Utah Assignment to Living Trust

Understanding this form

The Assignment to Living Trust form is a legal document used to transfer ownership of specific property to a Living Trust. This type of trust is created during an individual's lifetime, allowing them to manage their assets effectively for estate planning purposes. Unlike a will, which takes effect after death, a living trust provides more immediate benefits, such as avoiding probate and simplifying asset management.

Main sections of this form

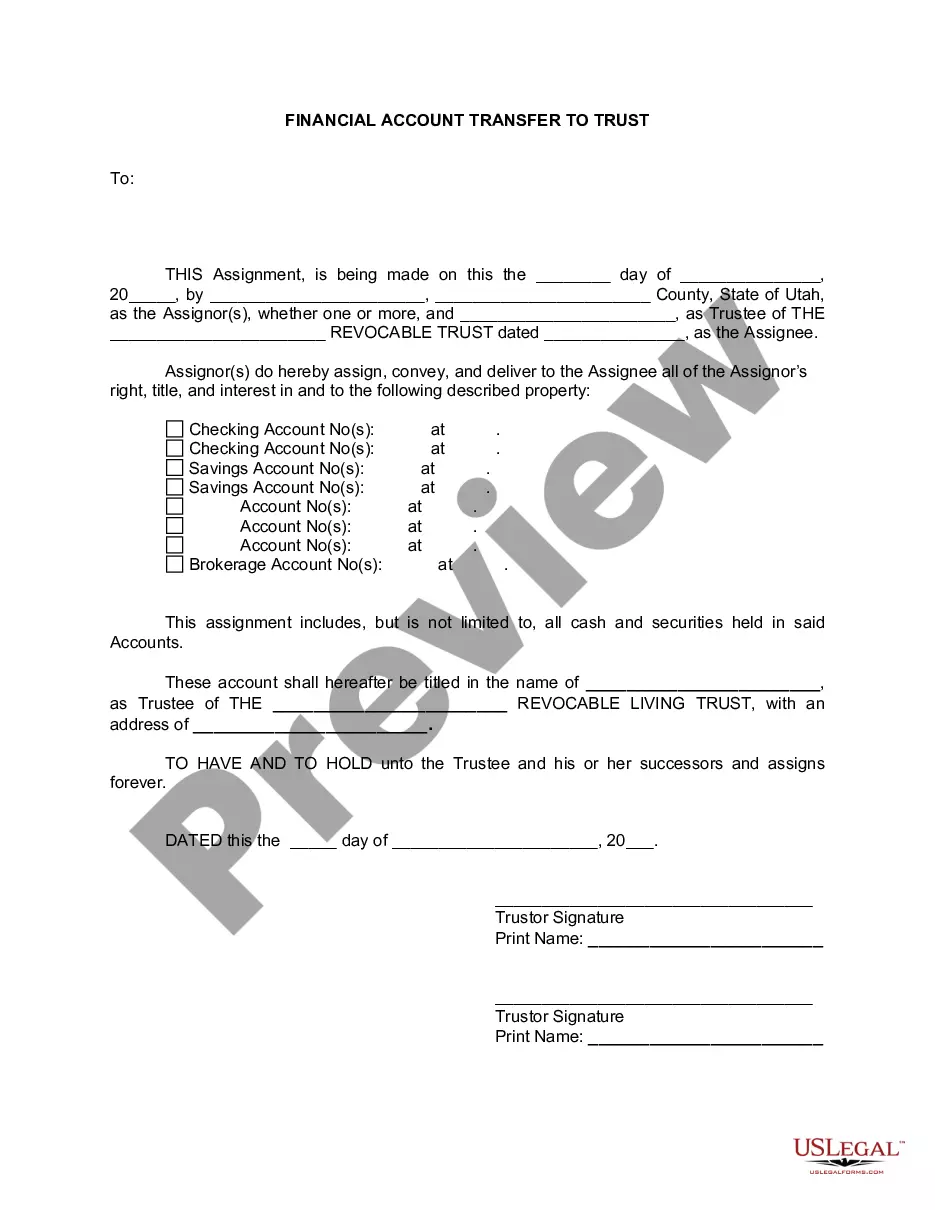

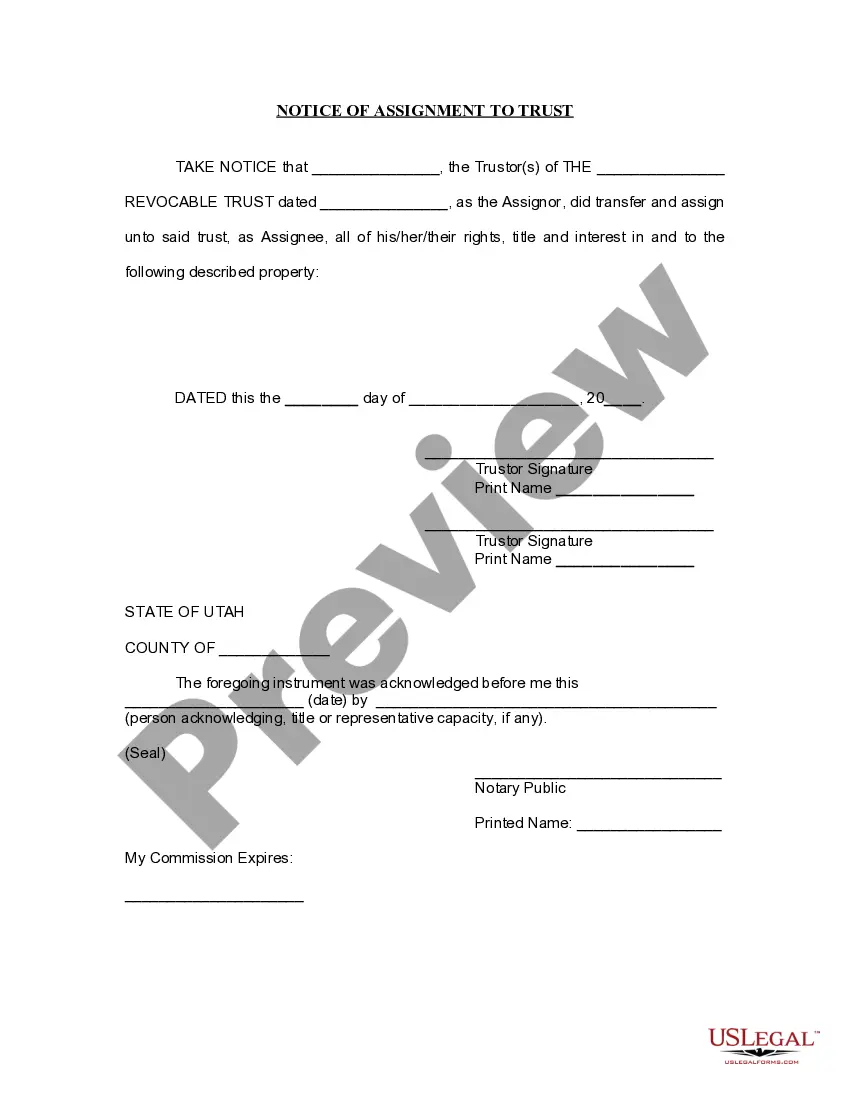

- Parties involved: Assignor(s) and Trustee information.

- Assignment details: Description of the property being assigned.

- Date of execution: The date when the document is completed.

- Notary acknowledgment section: Verification by a notary public.

Common use cases

This form is essential when you wish to transfer property to a Living Trust. You might need it when setting up the trust to ensure that your assets are included, or if you want to modify the assets held by your existing trust. Situations that may prompt using this form include the purchase of new property or changing your trust's structure during your lifetime.

Who should use this form

This form is suitable for:

- Individuals creating a Living Trust to manage their estate.

- Property owners looking to transfer assets into a trust.

- Trustees responsible for managing trust property.

How to prepare this document

- Identify the Assignor(s): Provide the names and addresses of the person or people transferring the property.

- Specify the property: Clearly describe the asset being transferred to the Living Trust.

- Enter the date: Fill in the date on which the transfer is being executed.

- Obtain signatures: The Assignor(s) must sign the form in front of a notary public.

- Complete notarization: Ensure the notary public acknowledges the document with their signature and seal.

Notarization requirements for this form

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to accurately describe the property being transferred.

- Not signing the document in the presence of a notary.

- Leaving out key identifying information about the Assignor(s) or Trustee.

Benefits of completing this form online

- Convenience: Download and complete the form at your own pace.

- Editability: Easily modify the document to suit your specific needs.

- Reliable templates: Forms drafted by licensed attorneys ensure legal compliance.

Main things to remember

