South Carolina FALSE STATEMENT TO FDIC

What is this form?

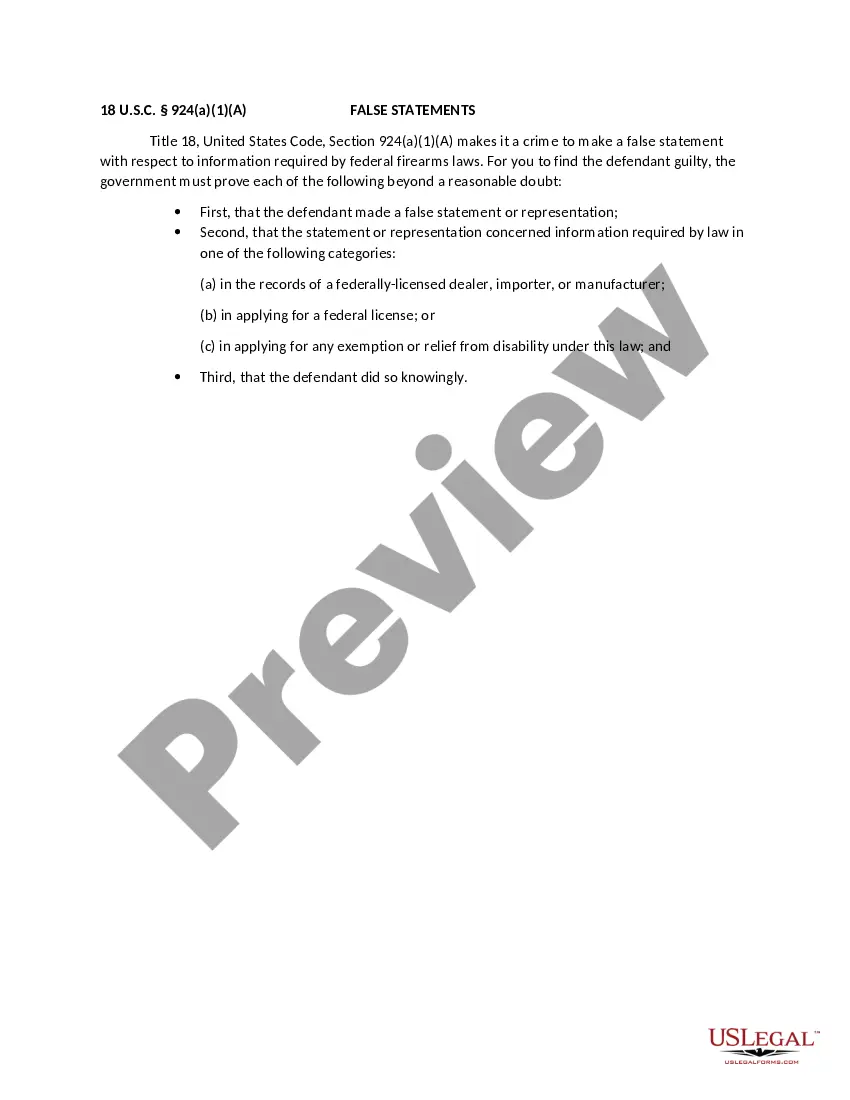

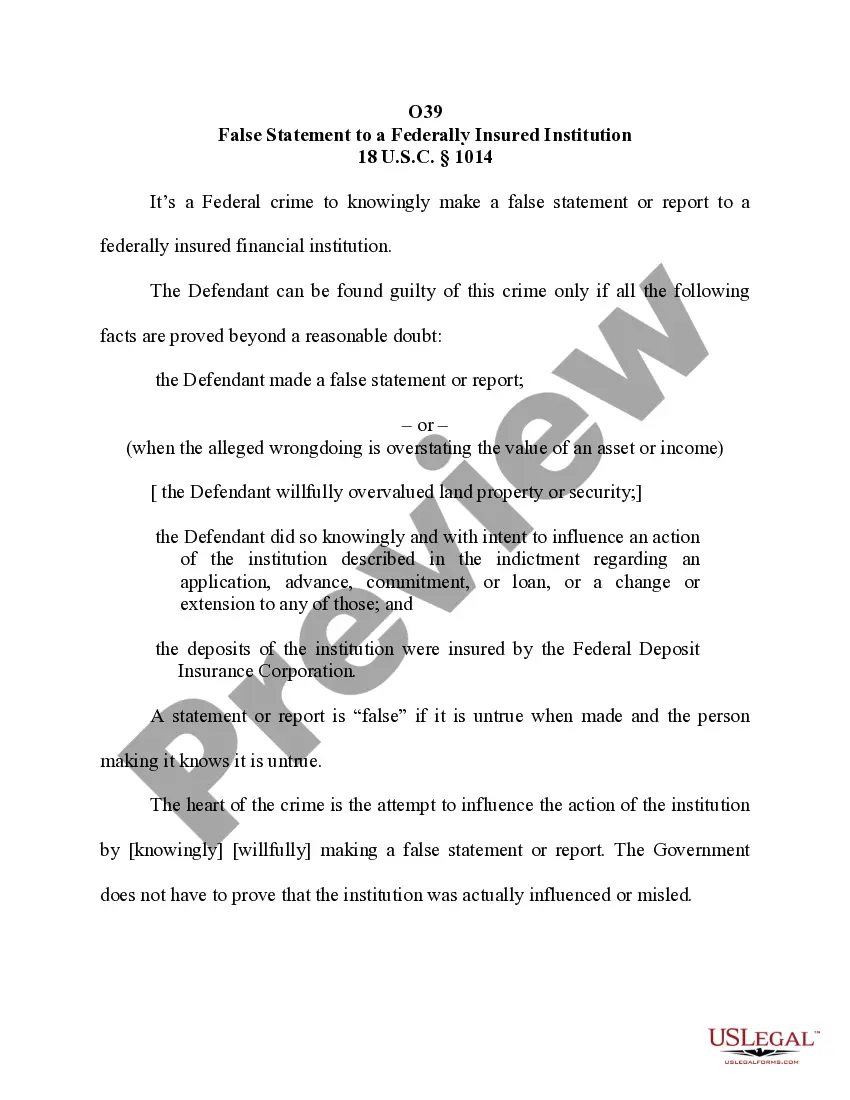

The False Statement to FDIC form is a legal document that addresses criminal violations under Title 18, United States Code, Section 1007. This form is used in cases where a defendant is accused of making false statements to influence the actions of the Federal Deposit Insurance Corporation (FDIC). It is important because it sets forth the specific legal standards that must be met to establish guilt in such cases, distinguishing it from other forms that may relate to different aspects of financial misconduct.

Key parts of this document

- Definition of false statement: Clarifies what constitutes a false, forged, or counterfeit statement in the context of influencing the FDIC.

- Elements of proof: Lists the three critical components the government must prove to establish a violation.

- Intent: Emphasizes the necessity of demonstrating that the defendant had knowledge of the falsity of the statement and intended to influence the FDIC.

Situations where this form applies

This form is used in legal situations where an individual is accused of making untrue statements or submitting fraudulent documents to the FDIC. It may arise during investigations into bank fraud, financial misrepresentation, or other financial crimes. Legal practitioners typically reference this form during trial preparations or in the course of defending against allegations of fraudulent behavior involving the FDIC.

Who can use this document

- Legal professionals representing individuals accused of making false statements to the FDIC.

- Federal prosecutors involved in cases against defendants charged under Section 1007.

- Individuals seeking to understand the legal implications of their actions concerning the FDIC.

Completing this form step by step

- Identify the parties involved, including the defendant and the government prosecuting the case.

- Provide the relevant factual background, including details of the alleged false statement and its impact on the FDIC.

- Outline the specific false statements or documents involved in the case.

- Include evidence or references to support the claim that the statement was intended to influence FDIC actions.

- Prepare to present arguments that address each element of proof required to establish or defend against the charges.

Does this form need to be notarized?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly establish knowledge of the falsity of the statement made.

- Neglecting to provide sufficient evidence connecting the false statement to actions taken by the FDIC.

- Confusing substantive legal standards with procedural requirements in presenting the case.

Why complete this form online

- Convenience of downloading legal forms anytime, enabling quick access during legal preparations.

- Editability allows legal professionals to tailor the form to specific cases before filing.

