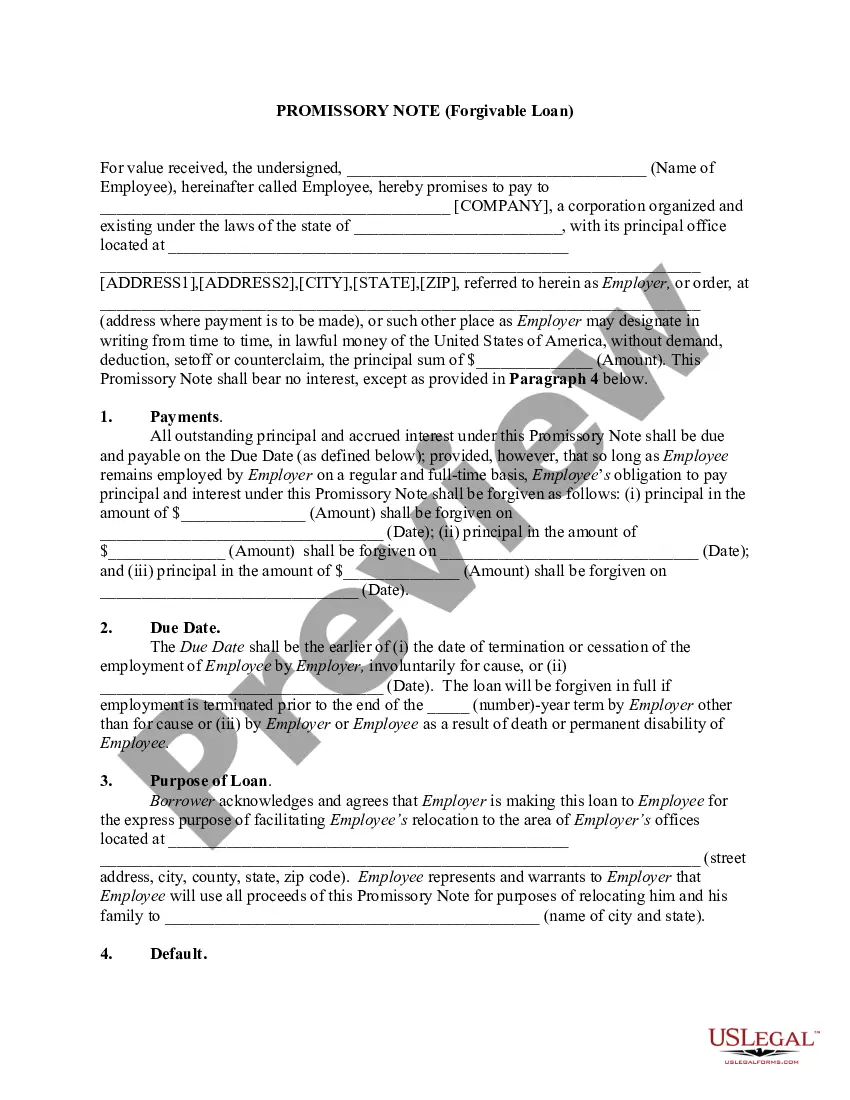

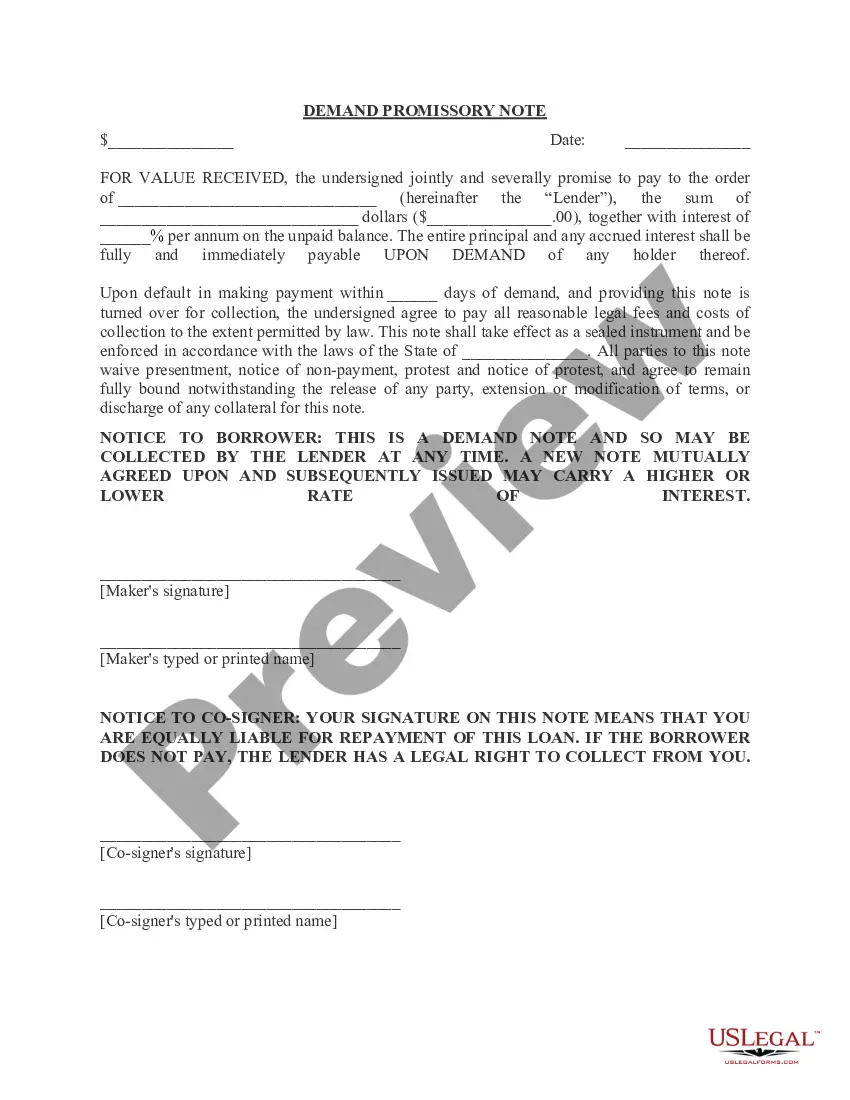

Promissory Note - Forgivable Loan

What is this form?

A Promissory Note - Forgivable Loan is a written agreement where an employee promises to repay a loan provided by their employer. This type of loan is often forgiven over time or upon certain conditions, such as the employee remaining with the company. It differs from standard promissory notes because it includes provisions for forgiveness based on employment status, making it a valuable option for both employers and employees in relocation or financial assistance situations.

What’s included in this form

- Parties Involved: Identifies the employee and employer by name and address.

- Loan Amount: Specifies the principal sum to be loaned.

- Forgiveness Terms: Details when and how much of the loan will be forgiven based on employee performance and time.

- Default Clause: Outlines the consequences if the employee fails to meet repayment obligations.

- State Law Governing: Indicates which state's law applies to the agreement.

When to use this document

This form is typically used when an employer provides financial assistance to a new employee, usually to help with relocation or setup costs. It is ideal for situations where the employer wishes to incentivize the employee to remain with the company for a specified period, highlighting both the benefits of financial support and the potential for forgiveness.

Intended users of this form

- Employers offering relocation assistance to new hires.

- Employees receiving a forgivable loan as part of their employment package.

- Human resources professionals organizing loan agreements for staff.

How to prepare this document

- Identify the parties by entering the full names and addresses of the employee and employer.

- Specify the total loan amount being provided.

- Outline the forgiveness schedule by detailing amounts and relevant dates.

- Include the due date for repayment in case of default.

- Ensure both parties sign and date the agreement for validity.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, having it notarized can add an extra layer of security and verification for both parties.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to specify all forgiveness conditions clearly.

- Not including repayment terms, leading to misunderstandings.

- Leaving out the due date for repayment, which could cause confusion if the employee leaves the job.

Why complete this form online

- Convenience of accessing the form anytime and from anywhere.

- Ability to customize the agreement to fit specific circumstances.

