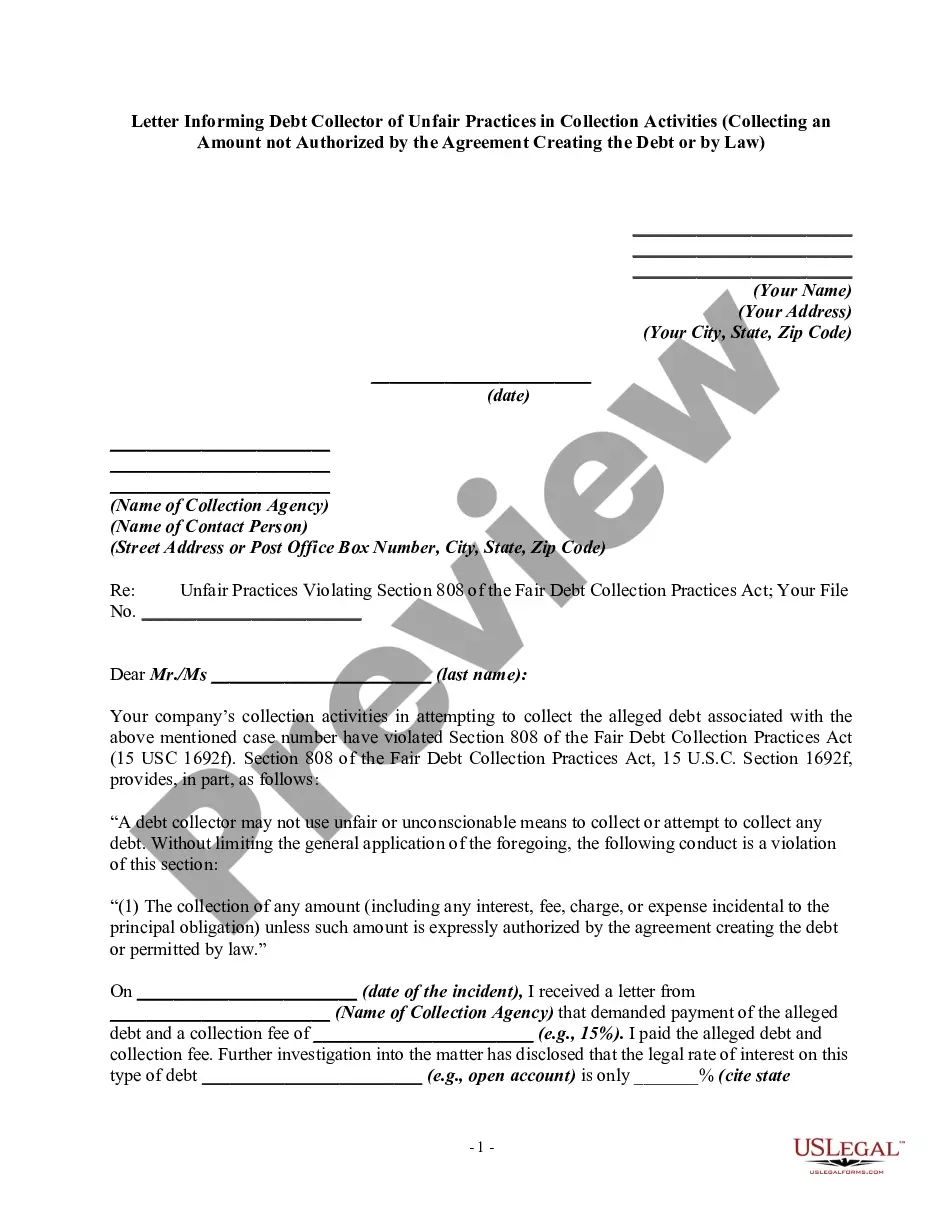

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Virgin Islands Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

Are you currently in a location where you require documents for occasional business or personal purposes nearly every working day.

There are numerous legal document templates available online, but locating those you can trust is not simple.

US Legal Forms offers thousands of form templates, such as the Virgin Islands Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law, which are designed to comply with state and federal regulations.

You can obtain another copy of the Virgin Islands Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law at any time if needed. Simply click on the relevant form to download or print the document template.

Use US Legal Forms, the most comprehensive collection of legal forms, to save time and avoid mistakes. The service provides professionally crafted legal document templates that you can utilize for various purposes. Create an account on US Legal Forms and start simplifying your life.

- If you are already aware of the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Virgin Islands Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law template.

- If you do not possess an account and wish to start utilizing US Legal Forms, follow these instructions.

- Obtain the form you require and confirm it is for the correct state/region.

- Use the Preview button to inspect the form.

- Review the description to ensure you have selected the right template.

- If the form is not what you're searching for, utilize the Lookup field to find the form that satisfies your needs and specifications.

- When you locate the proper form, click Get now.

- Select the payment plan you prefer, enter the necessary details to set up your account, and complete the purchase using your PayPal or credit card.

- Choose a suitable document format and download your copy.

- Access all the document templates you have purchased in the My documents section.

Form popularity

FAQ

A debt validation letter is what a debt collector sends you to prove that you owe them money. This letter shows you the details of a specific debt, outlines what you owe, who you owe it to, and when they need you to pay. Get help with your money questions.

Remember, debts that cannot be enforced are only protected from court action; the bad debt is still going on your credit report. If you want to settle the debt, you have to negotiate. If the collector cannot produce the agreement, you don't have to pay your dues.

If you don't pay a collection agency, the agency will send the matter back to the original creditor unless the collection agency owns the debt. If the collection agency owns the debt, they may send the matter to another collection agency. Often, the collection agency or the original creditor will sue you.

If a debt collector fails to validate the debt in question and continues trying to collect, you have a right under the FDCPA to countersue for up to $1,000 for each violation, plus attorney fees and court costs, as mentioned previously.

§ 1006.34 Notice for validation of debts.Deceased consumers.Bankruptcy proofs of claim.In general.Subsequent debt collectors.Last statement date.Last payment date.Transaction date.Assumed receipt of validation information.More items...

As per the Limitation Act 1980, a creditor can chase a debt for a period of six years if the debt is unsecured. If the debt is a mortgage debt, then the period is twelve years in most cases.

The validation notice is meant to help you recognize whether the debt is yours and dispute the debt if it is not yours. The notice generally must include: A statement that the communication is from a debt collector. The name and mailing information of the debt collector and the consumer.

Not being able to meet payment obligations can make anyone feel anxious and worried, but in most cases, you won't have to worry about serving jail time if you are unable to pay off your debts. You cannot be arrested or go to jail simply for being past-due on credit card debt or student loan debt, for instance.

If a creditor waits too long to take court action, the debt will become 'unenforceable' or statute barred. This means the debt still exists but the law (statute) can be used to prevent (bar) the creditor from getting a court judgment or order to recover it.

Under the Fair Debt Collection Practices Act (FDCPA), a debt collector must respond to a request for a debt validation letter. If they don't, they're in violation of the act. You can report them to your state's attorney general, the FTC or the Consumer Financial Protection Bureau (CFPB).