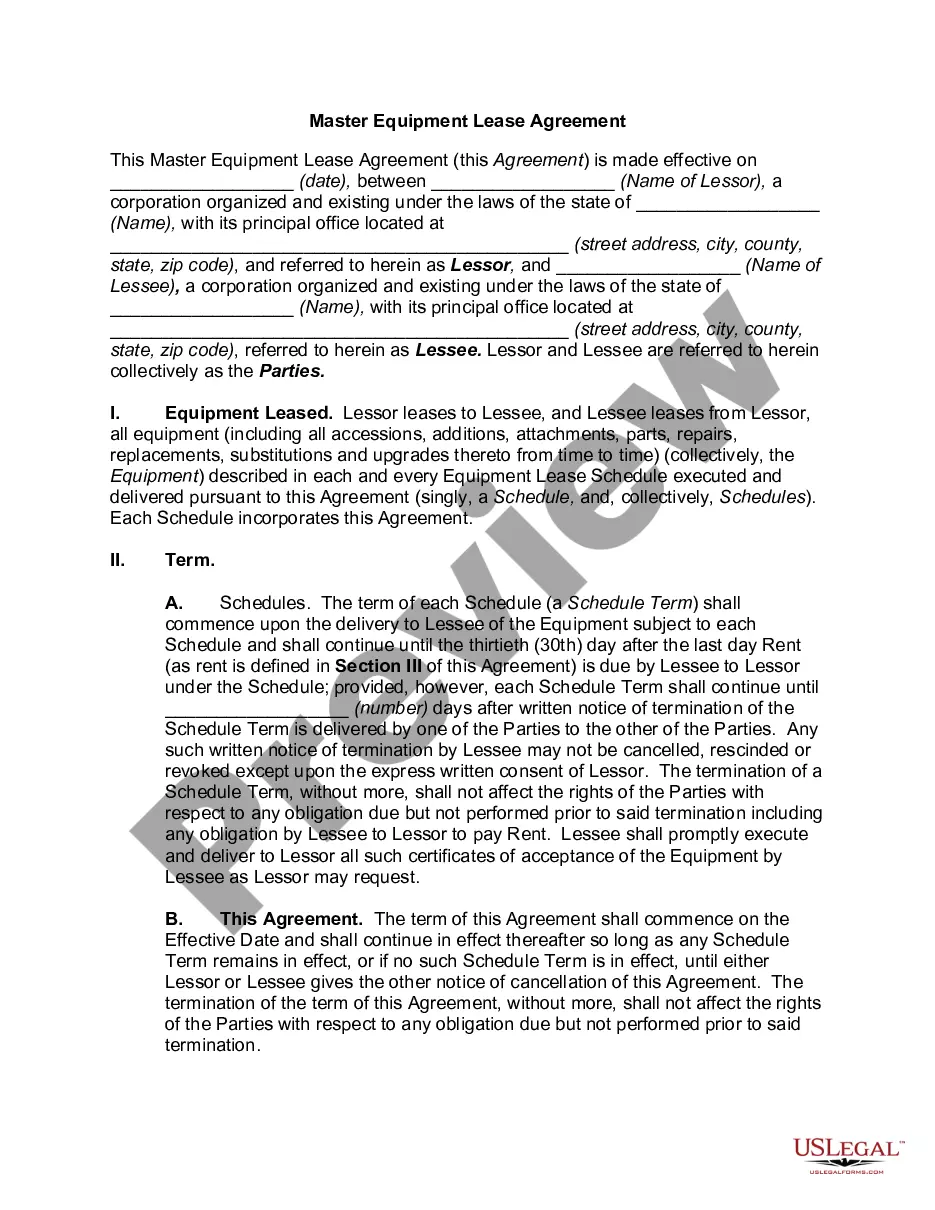

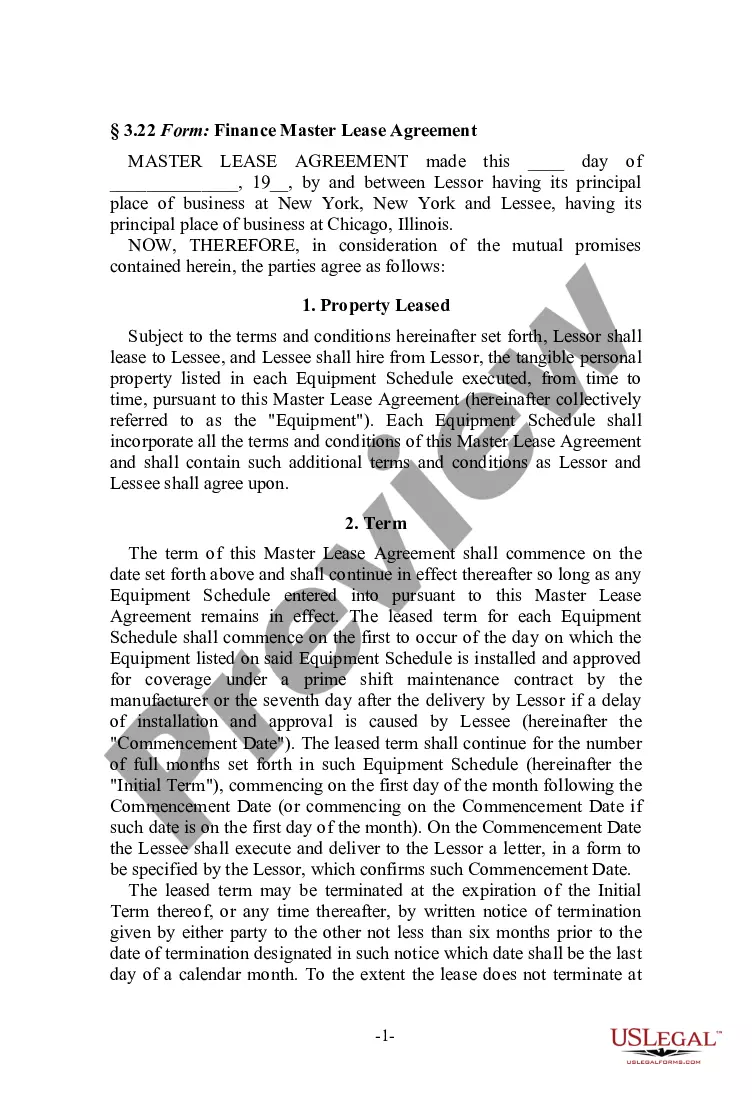

Equipment Technology Lease

What is this form?

The Equipment Technology Lease is a legal document that establishes an agreement between a vendor and a lessee for leasing equipment or technology. This form outlines the responsibilities of both parties, including delivery, rental payments, lease terms, and options for purchase or substitution of the equipment. It serves as a critical tool for businesses looking to use specialized equipment without the upfront costs of purchasing it outright.

Form components explained

- Lease Rental Deposit: Terms regarding deposit and initial payment due on the effective date.

- Rent: Details on monthly rent, including late fees for non-return of equipment.

- Term: Specifies the duration of the lease and conditions for termination.

- Purchase Option: Describes options for the lessee to purchase the equipment at the end of the lease.

- Substitution of Equipment: Terms for replacing outdated equipment with newer technology.

- Indemnification: Responsibilities regarding liability for injuries or damages related to the use of the equipment.

When to use this document

This form is ideal for businesses that need to lease technology or equipment for a specific period but do not wish to commit to purchasing it. Use this form when you want to outline the renting terms clearly, if you plan to use the equipment for a defined project, or if you need the option to eventually buy the equipment after the lease term ends.

Intended users of this form

- Businesses looking to lease equipment or technology without buying it outright.

- Corporations needing temporary use of specialized machinery for projects.

- Startups that require equipment with limited financial resources.

- Organizations assessing equipment before deciding to purchase.

How to complete this form

- Identify the parties involved: Fill in the lessee's name and address, and vendor details.

- Specify the lease term: Enter the start and end date for the lease.

- Detail the financial terms: Include the deposit, rent amount, and purchase option price in Exhibit A.

- Outline equipment details: Describe the equipment being leased along with its condition and any necessary specifications.

