Utah Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Balloon Secured Note Addendum And Rider To Mortgage, Deed Of Trust Or Security Agreement?

Are you in a situation where you require documents for both organizational or personal reasons almost all the time.

There are numerous legal form templates accessible online, but finding ones you can rely on is not easy.

US Legal Forms provides thousands of document templates, such as the Utah Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement, which can be tailored to meet state and federal regulations.

Once you find the correct form, click Buy now.

Choose the pricing plan you want, provide the necessary information to create your account, and pay for the order using your PayPal or credit card.

- If you are already familiar with the US Legal Forms website and have your account, simply Log In.

- After that, you can download the Utah Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is for the correct city/state.

- Use the Preview option to review the form.

- Check the details to confirm you have selected the correct document.

- If the form isn’t what you are looking for, use the Search field to find the form that meets your requirements.

Form popularity

FAQ

Benefits of a balloon payment For example, if you buy a car for R400,000 with a balloon payment of 20%, your monthly instalments will be paying off a capital balance of R320,000. The remaining R80,000 (the balloon payment) will be due at the end of your loan term ? usually 72 months.

Example of a Balloon Loan Let's say a person takes out a $200,000 mortgage with a seven-year term and a 4.5% interest rate. Their monthly payment for seven years is $1,013. At the end of the seven-year term, they owe a $175,066 balloon payment.

When the loan is interest-only, you only pay interest throughout the life of the loan. The final payment on the loan is called a balloon payment and equals the entire principal. This amount is due at the end of the loan period.

There are also some risks associated with balloon mortgages, including defaulting on the loan if you're unable to make the balloon payment at the end of the loan term. In such cases, your lender will likely take steps to foreclose on your home.

