South Carolina Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

Have you found yourself in a situation where you require documents for either business or personal purposes almost constantly.

There are numerous credible document templates accessible online, but finding ones you can trust is not easy.

US Legal Forms offers thousands of document templates, such as the South Carolina Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself, which are designed to comply with federal and state requirements.

Once you have the correct template, simply click Get now.

Choose the payment plan you prefer, fill out the necessary information to create your account, and pay for the transaction with your PayPal or credit card.

- If you are already familiar with the US Legal Forms website and have an account, just Log In.

- Then, you can download the South Carolina Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself template.

- If you do not have an account and wish to use US Legal Forms, follow these steps.

- Find the template you need and ensure it is for your correct city/region.

- Use the Review button to check the form.

- Read the summary to make sure you have selected the right template.

- If the template isn't what you're looking for, use the Search field to locate the form that meets your needs.

Form popularity

FAQ

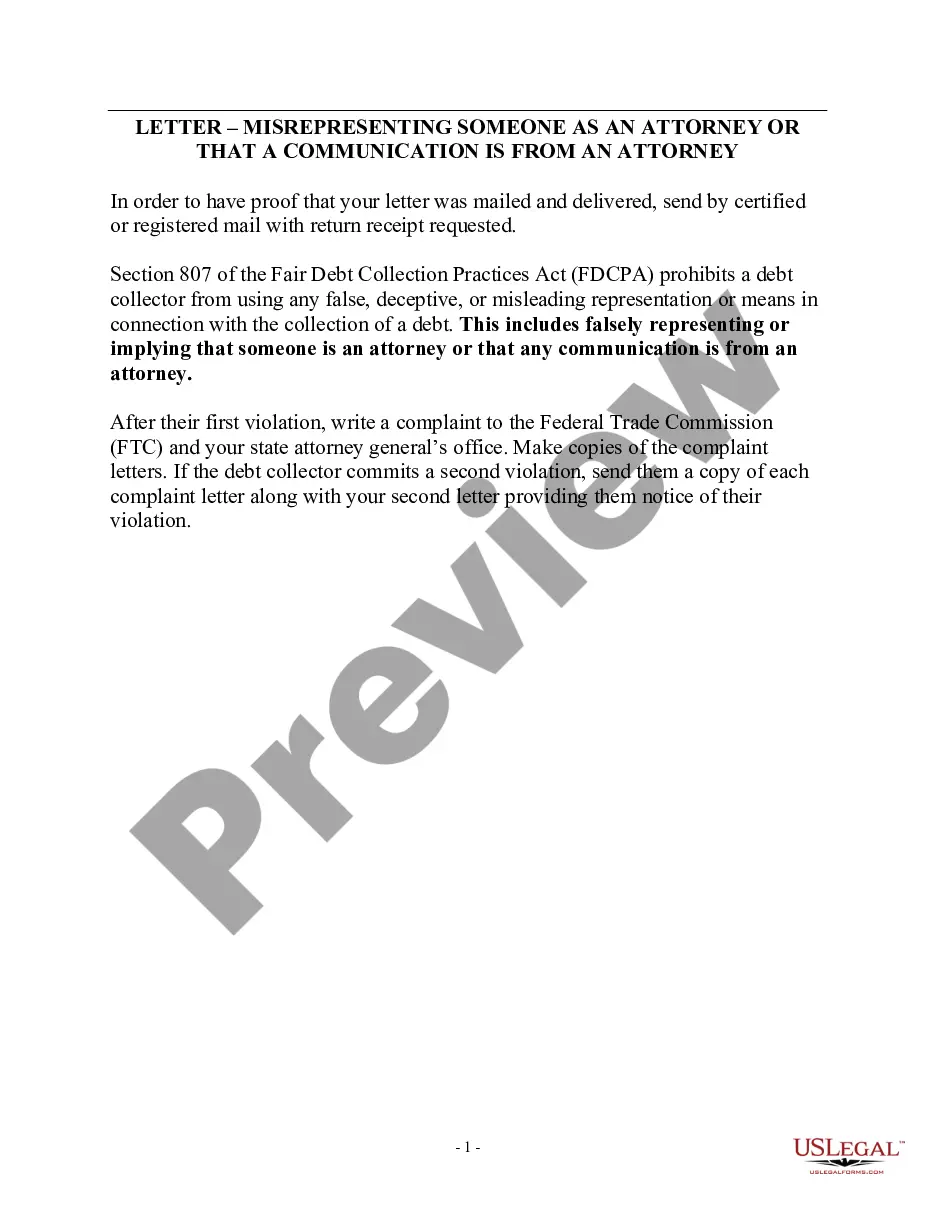

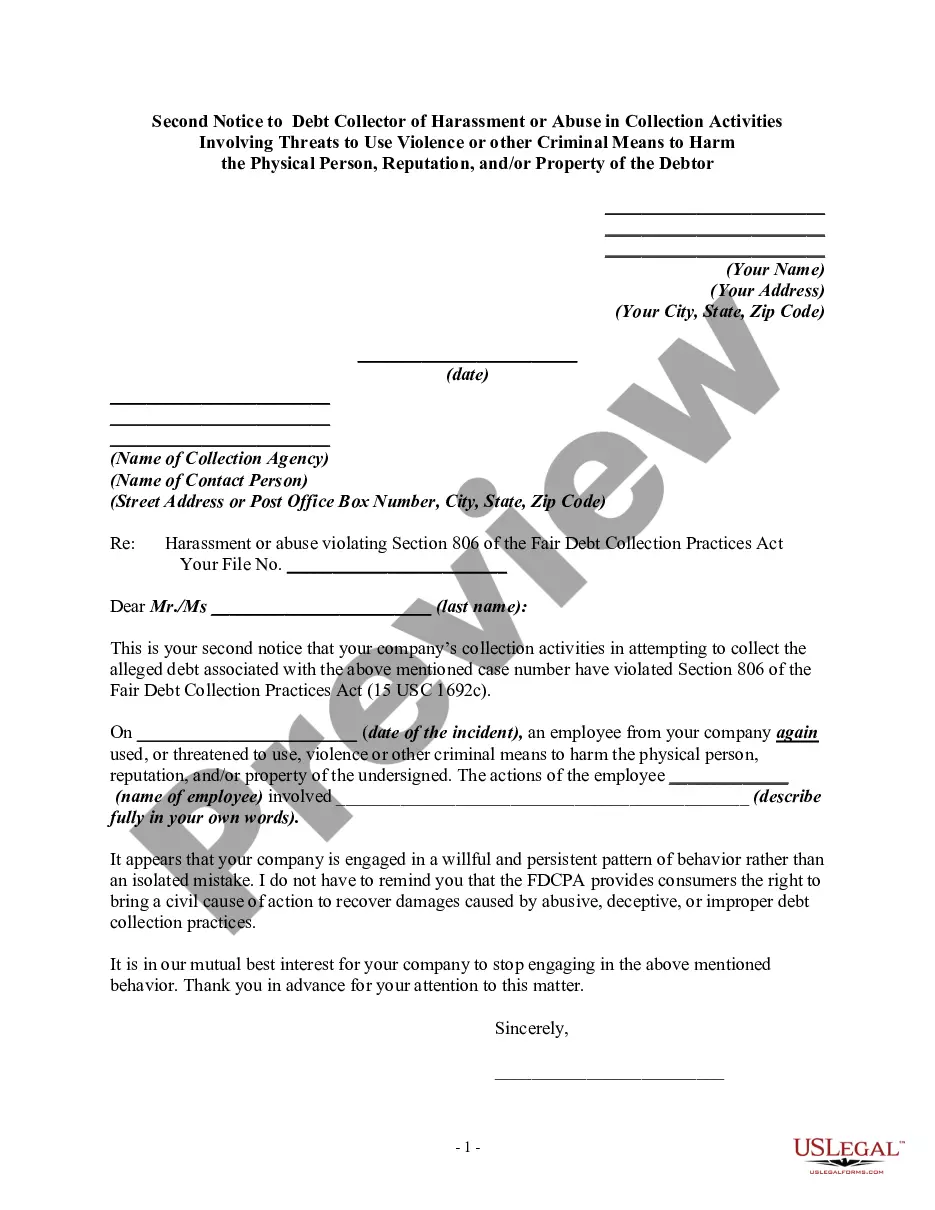

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

The law makes it illegal for debt collectors to harass debtors in other ways, including threats of bodily harm or arrest. They also cannot lie or use profane or obscene language. Additionally, debt collectors cannot threaten to sue a debtor unless they truly intend to take that debtor to court.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Old Debt and the Statute of Limitations Under South Carolina law (S.C. Code § 15-3-530), the statute of limitations for most types of consumer and business debt is three (3) years.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

In South Carolina, creditors and debt collectors can only come after you for medical and credit card debt for three years. They can pursue you for mortgage debt for twenty years and state tax debt for ten years.

Judgments in South Carolina may not be renewed. The South Carolina Supreme Court has concluded that a judgment is utterly extinguished after the expiration of ten years from the date of entry. Hardee v.

In South Carolina mortgage debt has a statute of limitations of 20 years. This is quite long compared to consumer debt such as credit card debt, which has a statute of limitations of 3 years. Medical debt also holds a statute of limitations of 3 years, while auto loan debt is 6, and state tax debt is 10.

The state of South Carolina is one of four states that does not permit wage garnishment. However, state law does permit creditors to pursue garnishment against your bank account, effectively freezing your assets.