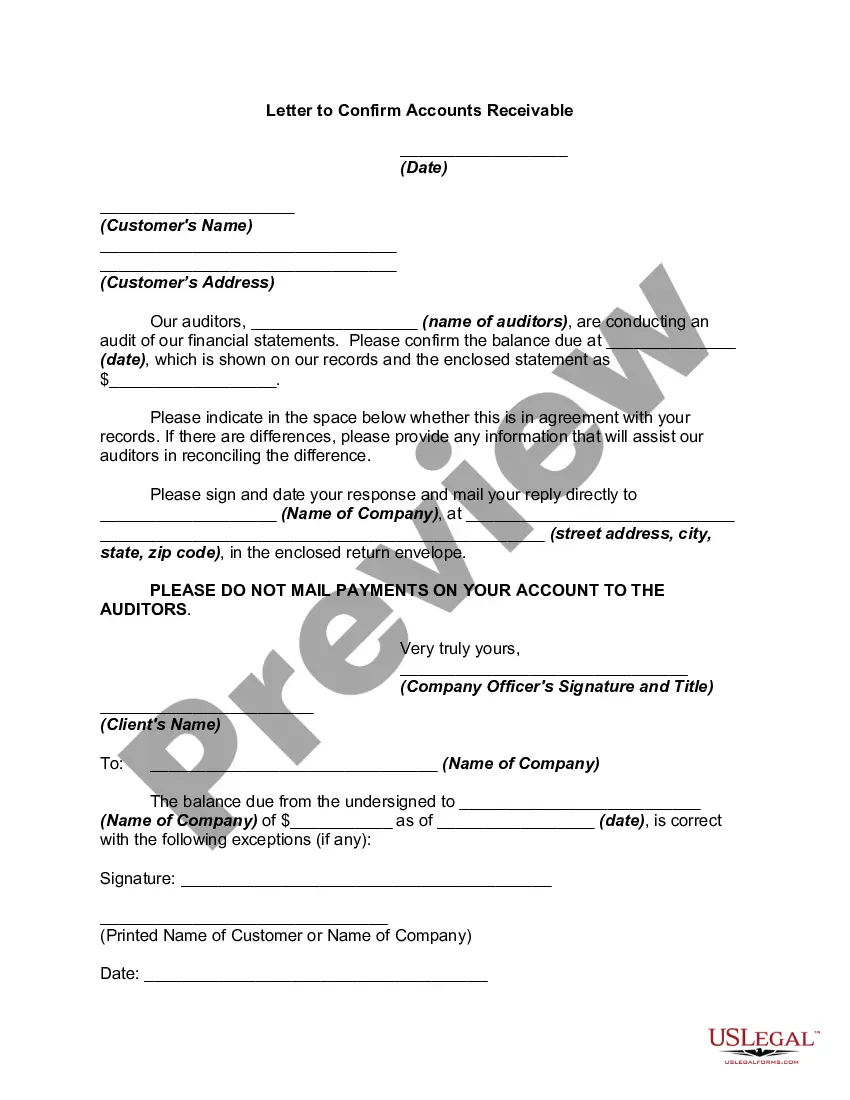

Request for Verification of Receivable During Audit

What is this form?