- Review and sign: Ensure both parties sign the agreement to make it legally binding.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to specify all equipment details, leading to disputes.

- Not including the specific lease term, which can create confusion about duration.

- Overlooking the need for initial payments or deposits as specified.

- Not reviewing the indemnification clause, which can affect liability.

Benefits of completing this form online

- Accessibility: Easily download and fill out the form at your convenience.

- Editability: Modify the template as needed to fit your specific lease situation.

- Cost-effective: Avoid legal fees by using a trusted template created by licensed attorneys.

- Time-saving: Quickly generate a legal document without extensive legal knowledge.

Legal use & context

- This lease agreement is legally binding once signed, outlining the obligations of both parties.

- Enforceability is governed by the laws of the relevant jurisdiction, typically aligning with commercial lease regulations.

- It may include limitations related to the technology or equipment that could impact liability or repairs during the term.

Looking for another form?

Form popularity

FAQ

Leasing companies can make money when a lessee requests for an upgrade to the equipment they currently have or request for the lease contract to be modified. If the upgrade does not have a stand-alone value or is not readily removable, the leasing company will pay for the upgrade.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

A lessee must capitalize a leased asset if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An asset should be capitalized if:The lease runs for 75% or more of the asset's useful life.

An equipment lease agreement is a contractual agreement where the lessor, who is the owner of the equipment, allows the lessee to use the equipment for a specified period in exchange for periodic payments. The subject of the lease may be vehicles, factory machines, or any other equipment.

Unlike an outright purchase or equipment secured through a standard loan, equipment under an operating lease cannot be listed as capital. It's accounted for as a rental expense. This provides two specific financial advantages: Equipment is not recorded as an asset or liability.

Assets being leased are not recorded on the company's balance sheet; they are expensed on the income statement. So, they affect both operating and net income.