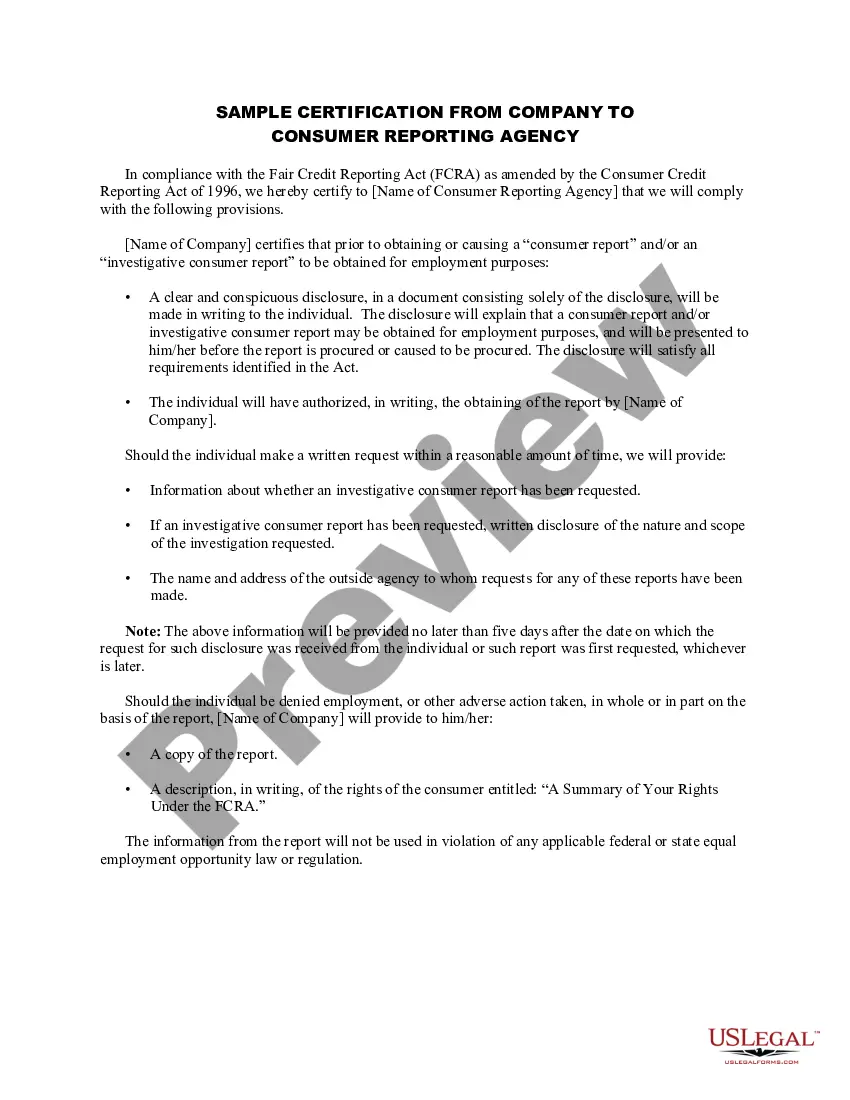

Rhode Island FCRA Certification Letter to Consumer Reporting Agency

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out FCRA Certification Letter To Consumer Reporting Agency?

You can spend time online looking for the valid document template that meets the federal and state requirements you need.

US Legal Forms offers a multitude of valid forms that have been reviewed by professionals.

You can easily download or print the Rhode Island FCRA Certification Letter to Consumer Reporting Agency from the service.

If available, utilize the Review option to look through the document template as well.

- If you already have a US Legal Forms account, you can Log In and click on the Download button.

- Then, you may complete, edit, print, or sign the Rhode Island FCRA Certification Letter to Consumer Reporting Agency.

- Every valid document template you obtain is yours indefinitely.

- To get another copy of any purchased form, go to the My documents section and click on the appropriate option.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for the jurisdiction/city of your choice.

- Review the form description to confirm you have chosen the correct form.