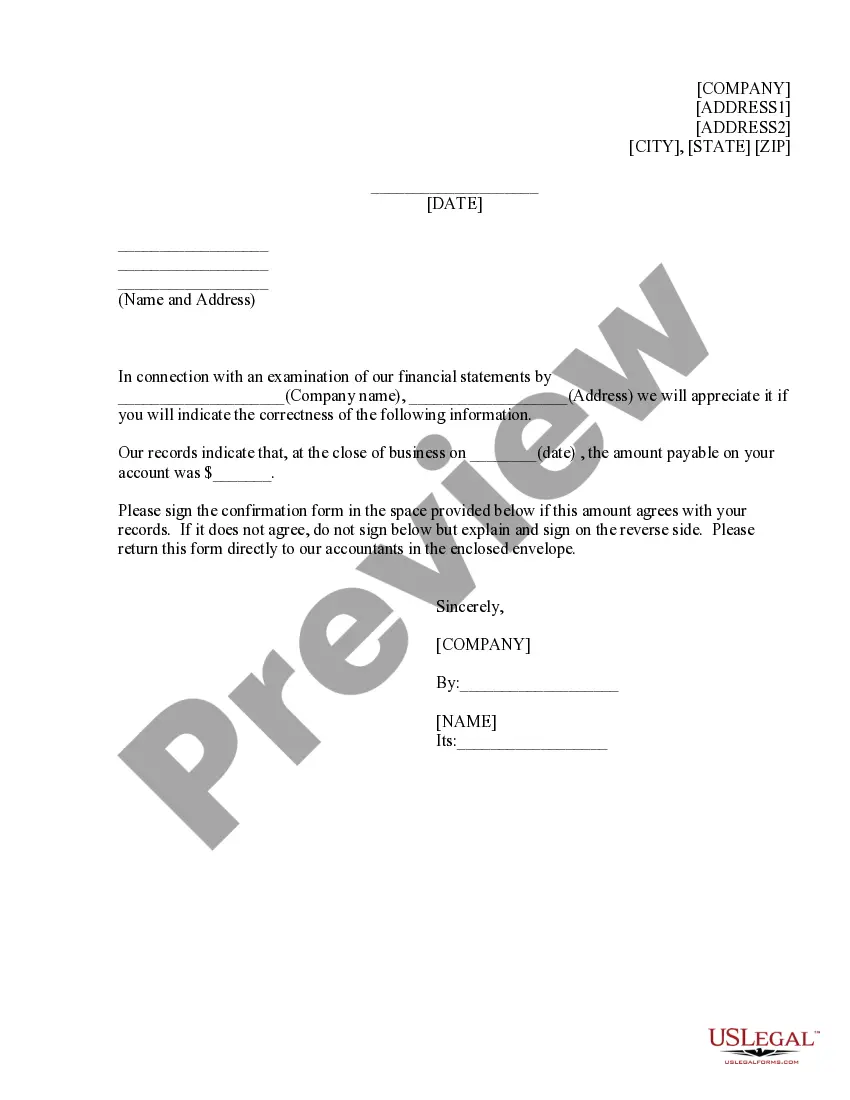

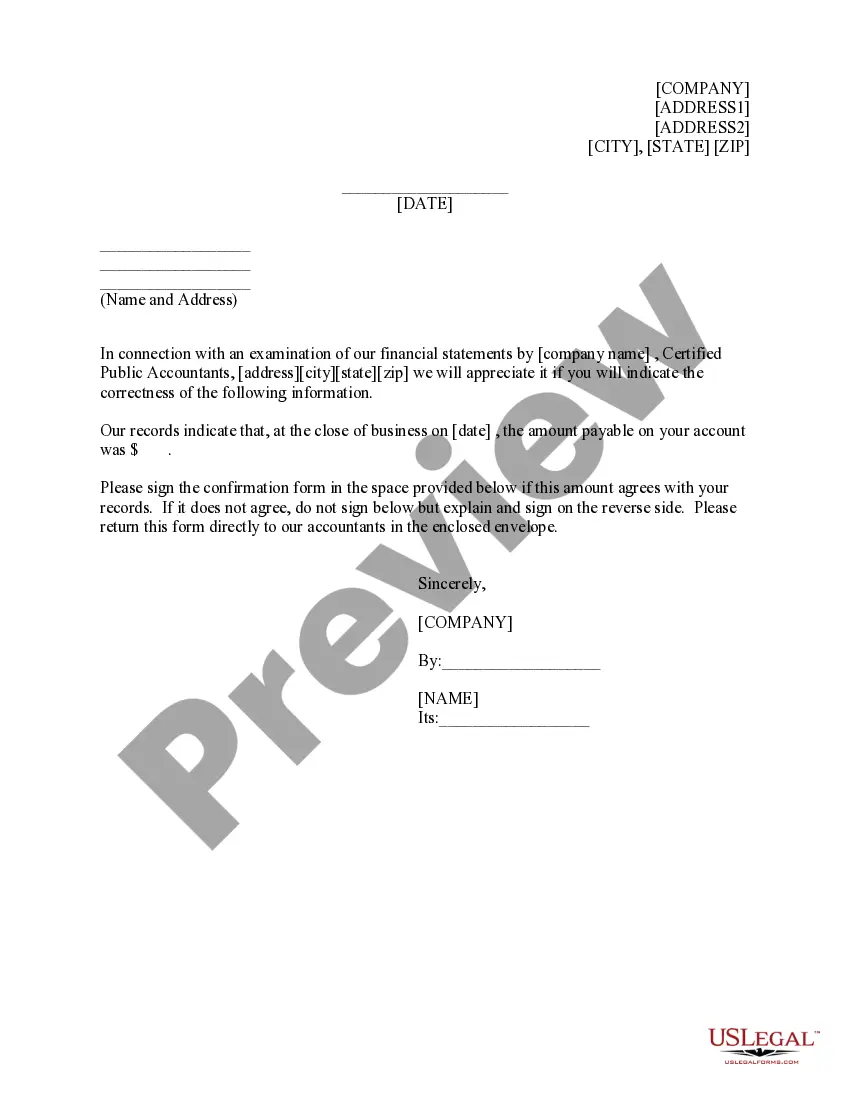

The Request for Verification of Receivable During Audit is a legal document used by companies during an audit process to confirm outstanding receivables with their clients. This form serves as a formal request for clients to verify account balances that a business claims are due. By using this form, businesses can ensure accuracy in their financial statements and clarify any discrepancies in account balances with clients.

Main sections of this form

- Business address: The address of the company sending the request.

- Date: The date on which the request is being made.

- Recipient information: Name and address of the client whose receivable is being verified.

- Amount due: The amount the business claims is owed by the client at the end of the business day specified.

- Confirmation section: A space for the client to confirm the correctness of the amount or provide an explanation if it does not match their records.

- Return instructions: Details on how and where to return the completed form.

When to use this form

This form should be used during a financial audit when a business needs to verify outstanding receivables with clients. It is particularly important when preparing financial statements to ensure that all accounts are accurate and up to date. Utilizing this form can prevent financial discrepancies and ensure compliance with accounting standards.

Intended users of this form

- Businesses undergoing an audit that need to confirm account balances with clients.

- Accountants and financial officers responsible for preparing accurate financial statements.

- Companies seeking to maintain transparent financial records with their clients.

How to complete this form

- Enter the business address in the designated fields provided at the top of the form.

- Input the date when the request is being made.

- Add the name and address of the client whose receivable you wish to verify.

- Specify the amount due as per your records on the given date.

- Provide a space for the client to confirm the amount or to explain any discrepancies.

- Sign the document in the designated area to validate the form.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include the correct recipient information, which may delay the verification process.

- Omitting the date, leading to confusion about when the request was made.

