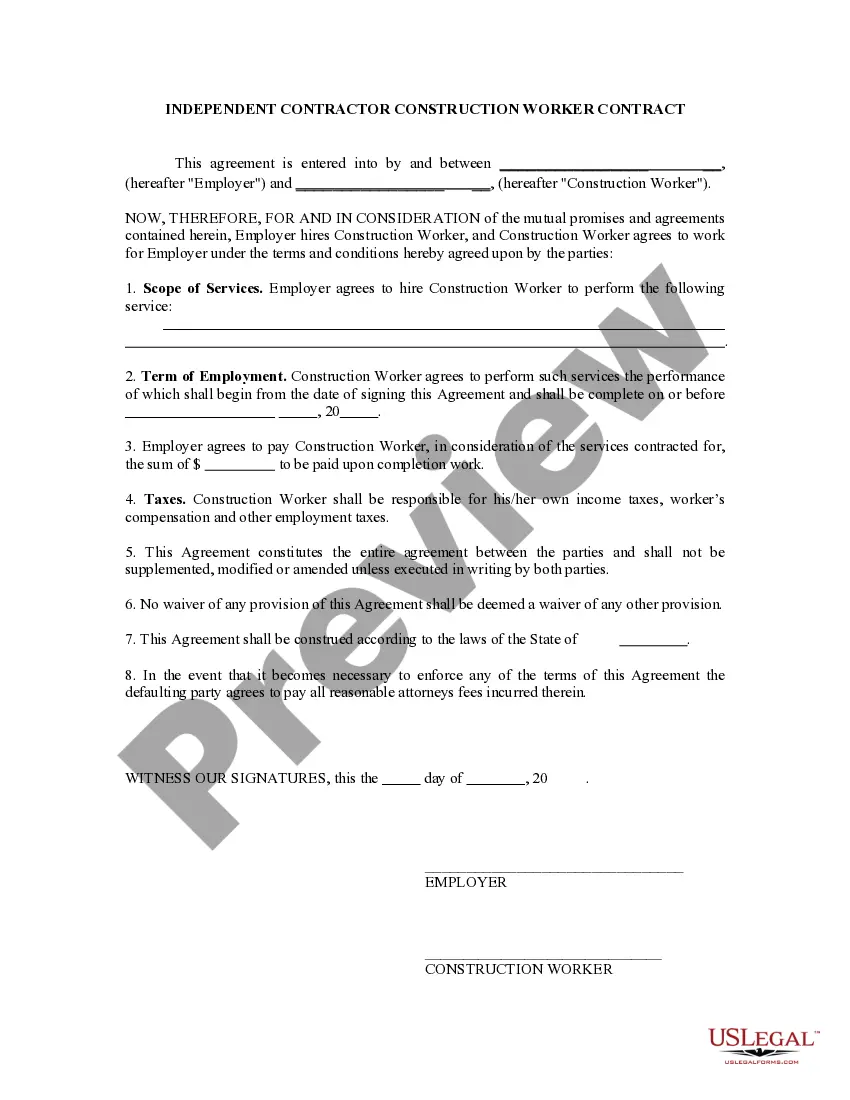

Determining Self-Employed Contractor Status

Overview of this form

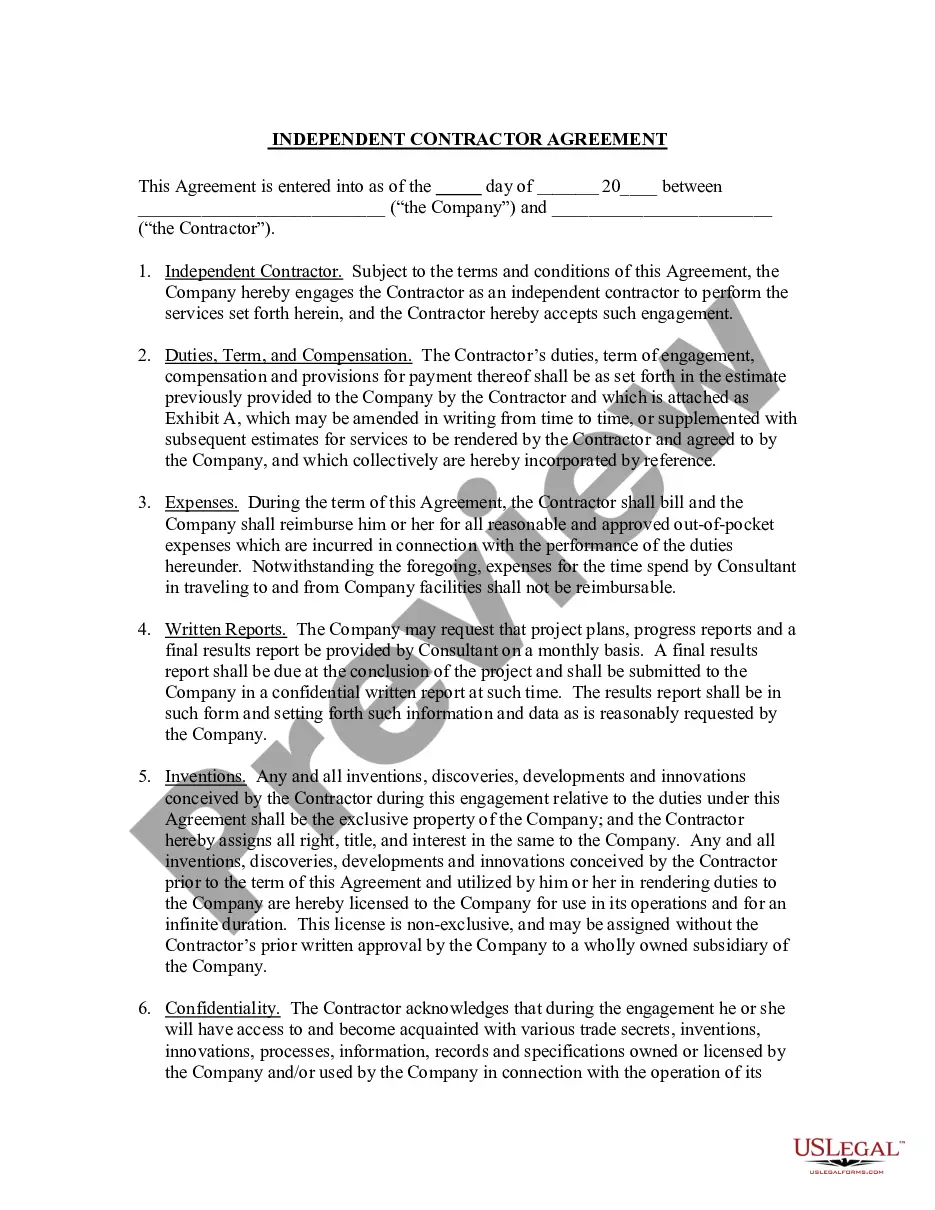

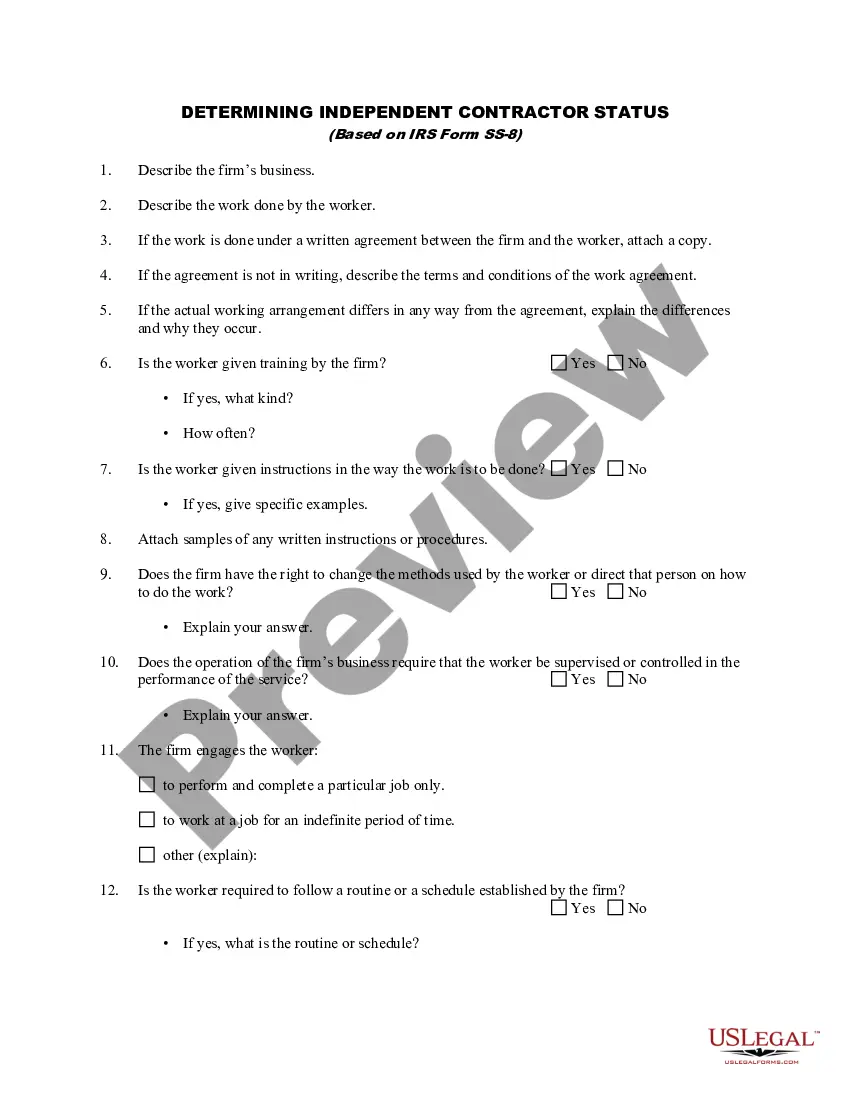

The Determining Self-Employed Contractor Status form is designed to help assess whether a contractor is classified as an independent contractor or an employee. This differentiation is crucial as it impacts tax responsibilities, legal rights, and insurance obligations. Unlike other employment forms, this document specifically focuses on evaluating the degree of control exerted by one party over the other, which is a key factor in determining employment status.

