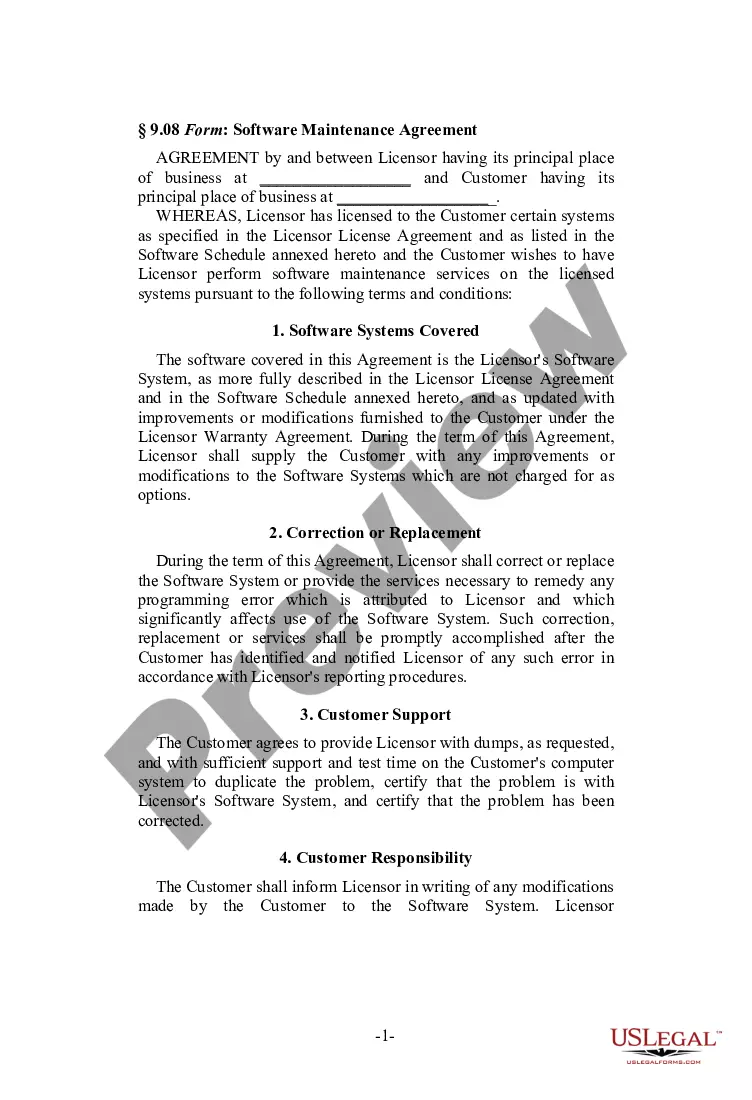

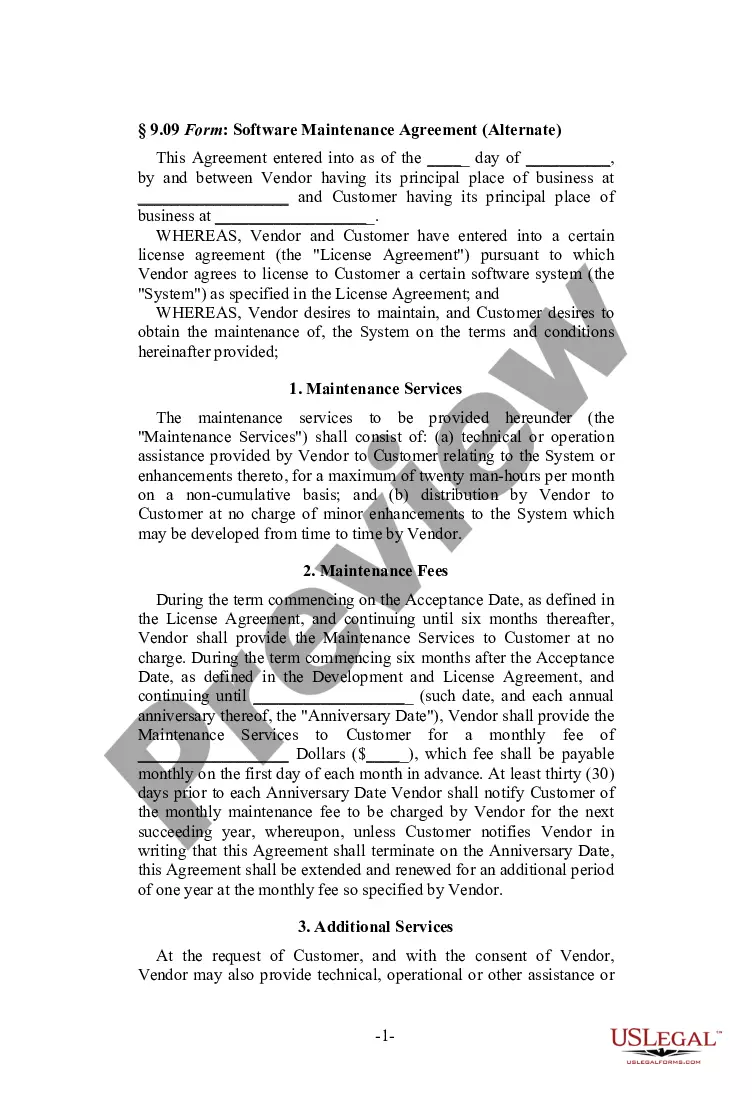

South Carolina Software Maintenance Agreement (Alternate)

Description

")

")

")

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Software Maintenance Agreement (Alternate)?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a vast selection of legal document templates that you can download or print.

By using the site, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can find the most recent forms such as the South Carolina Software Maintenance Agreement (Alternate) in just a few minutes.

If the form doesn't meet your requirements, use the Search field at the top of the screen to find one that does.

Once you are satisfied with the form, confirm your choice by clicking the Get now button. Then, select your preferred pricing plan and provide your information to register for an account.

- If you currently have a subscription, Log In and access the South Carolina Software Maintenance Agreement (Alternate) from your local US Legal Forms library.

- The Download button will appear next to each form you view.

- You can access all previously acquired forms in the My documents tab of your account.

- If you are new to US Legal Forms, here are simple steps to help you get started.

- Ensure you have selected the correct form for your location/region.

- Click the Preview button to review the content of the form.

Form popularity

FAQ

California: SaaS is not a taxable service. However, software or information that is delivered electronically is exempt. The ability to access software from a remote network or location is exempt. Under California sales and use tax law, there must be a transfer of TPP, in order to have a taxable event.