- The Assignment to Living Trust form facilitates the transfer of assets to a trust during a person's lifetime.

- Accurate completion and notarization are essential for legal validity.

- This form aids in effective estate planning by managing assets and avoiding probate.

Looking for another form?

Form popularity

FAQ

Qualified retirement accounts 401ks, IRAs, 403(b)s, qualified annuities. Health saving accounts (HSAs) Medical saving accounts (MSAs) Uniform Transfers to Minors (UTMAs) Uniform Gifts to Minors (UGMAs) Life insurance. Motor vehicles.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

You should still have a durable power of attorney for finances.You may even want to empower your attorney-in-fact to transfer into your living trust any property that becomes yours after you become incapacitated. Only a durable power of attorney for finances can grant that authority.

Pick a type of living trust. If you're married, you'll first need to decide whether you want a single or joint trust. Take stock of your property. Choose a trustee. Draw up the trust document. Sign the trust. Transfer your property to the trust.

Sure you can write your own revocable living trust.The discussion of your need for a revocable living trust is in another of my articles, but it is safe to say that if you own real property and have a significant estate (over about $50,000), then you could use a trust and it would help your loved ones.

This should include the titles and deeds to real property, bank account information, investment accounts, stock certificates, life insurance policies, and other assets you will be using to fund the trust. Having this information available will make it easier to prepare your trust distribution provisions.

Pick a single or joint trust. If you're married, a joint trust lets you to split your property between what's individually and jointed owned. Review and inventory your property. Decide on a trustee. Write out your trust documents. Sign your living trust in front of a notary public. Fund your trust.

When you create a DIY living trust, there are no attorneys involved in the process. You will need to choose a trustee who will be in charge of managing the trust assets and distributing them.You'll also need to choose your beneficiary or beneficiaries, the person or people who will receive the assets in your trust.

A living trust is an important part of your estate plan. Most people can create a living trust without an attorney using software or an online service.