Form popularity

FAQ

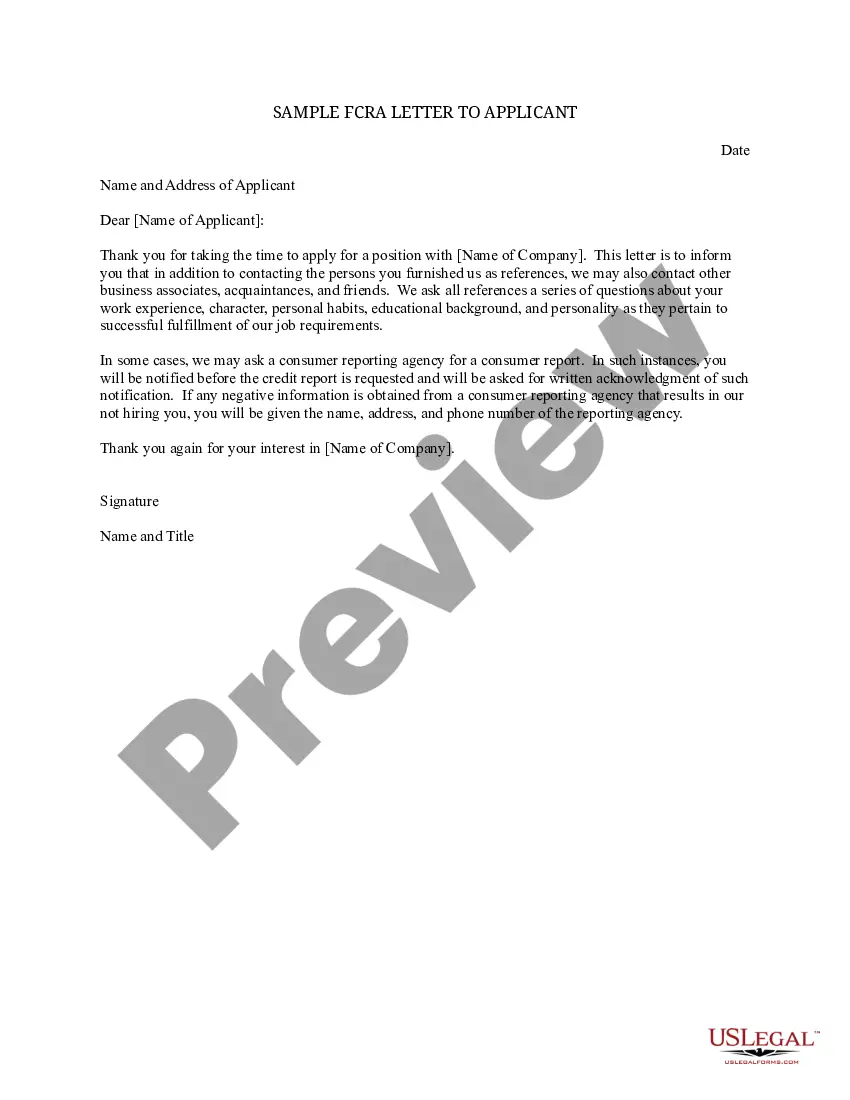

Four Basic Steps to FCRA ComplianceStep 1: Disclosure & Written Consent. Before requesting a consumer or investigative report, an employer must:Step 2: Certification To The Consumer Reporting Agency.Step 3: Provide Applicant With Pre-Adverse Action Documents.Step 4: Notify Applicant Of Adverse Action.

The FCRA requires agencies to remove most negative credit information after seven years and bankruptcies after seven to 10 years, depending on the kind of bankruptcy. Restrictions around who can access your reports.

