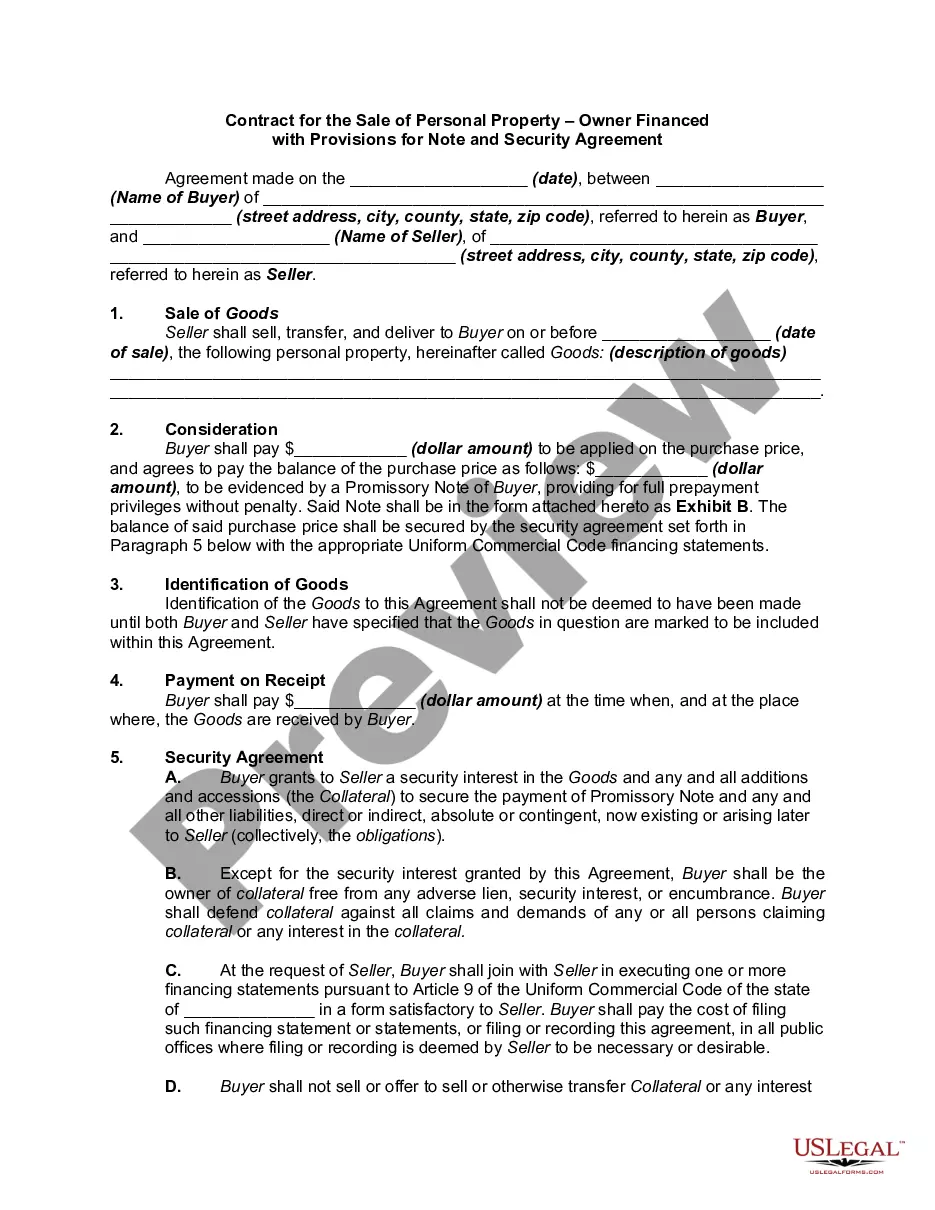

Seller financing terms vary, but they often include a down payment, interest rate, and repayment schedule. In a West Virginia Owner Financing Contract for Mobile Home, sellers might expect a down payment of 10-20%, with monthly payments over a period of 5 to 30 years. The interest rates typically align with local market rates, making this option appealing to both buyers and sellers. Flexible terms can be tailored to fit both parties’ needs.

In West Virginia, a land contract, which is often used in owner financing situations, is not legally required to be recorded. However, recording the contract can provide protection to the buyer's interests. It creates a public record, which helps secure the buyer's claim to the property under a West Virginia Owner Financing Contract for Mobile Home.

An owner finance contract specifically allows a seller to finance the sale of their mobile home directly to the buyer. This contract details the payment schedule, interest rates, and any other relevant terms of the financing arrangement. It's particularly useful in West Virginia, as it opens up possibilities for those who might struggle with conventional loans.

While traditional lenders often look for higher credit scores, owner financing offers more leeway. In a West Virginia Owner Financing Contract for Mobile Home, sellers may be willing to accept lower credit scores because they evaluate other factors too. This approach allows buyers with less-than-perfect credit to still achieve home ownership. It's important to discuss your situation with potential sellers to find the best possible financing terms.

Owner financing terms can vary widely depending on the arrangement, but generally, they may include a down payment, monthly payments, and an interest rate. In a West Virginia Owner Financing Contract for Mobile Home, you might expect terms that range from a few years to several decades. Many sellers offer options that make it easier for buyers to manage their finances. Always clarify the specifics with the seller to ensure you understand the agreement.

Securing financing for a manufactured home, particularly through a West Virginia Owner Financing Contract for Mobile Home, can vary depending on several factors. It often proves easier than traditional loans since owner financing allows for more flexible terms. Borrowers can work directly with the seller to negotiate payments and interest rates. This can be particularly beneficial for buyers who may have trouble obtaining conventional financing.

Banks often hesitate to finance mobile homes due to their classification as personal property and potential depreciation. This can lead to additional risk for lenders. However, using a West Virginia Owner Financing Contract for Mobile Home allows buyers to bypass traditional financing hurdles, providing a direct path to purchasing a home without bank involvement.

Typically, a down payment for a land contract is not strictly necessary, but it is common. Sellers may require a down payment to ensure buyer commitment. When using a West Virginia Owner Financing Contract for Mobile Home, discussions can take place to either establish a minimal down payment or explore alternative arrangements that can suit both parties.

The lowest down payment for a mobile home can be as low as 3% to 5%, depending on the financing options available. However, owner financing may allow for lower down payment options in your agreement. A West Virginia Owner Financing Contract for Mobile Home provides flexibility in down payment negotiations, making home ownership more accessible.