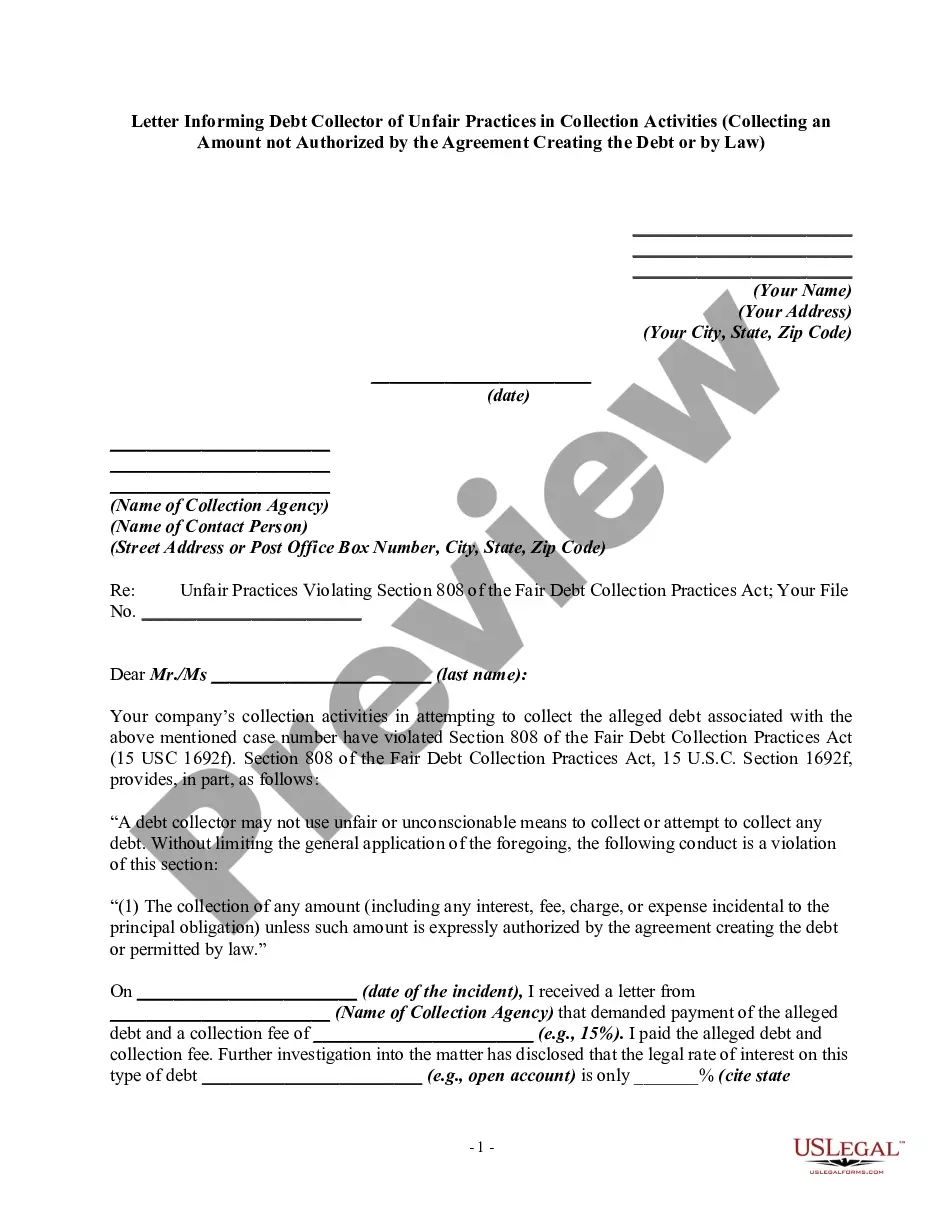

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Vermont Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

You might dedicate time online trying to discover the legal document template that meets the state and federal requirements you need.

US Legal Forms offers thousands of legal forms which can be reviewed by experts.

You can actually download or print the Vermont Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law from my service.

If available, utilize the Preview button to view the document template as well.

- If you possess a US Legal Forms account, you may Log In and click the Download button.

- After that, you may complete, modify, print, or sign the Vermont Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law.

- Every legal document template you obtain is your permanent property.

- To get another copy of any purchased form, go to the My documents tab and click the relevant button.

- If you are visiting the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for your chosen region/city.

- Check the form outline to make sure you have selected the right form.

Form popularity

FAQ

The document must include the credit limit, the interest rate and details of how and when a debtor is to discharge his payment obligations. A failure to produce such a document is still capable of rendering the agreement irredeemably unenforceable.

Does debt go away after 7 years? In the UK, for most people, unsecured debts go away after a period of 6 years from the point when they started or 6 years from the point when they last made a payment to, or had contact with, their creditor. This period can be 12 years for some mortgage debts.

You are not obliged let a debt collector into your home and they don't have the right to take goods away. It's very important to understand that a debt collector is not the same as an enforcement agent or bailiff. Debt collectors have no special legal powers.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts.

Debt collectors have no special legal powers. You may feel under pressure to pay more than you can afford, but don't feel threatened. Find out more about the difference between debt collectors and bailiffs. Debt collectors may work for your creditor, or they may work for a separate debt collection agency.

If a creditor waits too long to take court action, the debt will become 'unenforceable' or statute barred. This means the debt still exists but the law (statute) can be used to prevent (bar) the creditor from getting a court judgment or order to recover it.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Repeated calls. Threats of violence. Publishing information about you. Abusive or obscene language.

A credit agreement is a legally-binding contract documenting the terms of a loan agreement; it is made between a person or party borrowing money and a lender. The credit agreement outlines all of the terms associated with the loan. Credits agreements are created for both retail and institutional loans.