While software is not physical or tangible in the traditional sense, accounting rules allow businesses to capitalize software as if it were a tangible asset. Software that is purchased by a firm that meets certain criteria can be treated as if it were property, plant, & equipment (PP&E).

The Sales Tax is imposed on the sales at retail of tangible personal property and certain services. The Use Tax is imposed of the storage, use or consumption of tangible personal property and certain services when purchased at retail from outside the state for storage, use or consumption in South Carolina.

Yes. Charges for maintenance agreements (whether optional or mandatory) that are made in conjunction with, or as part of the sale of, computer software sold and delivered by tangible means are includable in "gross proceeds of sales" or "sales price", and, therefore, subject to the tax.

Maintenance, updating, and costs for adding to a website are treated as normal business expenses and are deductible when incurred if these costs are truly maintenance-type costs.

South Carolina Digital products are not taxable in South Carolina. Digital products are not specifically included in the definition of tangible personal property.

The majority of states which have addressed the issue and have concluded that software (at least unbundled software) is not tangible personal property for ad valorem tax purposes and therefore is generally not taxable.

Prescription medicines, groceries, and gasoline are all tax-exempt. Some services in South Carolina are subject to sales tax.

In a recent private letter ruling, the South Carolina Department of Revenue held that software subscription services are tangible personal property subject to sales and use taxes.

Except as provided in ? 1.199-3(j)(5)(ii) and 1.199-3(k)(2)(i), computer software, sound recordings, and qualified films are not treated as tangible personal property regardless of whether they are affixed to a tangible medium.