What’s included in this form

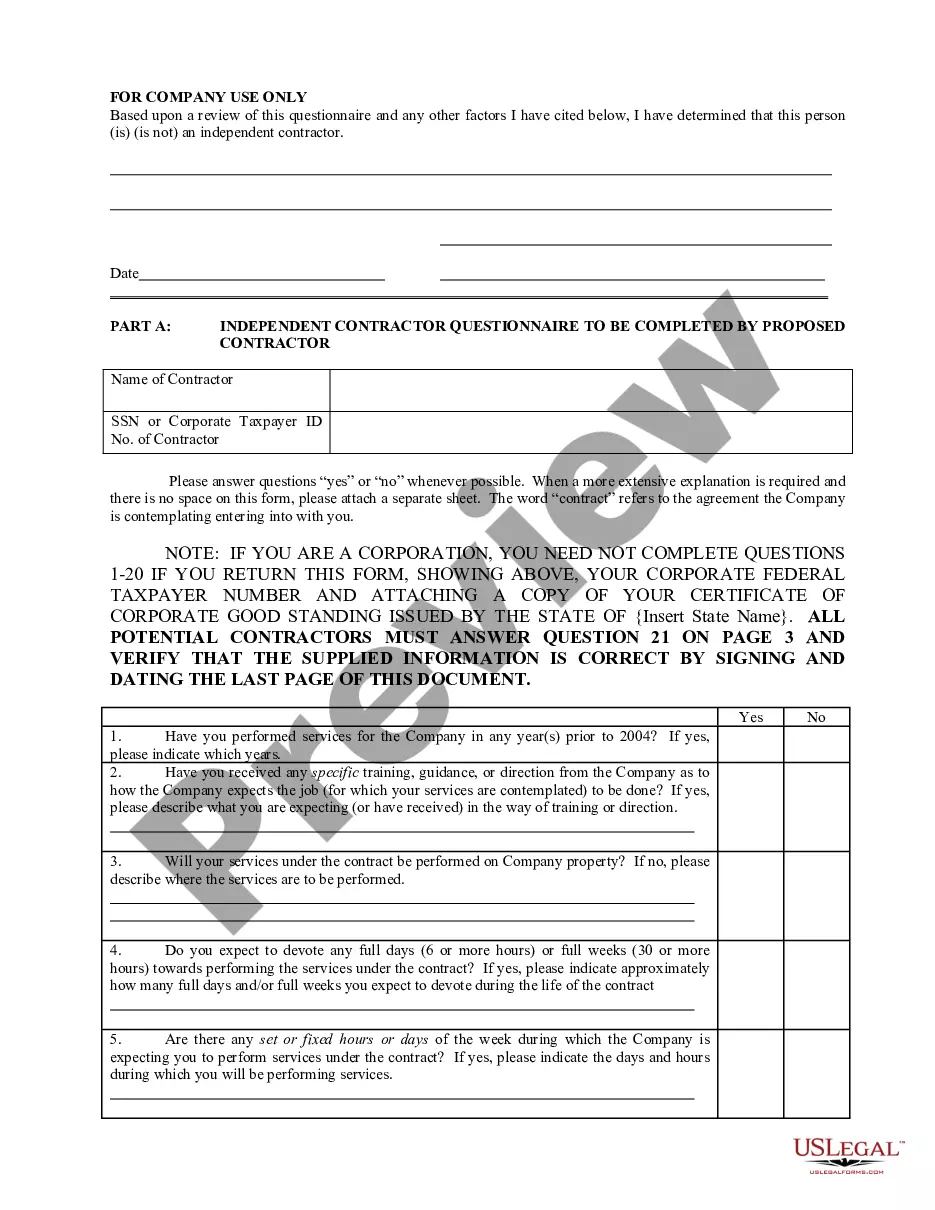

- Identification of the parties involved in the contractor relationship.

- Analysis of control factors, including the right to direct work and the degree of supervision.

- Details on payment structures employed in the relationship.

- Consideration of the provision of tools and materials necessary for the work.

- Clarification of the nature and frequency of the relationship between the parties.

When this form is needed

This form should be used when there is uncertainty about whether a contractor should be classified as an independent contractor or an employee. It is particularly useful in situations such as: evaluating working relationships during audits, establishing contractor agreements, determining workers' compensation eligibility, or navigating tax classifications with the IRS.

Intended users of this form

This form is intended for:

- Employers looking to clarify the status of their contractors.

- Independent contractors seeking to understand their employment classification.

- Legal professionals assisting clients with employment status assessments.

- Accountants handling tax-related inquiries for businesses.

How to prepare this document

- Identify the parties involved, including the contractor and the contracting entity.

- Analyze the control factors by answering questions about the relationship.

- Document payment information to clarify payment methods and frequency.

- Specify the tools and materials used by the contractor in their work.

- Complete any necessary fields regarding the nature of the working relationship.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to accurately analyze the control factors involved in the relationship.

- Ignoring state-specific labor laws that may affect classification.

- Assuming ongoing relationships indicate employment status without further evaluation.

Advantages of online completion

- Convenient access to professionally drafted templates available for download.

- Editability allows users to personalize the form according to their specific situation.

- Reliability from forms created under the guidance of licensed attorneys.

Legal use & context