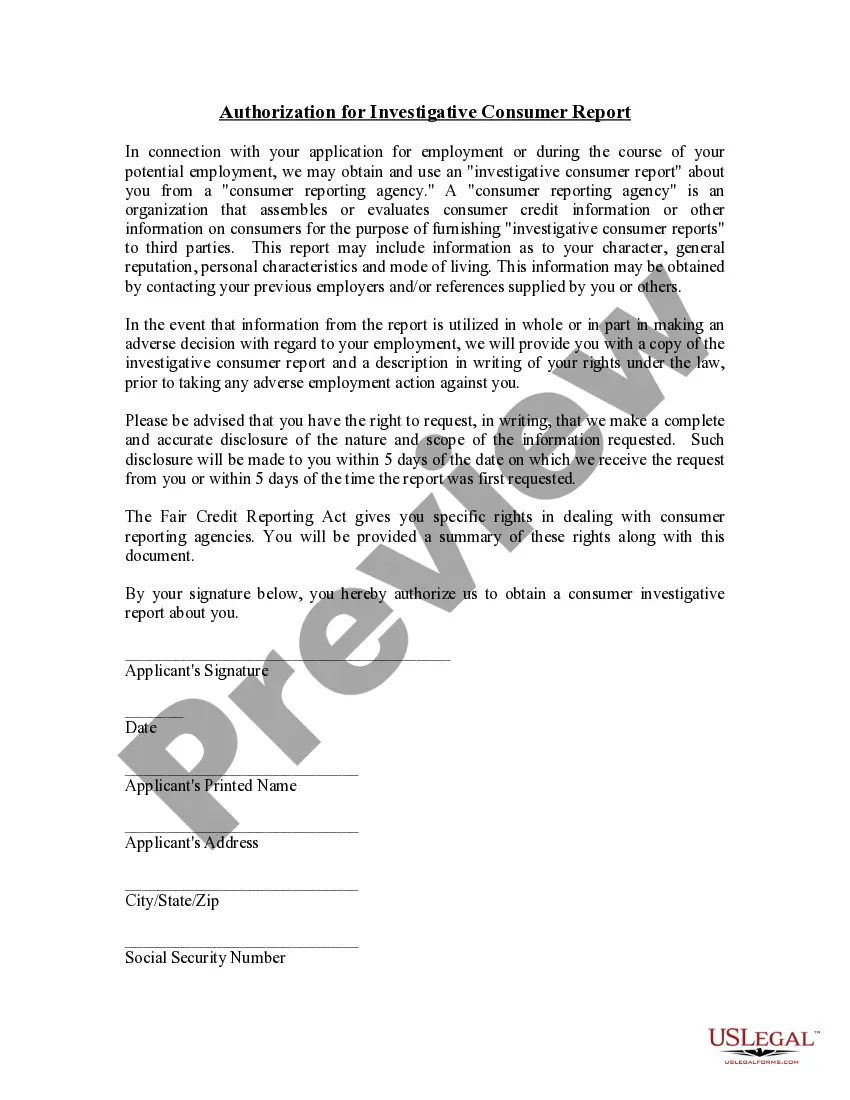

Specifically, the FCRA requires that you must provide a clear and conspicuous written notice that consists solely of the disclosure. In other words, the disclosure must be (1) clear and conspicuous; and (2) exist as a standalone document.

A statement indicating that the account "meets FCRA requirements" may be added if a consumer disputes information on their credit report, but the credit bureau determines that the information is accurate. Additionally, it can be concluded that all information is accurate and under federal regulations.

The FCRA requires any prospective user of a consumer report, for example, a lender, insurer, landlord, or employer, among others, to have a legally permissible purpose to obtain a report. Legally Permissible Purposes.

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

The FCRA Basic Certificate Program provides participants with a core understanding of foundational information core to the Fair Credit Reporting Act (FCRA). Staff at every level within an organization will benefit from this program.

Credit Report Adverse Action Letter A post-decision form sent by entities to consumers after deciding to deny/reject them due to their credit score and/or other information found in a consumer credit report.

Properly inform the applicant of adverse action: In your final adverse action letter, you must explain your choice and tell the applicant that they have the right to dispute your decision. Provide the necessary information for them to get another copy of their report.

A Summary of Your Rights Under the Fair Credit Reporting Act. The federal Fair Credit Reporting Act (FCRA) promotes the accuracy, fairness, and privacy of. information in the files of consumer reporting agencies.