- Not providing enough space for the client to explain discrepancies, which can complicate the resolution process.

- Forgetting to sign the form before sending it to the client.

Benefits of completing this form online

- Convenience: Download and complete the form from anywhere without the need for physical documentation.

- Editability: Easily modify the form to fit your specific needs before sending it out.

- Reliability: Forms are drafted by licensed attorneys, ensuring they meet legal standards for verification requests.

Looking for another form?

Form popularity

FAQ

Audit Basics: Confirmation Letters The auditor selects the items for which they will request confirmation.The auditor designs the confirmation requests and tailors them to specific audit objectives.The auditor communicates the confirmation request to the third party by sending out the audit confirmation letter.

Is the confirmation of cash and accounts receivable required ing to auditing standards? Yes, usually required by auditing standards but auditors can choose not to in certain situations. It then becomes the auditors responsibility to gather evidence which can take much more time.

Book debts can be verified by the books of accounts and those should be supported by sale documents. Book balances should be sent to debtors directly for confirmation. It will establish the existence of book debts. Ownership of book debts can be verified with the sales documents and the sales ledger.

The auditor does so with an accounts receivable confirmation. This is a letter signed by a company officer (but mailed by the auditor) to customers selected by the auditors from the company's accounts receivable aging report.

It is acceptable to confirm accounts receivable prior to the balance sheet date if the internal controls are adequate and can provide reasonable assurance that sales, cash receipts, and other credits are properly recorded between the date of the confirmation and the end of the accounting period.

Auditing your receivables is important because it sheds light upon the status of a business' incoming cash. In addition to validating your financial records, the outcomes presented on the auditing reports also let you check whether you have unsent invoices, and whether your customers pay their invoices on time.

In many situations, both confirmation of accounts receivable and other substantive tests of details are necessary to reduce audit risk to an acceptably low level for the applicable financial statement assertions.