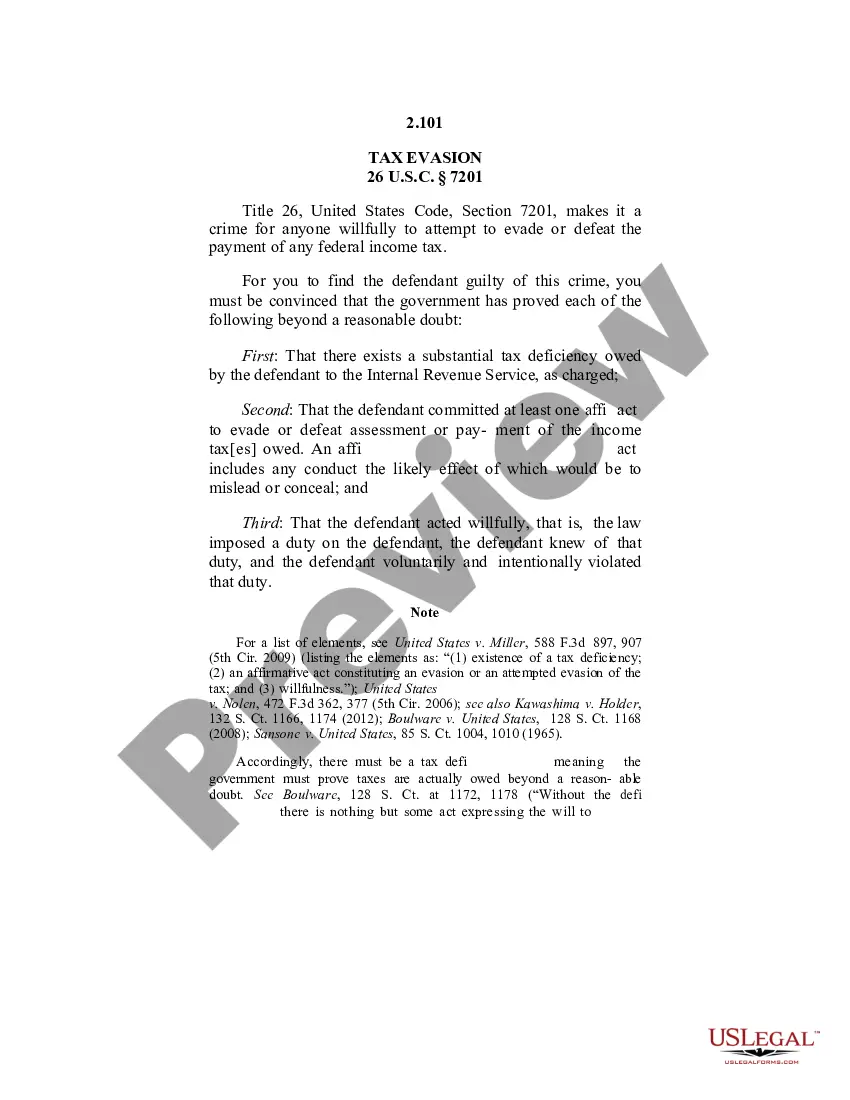

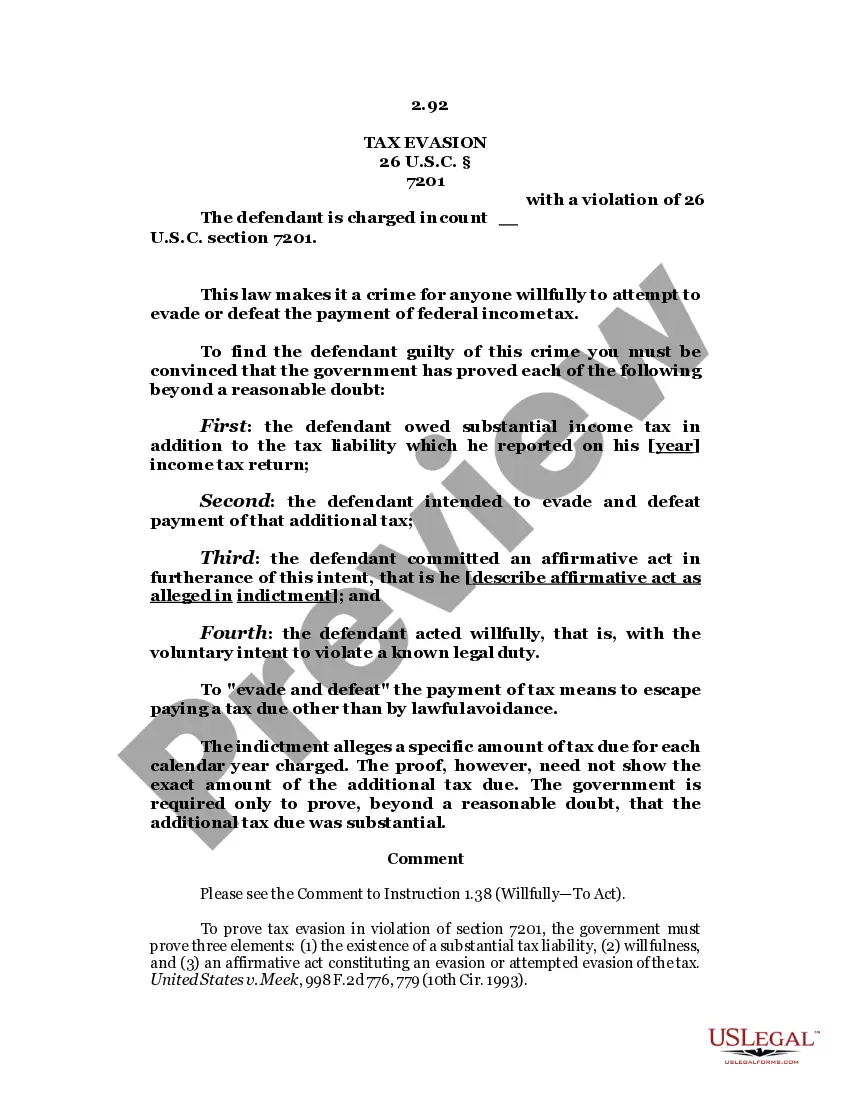

Tax Evasion - Willfully Defined (revised 2014)

Overview of this form

The Tax Evasion - Willfully Defined form clarifies the legal definition of willfulness in the context of tax evasion. It outlines what constitutes a voluntary and intentional violation of tax laws, differentiating it from mere negligence or mistakes. This form is essential for understanding legal responsibilities and defenses related to tax offenses, helping individuals navigate complex tax law issues effectively.

Key parts of this document

- Definition of willfulness: Describes voluntary and intentional violations of known legal duties.

- Conditions that exempt conduct from being considered willful: Discusses scenarios like negligence or good faith belief.

- Court references: Cites significant cases that clarify the meaning of willfulness in tax law.

- Jury instructions: Provides guidelines for juries on assessing claims of good faith misunderstandings.

")

")

When to use this form

This form is useful when addressing charges of tax evasion where the defendant's intent needs to be established. It is particularly relevant in cases where there may be arguments about whether the defendant acted willfully or under a genuine misunderstanding of tax obligations. This form can help clarify defenses based on willfulness, guiding legal professionals in court proceedings.

Who needs this form

- Individuals facing tax evasion charges who need to understand legal definitions.

- Lawyers representing clients in tax-related cases.

- Taxpayers looking to clarify their legal duties and potential defenses against charges of tax evasion.

- Students or professionals studying tax law and related legal principles.

Steps to complete this form

- Review the definition of willfulness to understand its legal implications.

- Analyze the specific circumstances surrounding the alleged tax violation.

