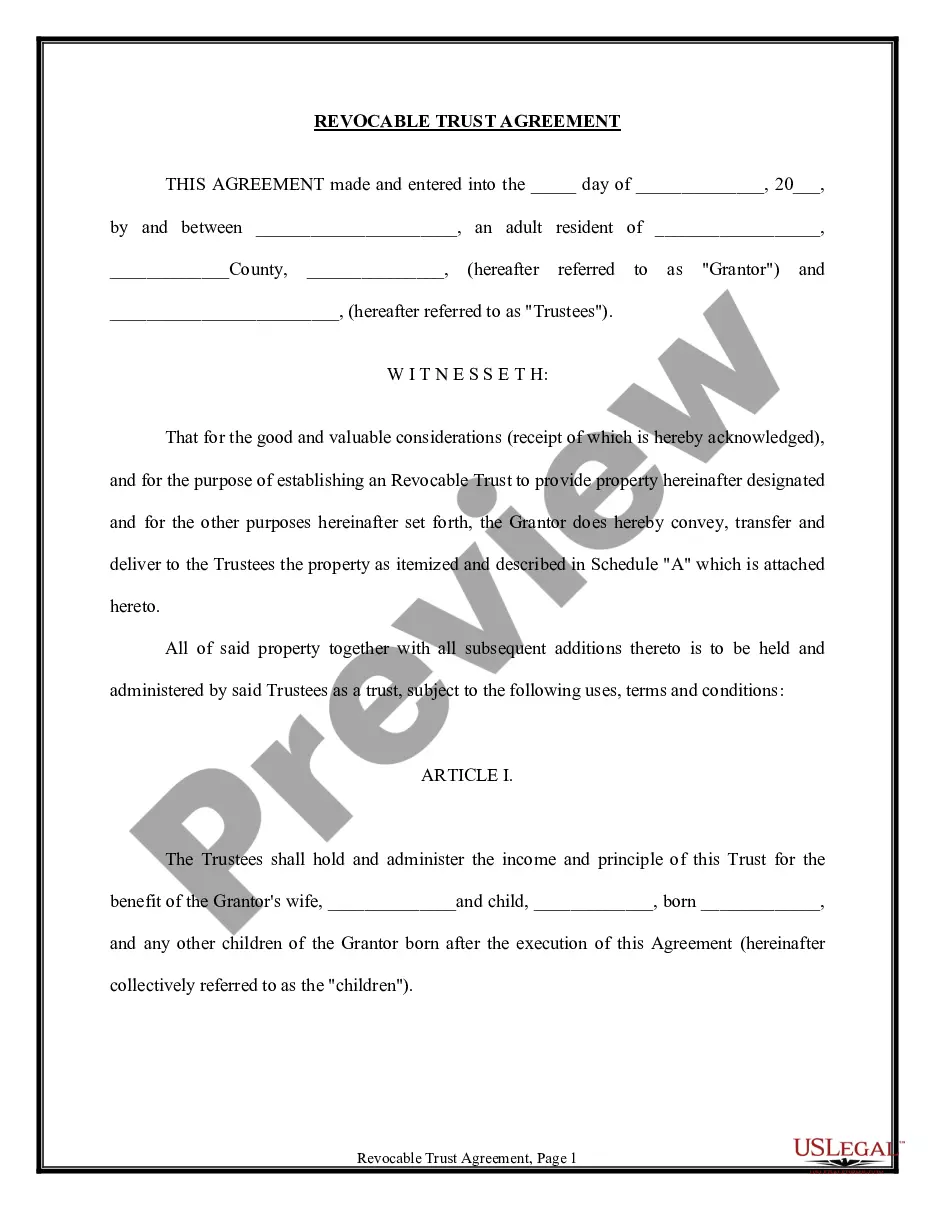

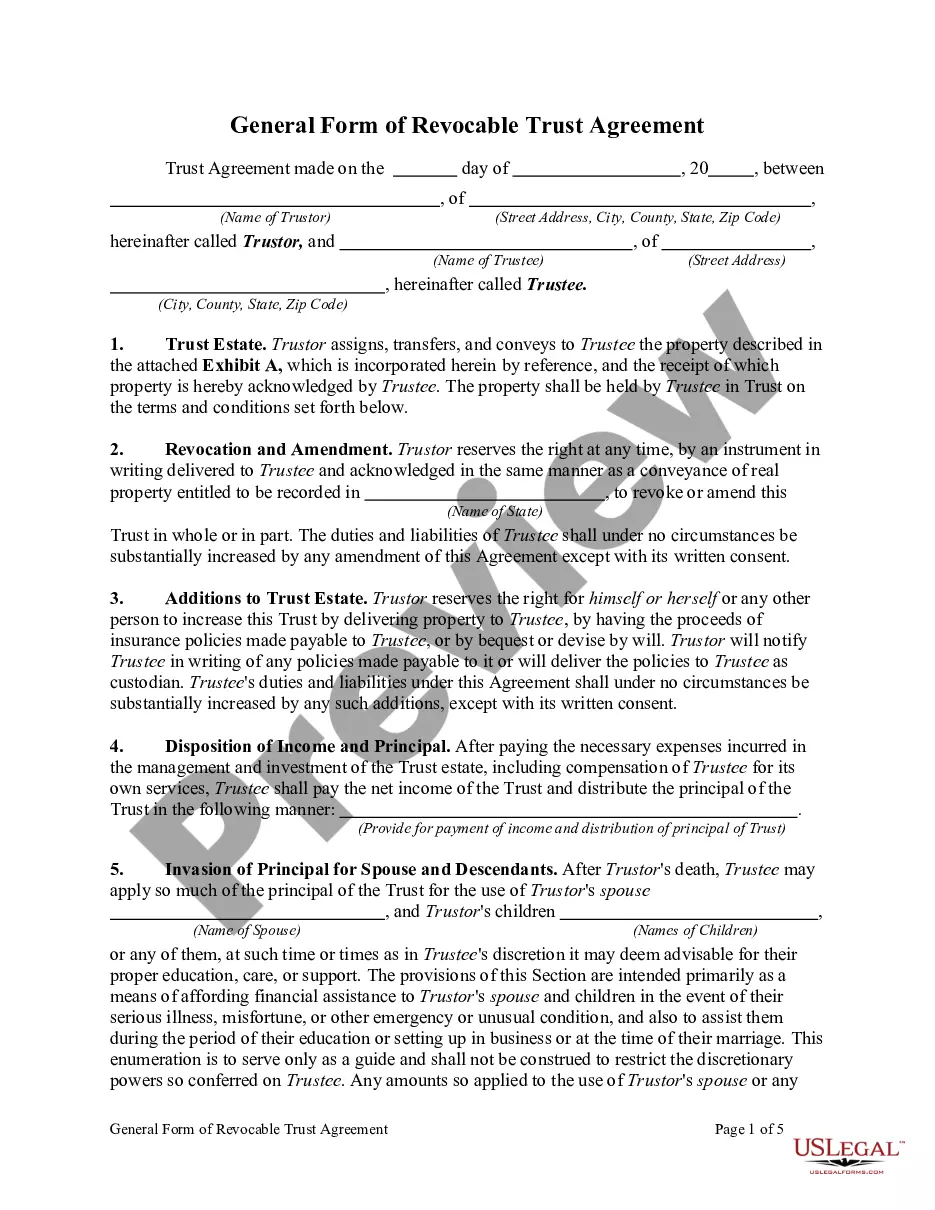

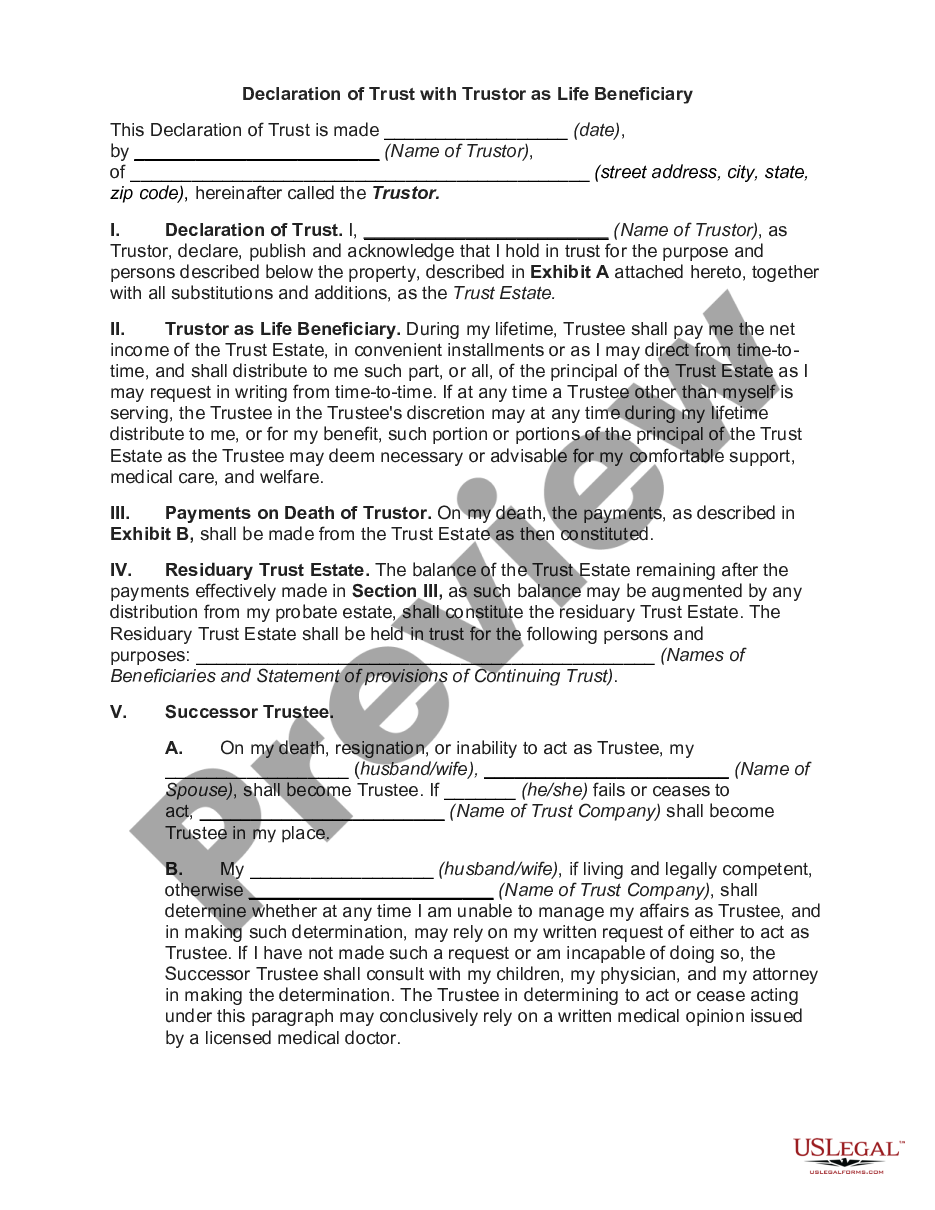

Revocable Trust Agreement - Grantor as Beneficiary

Overview of this form

The Revocable Trust Agreement - Grantor as Beneficiary is a legal document that establishes a trust whereby the grantor transfers property to a trustee while retaining the right to benefit from it during their lifetime. This type of trust is distinct because the grantor is also the beneficiary, allowing for flexibility in managing assets. It provides a means to control the distribution of assets while avoiding probate upon the grantor's death.

What’s included in this form

- Grantor and Trustee Identification: Specifies the parties involved in the agreement.

- Property Assignment: Describes the property transferred into the trust as listed on Schedule A.

- Beneficiary Designation: Identifies the grantor as the primary beneficiary of the trust assets.

- Trustee Powers: Outlines the authority and discretion afforded to the trustee regarding the management and distribution of trust assets.