- Regular updates by legal professionals ensure the form meets current laws.

Legal use & context

- This form is legally binding when signed by both parties.

- It provides protection for the employer and outlines the employee's responsibilities.

- Enforcement may vary based on state laws and circumstances surrounding employment termination.

Quick recap

- A Promissory Note - Forgivable Loan is useful for employer-employee relocation benefits.

- Clearly define all terms related to the loan and conditions for forgiveness.

- Both parties need to sign and, if necessary, consider notarization for added legitimacy.

Looking for another form?

Form popularity

FAQ

Promissory Note - Forgivable Loan is a written agreement in which an employer lends money to an employee with forgiveness available under certain conditions. It is typically used for relocation or setup costs, with forgiveness tied to continued employment or performance. The agreement lists the loan amount, forgiveness terms, a default clause, and the governing state law.

A forgivable loan agreement is a loan that may be forgiven if specific conditions—such as remaining employed for a set period or meeting performance milestones—are met. In Promissory Note - Forgivable Loan, forgiveness terms detail when and how much of the loan is forgiven, and a default clause outlines remedies if conditions aren’t satisfied.

In Promissory Note - Forgivable Loan, you generally don’t have to repay the forgiven portion if the stated conditions are met. If those conditions aren’t met, the loan may become due according to the agreement. The default clause describes consequences if repayment obligations are not fulfilled.

Yes. A standard promissory note is typically repaid in full, but Promissory Note - Forgivable Loan includes forgiveness based on employment- or time-based conditions. The Forgiveness Terms specify when and how much is forgiven, while the loan may still become due if the conditions aren’t satisfied.

Disadvantages can include reliance on employment status for forgiveness, meaning job changes or company policy shifts could affect the benefit. The form is more complex than a plain promissory note, with forgiveness terms and a default clause that influence when and how repayment may be required.

Promissory Note - Forgivable Loan differs from a standard promissory note because it contains Forgiveness Terms tied to employment status and tenure. A standard promissory note generally requires full repayment, while this form may forgive all or part of the loan under specified conditions, and it also includes a default clause and governing law.