- Collect evidence that supports claims of negligence or misunderstanding.

- Prepare jury instructions that align with the form's legal standards.

- Consult legal counsel for advice on application in relevant tax cases.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Assuming that negligent behavior constitutes willfulness.

- Failing to adequately present evidence of good faith misunderstandings.

- Not citing relevant case law which supports the argument of ignorance of tax laws.

Advantages of online completion

- Access to up-to-date legal definitions and guidance without geographic limitations.

- Editable formats that allow users to customize their legal documentation quickly.

- Instant download options enhance convenience and preparation speed.

Legal use & context

- The form provides a clear definition of willfulness, which is critical in tax law.

- Understanding willfulness can significantly impact the outcome of tax evasion cases.

- Legal representation can leverage this form for effective defense strategies.

Looking for another form?

Form popularity

FAQ

Generally, the IRS can include returns filed within the last three years in an audit. If we identify a substantial error, we may add additional years. We usually don't go back more than the last six years. The IRS tries to audit tax returns as soon as possible after they are filed.

The lookback period is the five-year period before the excess benefit transaction occurred. The lookback period is used to determine whether an organization is an applicable tax-exempt organization.

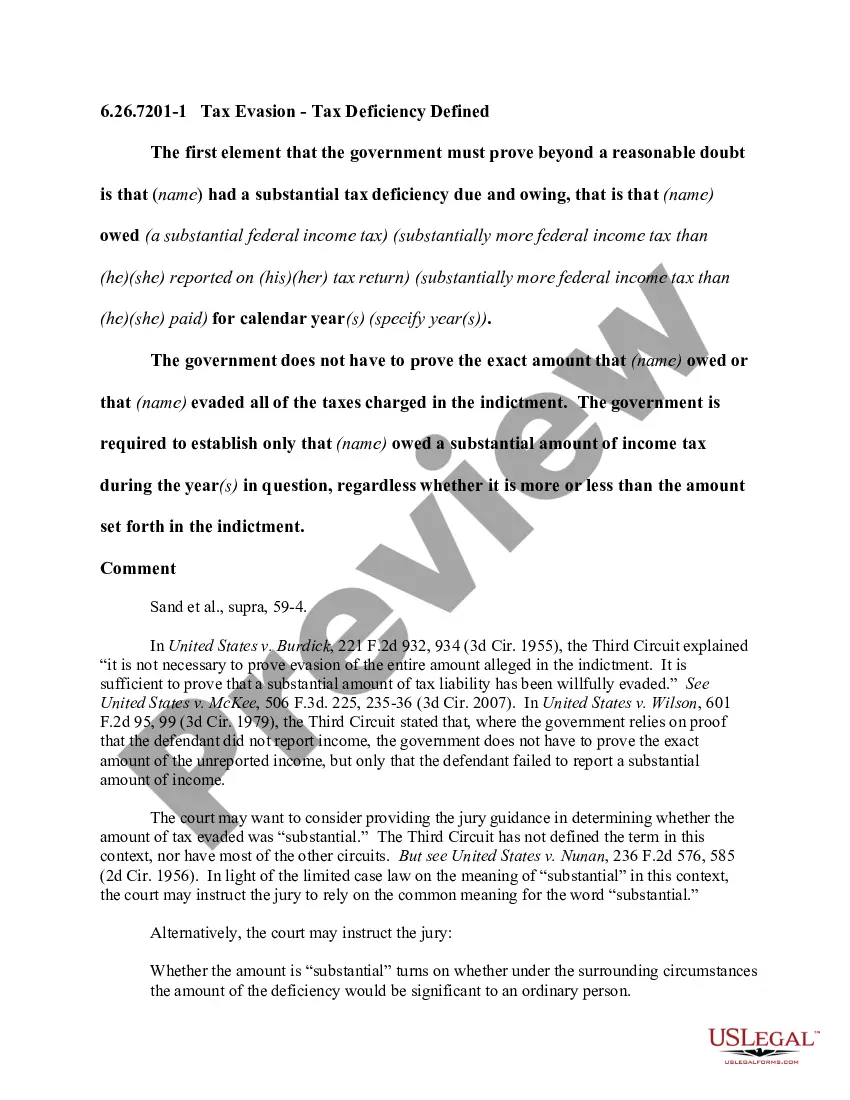

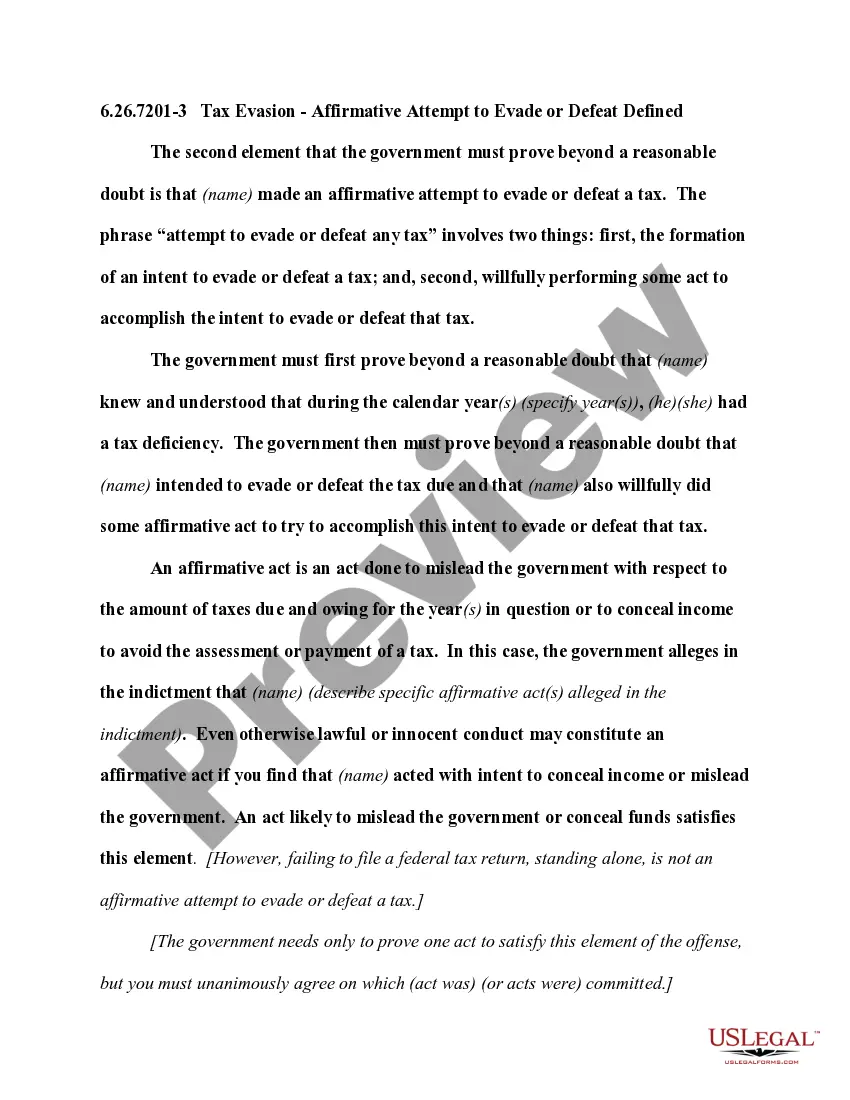

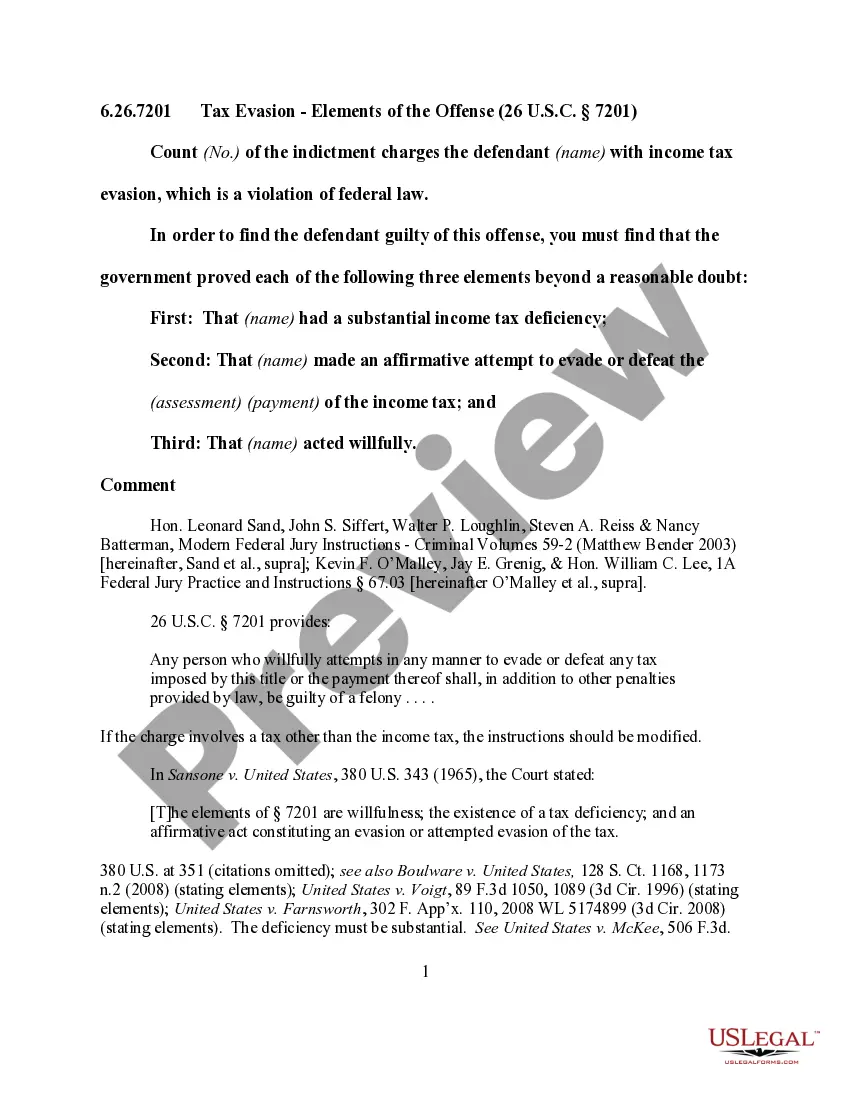

The three elements of tax evasion are: The existence of a tax deficiency. An attempt to evade or defeat tax. The taxpayer's willingness.

1 Two kinds of tax evasion. Section 7201 creates two offenses: (a) the willful attempt to evade or defeat the assessment of a tax, and (b) the willful attempt to evade or defeat the payment of a tax. Sansone v. United States, 380 U.S. 343, 354 (1965).

The average jail time for tax evasion is 3-5 years. Evading tax is a serious crime, which can result in substantial monetary penalties, jail, or prison. The U.S. government aggressively enforces tax evasion and related matters, such as fraud.

Willful Failure to Pay Income Taxes Tax fraud is a deliberate attempt to evade taxes or to defraud the IRS. Tax fraud takes place when a person or company willfully does one of the following: Intentionally fails to pay taxes owed. Willfully fails to file a federal income tax return. Fails to report all income.

The federal tax statute of limitations describes the time the IRS has to file charges against you if you are suspected of tax fraud. In most cases, the IRS can audit your tax returns up to three years after you file them, which means the tax return statute of limitations is three years.