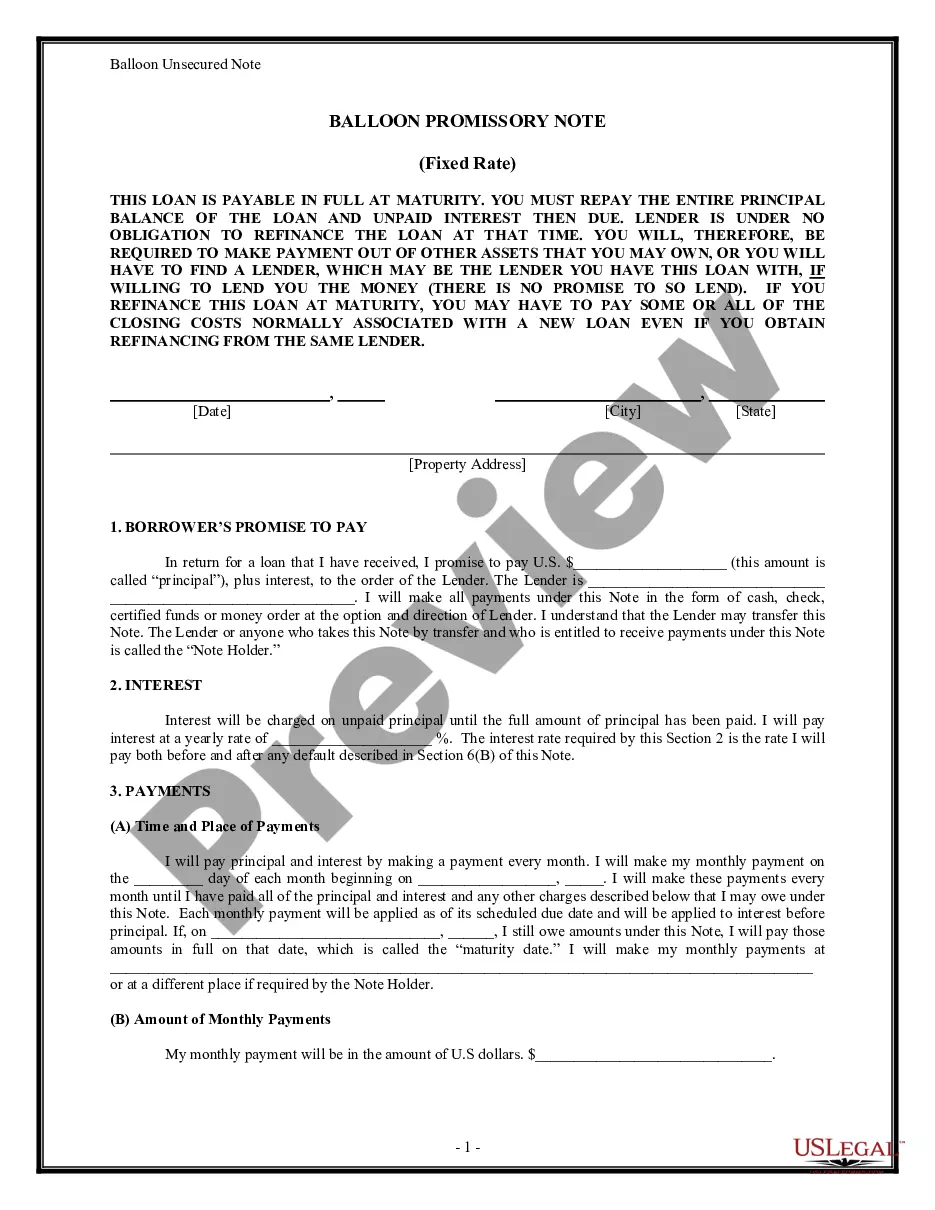

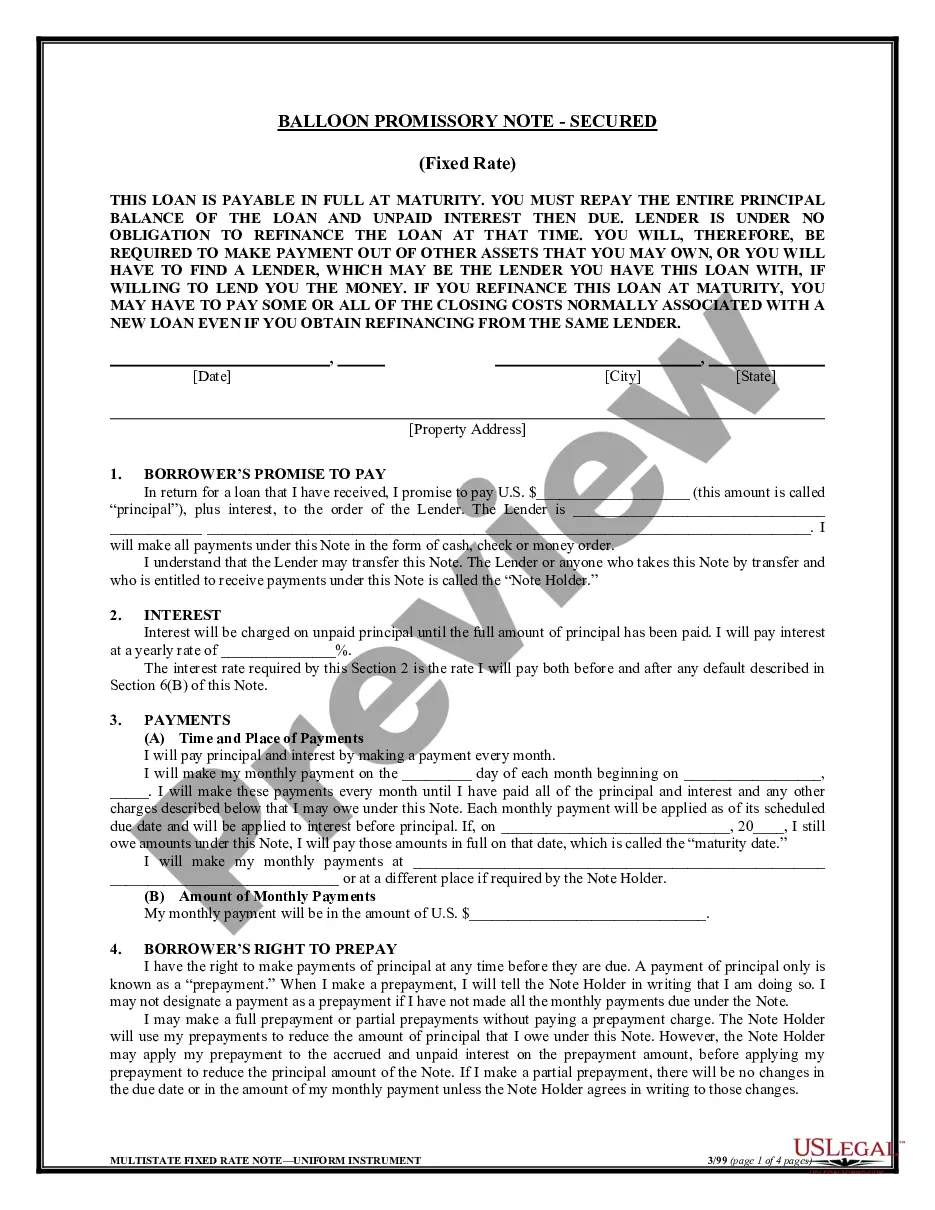

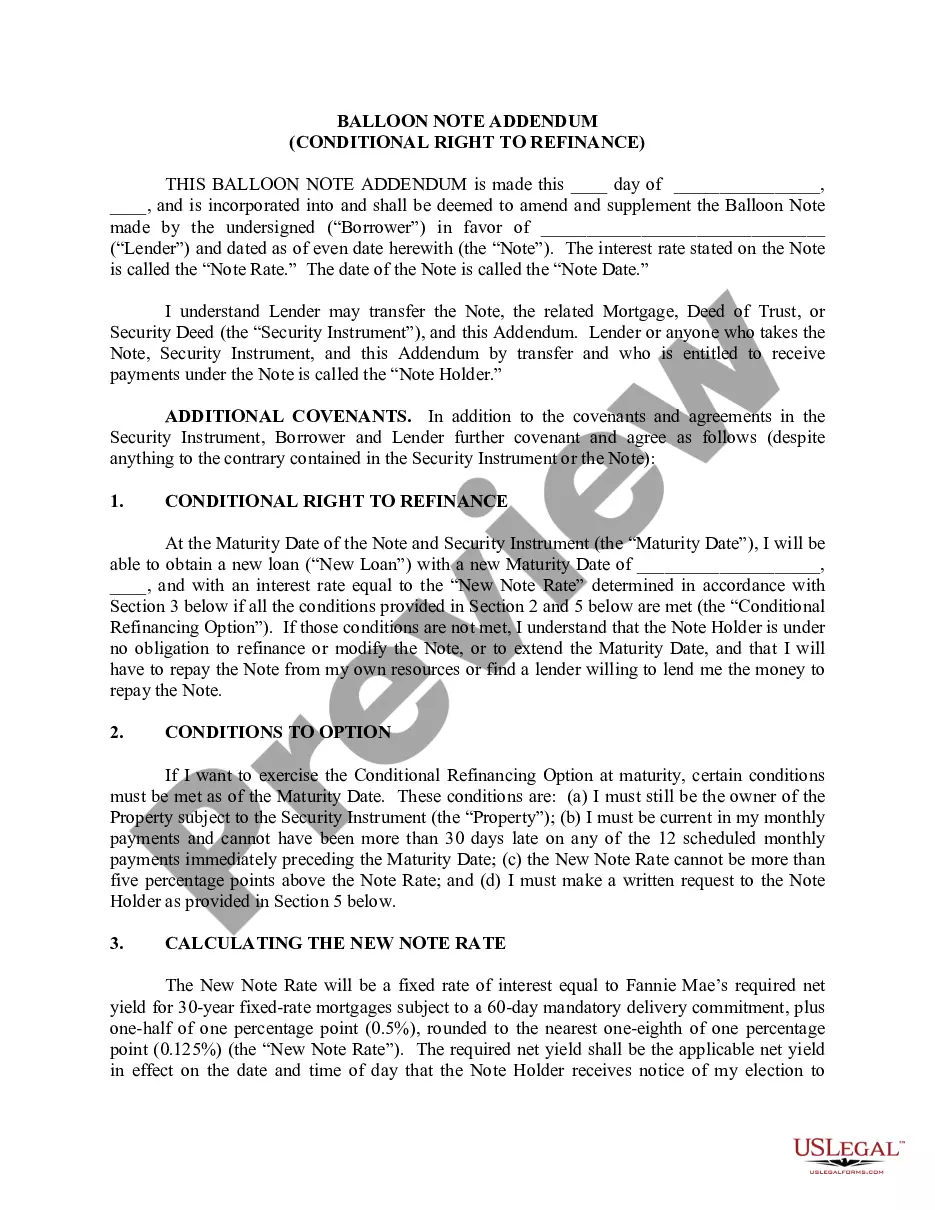

A balloon mortgage is a type of home loan in which you make low or no monthly payments for a short term, usually five or seven years. After this low- or no-payment period ends, you pay a lump sum, which settles the remaining balance in full.

Examples of a Balloon Payment Schedule A homebuyer may take a seven-year balloon mortgage of $150,000, paying $531.25 in interest-only payments each month. Throughout the life of the loan, those payments wouldn't change, but neither does the balance due on the mortgage. At the end of the term, the buyer owes $150,000.

A Promissory Note with Balloon Payments is a loan contract that enables a lender set loan terms with one or more larger payments at the end. This lending document helps you to clarify the terms of a loan, define the payment schedule, and provide an amortization table, if the loan includes interest.

A balloon payment is the final amount due on a loan that is structured as a series of small monthly payments followed by a single much larger sum at the end of the loan period. The early payments may be all or almost all payments of interest owed on the loan, with the balloon payment being the principal of the loan.