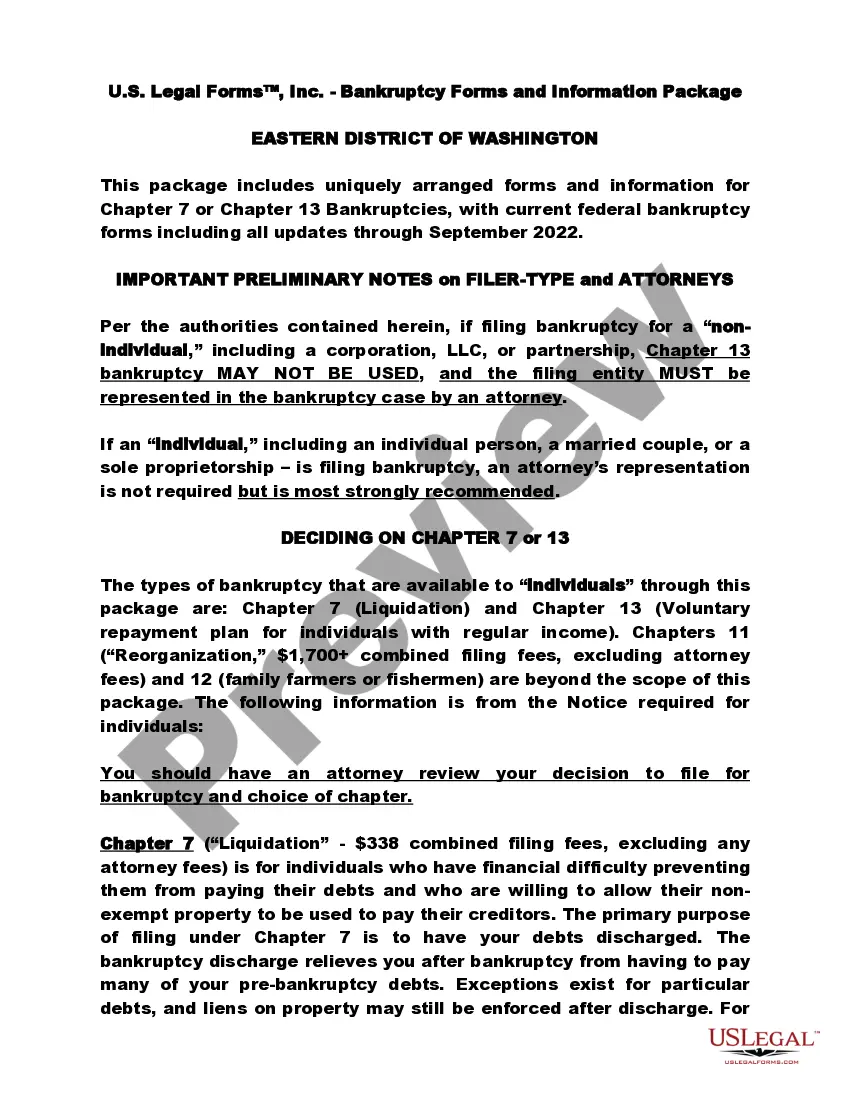

Uniquely packaged forms and information for Chapter 7 or 13 bankruptcies, including detailed instructions and other resources. Click and view the Free Preview for the latest revision dates and a complete overview of contents.

Washington Western District Bankruptcy Guide and Forms Package for Chapters 7 or 13

Instant download

Description

Free preview

How to fill out Washington Western District Bankruptcy Guide And Forms Package For Chapters 7 Or 13?

Out of the multitude of services that provide legal templates, US Legal Forms provides the most user-friendly experience and customer journey when previewing templates before purchasing them. Its extensive library of 85,000 templates is grouped by state and use for efficiency. All of the forms available on the service have been drafted to meet individual state requirements by certified lawyers.

If you have a US Legal Forms subscription, just log in, look for the form, click Download and access your Form name in the My Forms; the My Forms tab keeps all of your saved forms.

Follow the tips listed below to obtain the document:

- Once you discover a Form name, make certain it’s the one for the state you need it to file in.

- Preview the form and read the document description just before downloading the template.

- Search for a new sample via the Search field in case the one you have already found isn’t appropriate.

- Click Buy Now and choose a subscription plan.

- Create your own account.

- Pay using a credit card or PayPal and download the document.

Once you have downloaded your Form name, you are able to edit it, fill it out and sign it with an online editor that you pick. Any form you add to your My Forms tab might be reused many times, or for as long as it remains the most up-to-date version in your state. Our service offers quick and simple access to templates that fit both legal professionals as well as their clients.

Form popularity

FAQ

In many cases, Chapter 7 bankruptcy is a better fit than Chapter 13 bankruptcy. For instance, Chapter 7 is quicker, many filers can keep all or most of their property, and filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

The cost for filing a Chapter 7 bankruptcy is $306. This fee may not be waived but you may be able to pay it in installments. The fee of $281 for a Chapter 13 bankruptcy cannot be waived.

A Chapter 13 bankruptcy involves repaying some or all of your debt over a three- to- five-year period, while a Chapter 7 bankruptcy involves wiping out most of your debts without paying them back.In that way, a Chapter 13 may be better for your credit than a Chapter 7.

Chapter 13 Is Likely to Worsen Your Finances When your Chapter 13 case is dismissed, you are often in a far worse financial position. That's because the interest on your unpaid debts has continued to mount as you've struggled to make payments. And once you're out of bankruptcy protection, you have more debt than ever.

Chapter 11 bankruptcy works well for businesses and individuals whose debt exceeds the Chapter 13 bankruptcy limits. In most cases, Chapter 13 is the better choice for qualifying individuals and sole proprietors.

Key Takeaways. Chapter 7 bankruptcy doesn't require a repayment plan but does require you to liquidate or sell nonexempt assets to pay back creditors.Chapter 13 bankruptcy eliminates qualified debt through a repayment plan over a three- or five-year period.

However, if your first bankruptcy case was dismissed, including a voluntary dismissal, you can generally file again for either Chapter 7 or Chapter 13 at any time.Similarly, the automatic stay is limited to 30 days if a debtor files for Chapter 7 bankruptcy within one year of a previous case being dismissed.

How soon can you file for Chapter 13 after Chapter 7 bankruptcy? In order to get debts discharged through Chapter 13, you must wait four years after filing a Chapter 7 bankruptcy.

A Chapter 7 bankruptcy will generally discharge your unsecured debts, such as credit card debt, medical bills and unsecured personal loans. The court will discharge these debts at the end of the process, generally about four to six months after you start.