- Understanding the contractor-employee distinction is critical for compliance with labor laws.

- Using this form can help prevent misclassification, which can lead to legal repercussions.

- Clarifying the relationship can assist in ensuring proper payment of taxes and benefits.

Looking for another form?

Form popularity

FAQ

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work, not what will be done and how it will be done. Small businesses should consider all evidence of the degree of control and independence in the employer/worker relationship.

If the worker is paid a salary or guaranteed a regular company wage, they're probably classified as an employee. If the worker is paid a flat fee per job or project, they're more likely to be classified as an independent contractor.

A worker does not have to meet all 20 criteria to qualify as an employee or independent contractor, and no single factor is decisive in determining a worker's status. The individual circumstances of each case determine the weight IRS assigns different factors.

For the independent contractor, the company does not withhold taxes. Employment and labor laws also do not apply to independent contractors. To determine whether a person is an employee or an independent contractor, the company weighs factors to identify the degree of control it has in the relationship with the person.

There may be some factors suggesting a California worker is an employee and others suggesting he or she is an independent contractor. It is even possible that a worker can be considered an independent contractor for purposes of IRS tax filing, but they are considered an employee under California's wage and hours laws.

The three current main tests are the following. Mutuality of obligation the obligation to provide work, or to pay for work done, and the individual's obligation to perform that work.Control whether control by the engager, or the right to control exists over the individual.

Finally, the new stimulus bill provides independent contractors with paid sick and paid family leave benefits through March 14, 2021.Under CARES Act II, unemployed or underemployed independent contractors who have an income mix from self-employment and wages paid by an employer are still eligible for PUA.