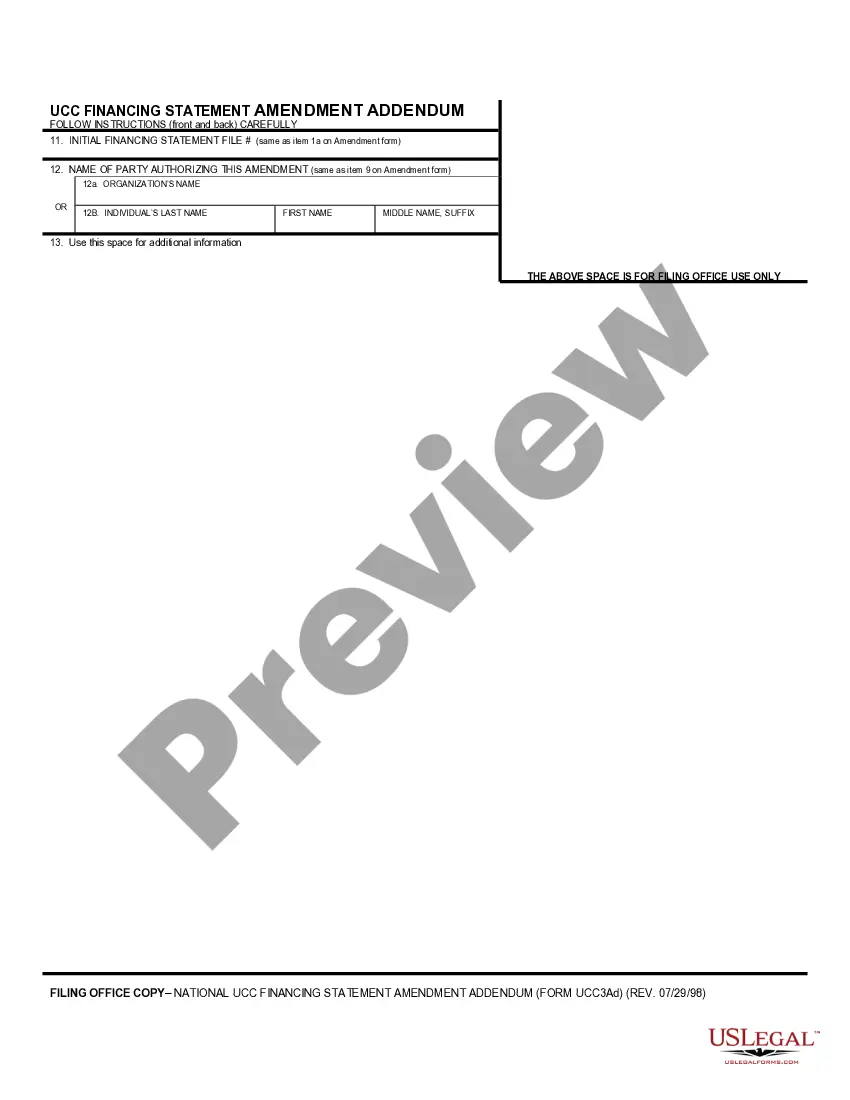

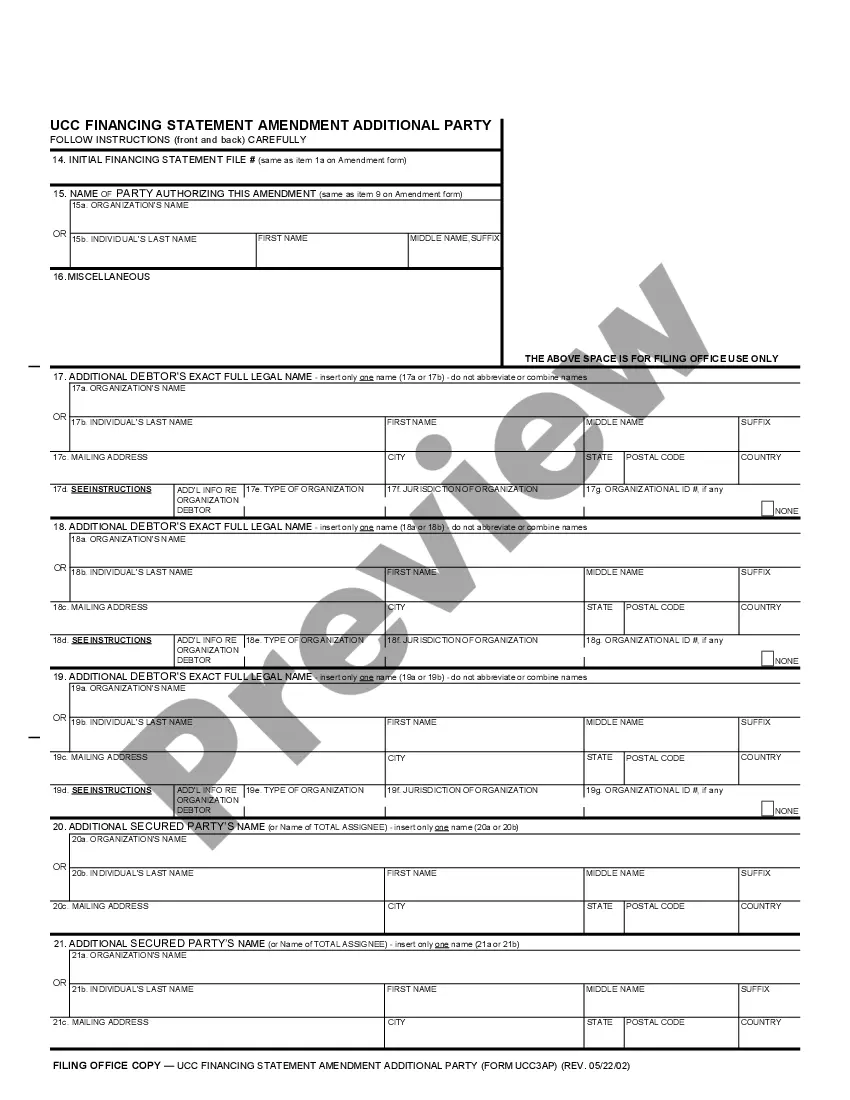

UCC3 - Financing Statement Amendment - Vermont - For use after July 1, 2001. This amendment is to be filed in the real estate records. This Financing Statement complies with all applicable state statutes.

Vermont UCC3 Financing Statement Amendment

Category:

State:

Vermont

Control #:

VT-UCC3

Format:

Word;

PDF;

Rich Text

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Vermont UCC3 Financing Statement Amendment?

Looking for a Vermont UCC3 Financing Statement Amendment on the internet might be stressful. All too often, you see papers that you just believe are alright to use, but discover afterwards they’re not. US Legal Forms offers more than 85,000 state-specific legal and tax documents drafted by professional attorneys in accordance with state requirements. Get any form you’re looking for within a few minutes, hassle free.

If you already have the US Legal Forms subscription, just log in and download the sample. It will instantly be included to the My Forms section. If you do not have an account, you must sign-up and select a subscription plan first.

Follow the step-by-step recommendations below to download Vermont UCC3 Financing Statement Amendment from the website:

- Read the form description and press Preview (if available) to verify whether the form suits your expectations or not.

- In case the form is not what you need, get others using the Search field or the provided recommendations.

- If it is right, click on Buy Now.

- Choose a subscription plan and create an account.

- Pay with a bank card or PayPal and download the document in a preferable format.

- Right after getting it, you may fill it out, sign and print it.

Get access to 85,000 legal templates from our US Legal Forms catalogue. Besides professionally drafted templates, customers can also be supported with step-by-step instructions regarding how to get, download, and fill out templates.