- Reliability of using professionally drafted forms created by licensed attorneys, ensuring compliance with legal standards.

Legal use & context

- The form is used in federal criminal trials to prove or defend against fraudulent behavior regarding false statements to the FDIC.

- Compliance with this form is essential for upholding the integrity of federal banking regulations.

Key takeaways

- The False Statement to FDIC form is vital for cases involving allegations of fraud against federal banking authorities.

- Understanding the elements required for proof can significantly impact the outcome of a case.

- Using online forms provides efficiency and accuracy in legal documentation.

Looking for another form?

Form popularity

FAQ

What Are Suspicious Transactions in Banking? Suspicious transactions are any event within a financial institution that could be possibly related to fraud, money laundering, terrorist financing, or other illegal activities.

Section 19 of the Federal Deposit Insurance Act prohibits individuals that are convicted of certain criminal offenses from participating in the affairs of an insured depository institution without the written consent of the FDIC.

Part 353 of FDIC Rules and Regulations and CFR1 Title 31, Chapter X, § 1020.320 of the Financial Crimes Enforcement Network (FinCEN) regulations require insured nonmember banks and state chartered savings associations to report suspicious activities to FinCEN, a bureau of the U.S. Department of the Treasury.

§ 353.1 Purpose and scope. The purpose of this part is to ensure that an FDIC supervised institution files a Suspicious Activity Report when it detects a known or suspected criminal violation of federal law or a suspicious transaction related to a money laundering activity or a violation of the Bank Secrecy Act.

In the United States, financial institutions must file a SAR if they suspect that an employee or customer has engaged in insider trading activity. A SAR is also required if a financial institution detects evidence of computer hacking or of a consumer operating an unlicensed money services business.

However, if there is sufficient evidence linking you to a potential crime, such as money laundering, it may result in a formal investigation by law enforcement authorities. In some cases, filing a SAR may also result in your assets being frozen or seized by law enforcement agents.

A criminal offense involving dishonesty, breach of trust, or money laundering. Some examples include, but are not limited to, theft, misappropriation, embezzlement, forgery, false identification, false report to law enforcement, tax evasion, drug possession with intent to distribute, and writing of a bad check.

Section 18(a)(4) of the Federal Deposit Insurance Act (FDI Act), 12 U.S.C. 1828(a)(4) (Section 18(a)(4)), prohibits any person from engaging in false advertising by misusing the name or logo of the FDIC or from making knowing misrepresentations about the existence of or the extent or manner of deposit insurance.