- Trust Duration: States that the trust is effective during the grantor's lifetime and details what happens upon the grantor's death.

Situations where this form applies

This form should be used when an individual wishes to create a revocable trust, allowing them to manage their assets and designate beneficiaries effectively. It is particularly useful for estate planning purposes, where the grantor wants to ensure their assets are distributed according to their wishes without the delays and costs associated with probate court. Additionally, using this form is suitable when the grantor wants to retain control over the assets while providing for their personal needs and those of their dependents.

Who needs this form

- Individuals looking to create a revocable trust to manage their assets.

- Grantors who wish to remain the beneficiary of their trust assets during their lifetime.

- Those interested in avoiding probate for their estate upon death.

- People wanting to provide for their dependentsâ future needs while retaining control over their assets.

Instructions for completing this form

- Identify and enter the full names and addresses of the grantor and trustee.

- List the property to be included in the trust on Schedule A and ensure it is accurately detailed.

- Specify the name of the trust in the designated section.

- Detail the distribution terms for both income and principal from the trust.

- Have the grantor and trustee sign the document in the presence of a notary public.

Notarization requirements for this form

Yes, this form must be notarized to be legally valid. US Legal Forms offers integrated online notarization, accessible 24/7, allowing you to complete the notarization process via secure video call without the need to travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to list all properties on Schedule A, leading to incomplete asset transfers.

- Not clearly defining the trusteeâs powers, which can result in misunderstandings later.

- Omitting signatures or not completing notarization, making the trust invalid.

- Assuming all estate planning needs are covered without consulting a legal professional.

Advantages of online completion

- Convenience of completing the form from home at any time.

- Editability allows for easy revisions until finalized.

- Access to legal templates drafted by licensed attorneys ensures reliability.

Legal use & context

- A revocable trust helps avoid probate and allows for asset management during the grantor's lifetime.

- Trusts must comply with state laws to ensure enforceability and proper administration.

- Beneficiaries' rights and access to trust assets are defined by the terms of the trust agreement.

Summary of main points

- The Revocable Trust Agreement allows the grantor to retain control over their assets while providing for beneficiaries.

- Properly completing and maintaining the trust can facilitate estate planning and asset management.

- Consulting with a legal professional is recommended to ensure compliance with state-specific regulations.

Looking for another form?

Form popularity

FAQ

If you are talking about an irrevocable trust, then no, the grantor should not be the trustee. One of the purposes behind an irrevocable trust is to typical get assets OUT of the grantor's estate, for various reasons. Having the grantor as a trustee (or beneficiary) would defeat that purpose.

Someone who inherits money from a revocable trust receives it tax-free, but the estate might have to pay estate tax on everything that it contains before distributing it.

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust's income, rather than the trust itself paying the tax. However, such beneficiaries are not subject to taxes on distributions from the trust's principal.

The person or people benefiting from the trust are the beneficiaries. Because a revocable trust lists one or more beneficiaries, the trust avoids probate, which is the legal process of distributing assets of a will.

The grantor (as an individual or couple) transfers their assets to an irrevocable trust. However, unlike other irrevocable trusts, the grantor can be the income beneficiary. Their children or spouse would be the residual beneficiaries.

The Revocable Trust tax implications, following the death of the Grantor, impact both the Grantor's Estate and the Beneficiaries'.However, any income earned by the Trust assets or principal after the date of the Grantor's death is reported in a separate tax return for the Trust.

The short answer is yes, a trustee can also be a trust beneficiary. One of the most common types of trust is the revocable living trust, which states the person's wishes for how their assets should be distributed after they die.

In a Revocable Living Trust, the grantor and the trustee are usually the same person.Beneficiaries: the people who will receive the benefit of the trust's assets. The Grantor (you) is the original beneficiary, and those who receive benefits after your passing are known as "remainder beneficiaries".

A beneficiary is the person or persons who are entitled to the benefit of any trust arrangement. A beneficiary will normally be a natural person, but it is perfectly possible to have a company as the beneficiary of a trust, and this often happens in sophisticated commercial transaction structures.