Form popularity

FAQ

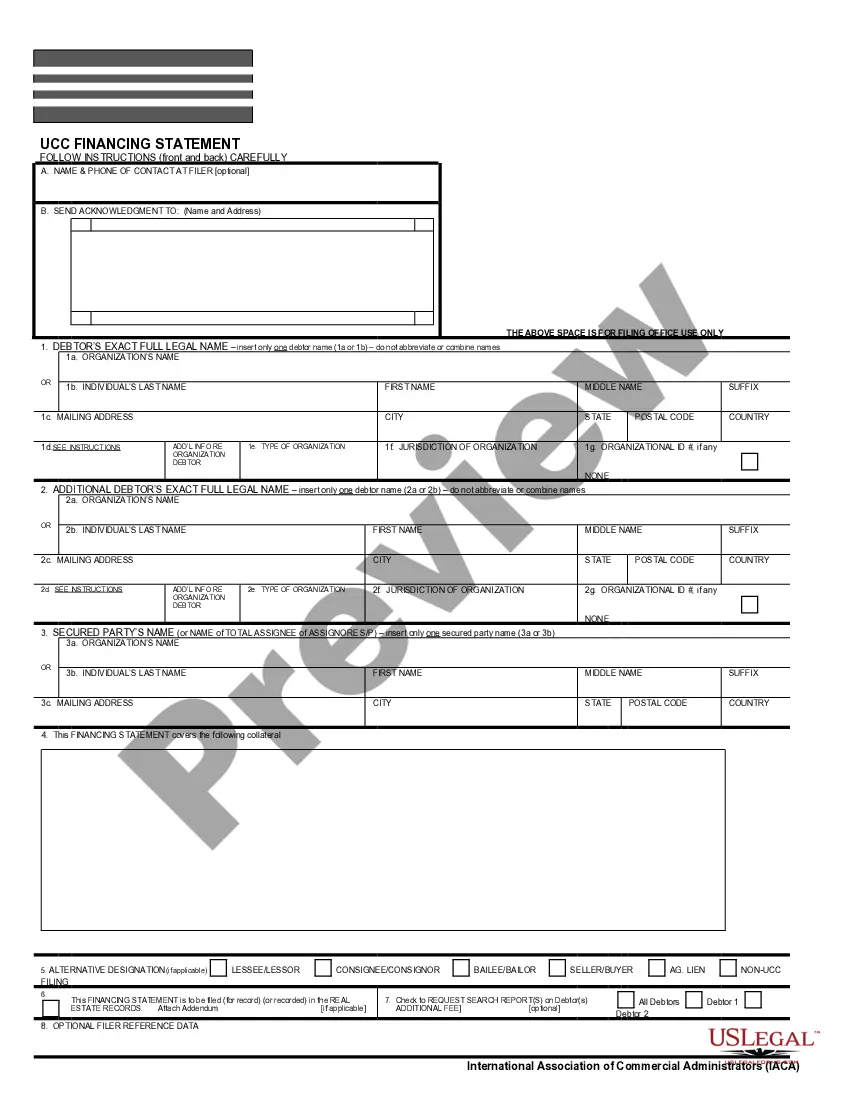

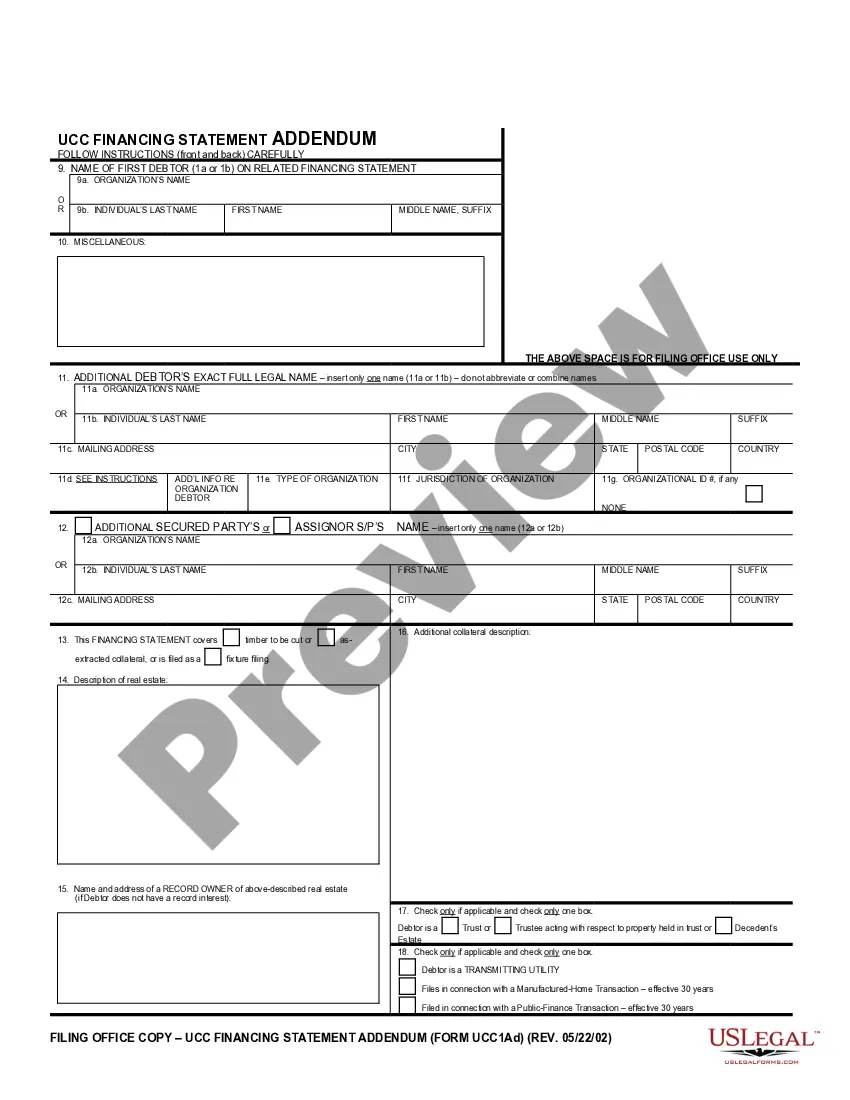

Also known as a UCC-3, and, depending on the context, a UCC-3 financing statement amendment, a UCC-3 termination statement, and a UCC-3 continuation statement. Under the Uniform Commercial Code, a UCC-3 is used to continue, assign, terminate, or amend an existing UCC-1 financing statement (UCC-1).

When the debtor has satisfied all amounts owed to the lender, a UCC-3 termination statement (now called a UCC termination statement) is routinely filed to terminate the security interest perfected by the UCC-1 financing statement.

A UCC1 financing statement is effective for a period of five years. A record that is not continued before its lapse date will cease to be effective, costing the secured party their perfected status and perhaps their priority position to collect. Once a financing statement has lapsed, it cannot be revived.

Why file a UCC-3 form? The UCC-3 is the Swiss-Army-Knife of forms. Unlike a UCC 1, a UCC 3 can be used for multiple purposes. The actions one can take are Amendment, Assignment, Continuation, and Termination.

To continue the effectiveness of a UCC-1 financing statement beyond its initial 5-year effective period, a secured party must file a Continuation. A Continuation extends the life of the financing statement for an additional five years.Each Continuation must identify, by its file number, the UCC-1 to which it relates.

Rules vary by State around releasing a UCC lien after a borrower satisfied the debt. Primarily there are two main ways to remove them. One way is by having the lender file a UCC-3 Financing Statement Amendment. Another way to remove a UCC filing is by swearing an oath of full payment at the secretary of state office.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.

After receiving your request, the lender has 20 days to terminate the UCC filing.

The UCC-1 Financing Statement is filed to protect a lender's or creditor's security interest by giving public notice that there is a right to take possession of and sell certain assets for repayment of a specific debt with a certain debtor.