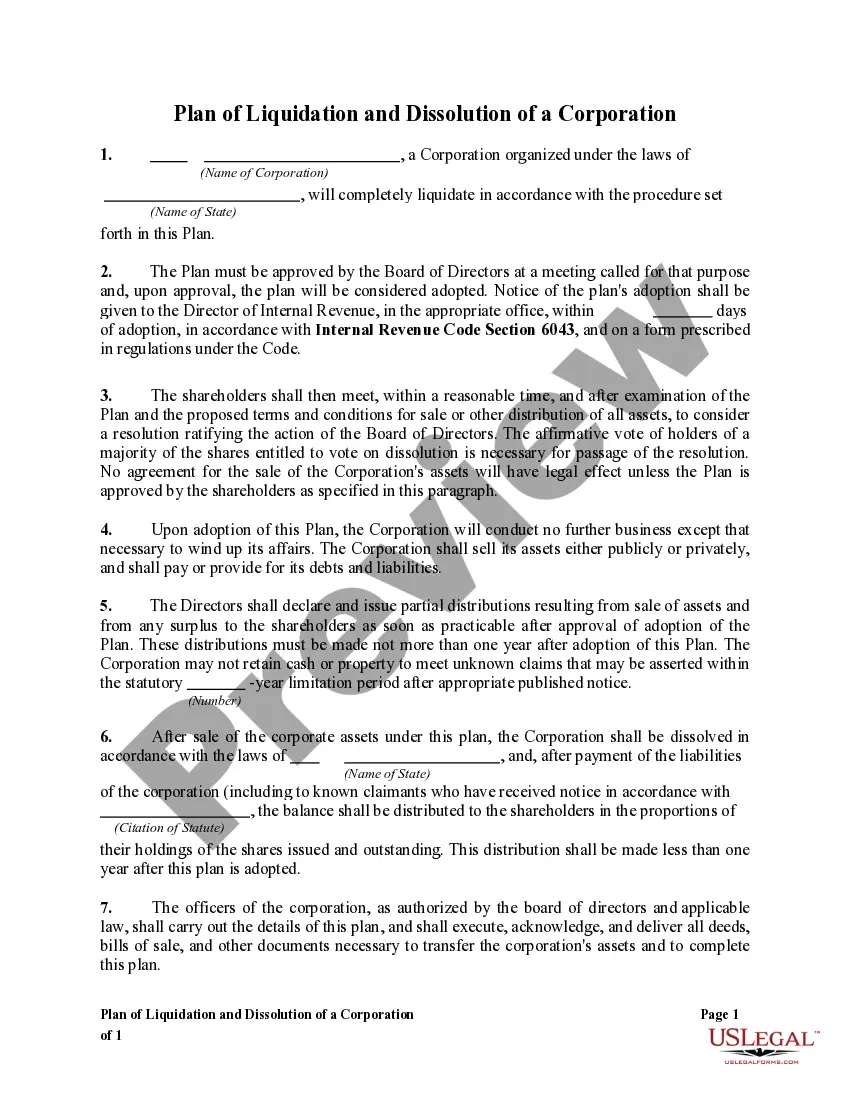

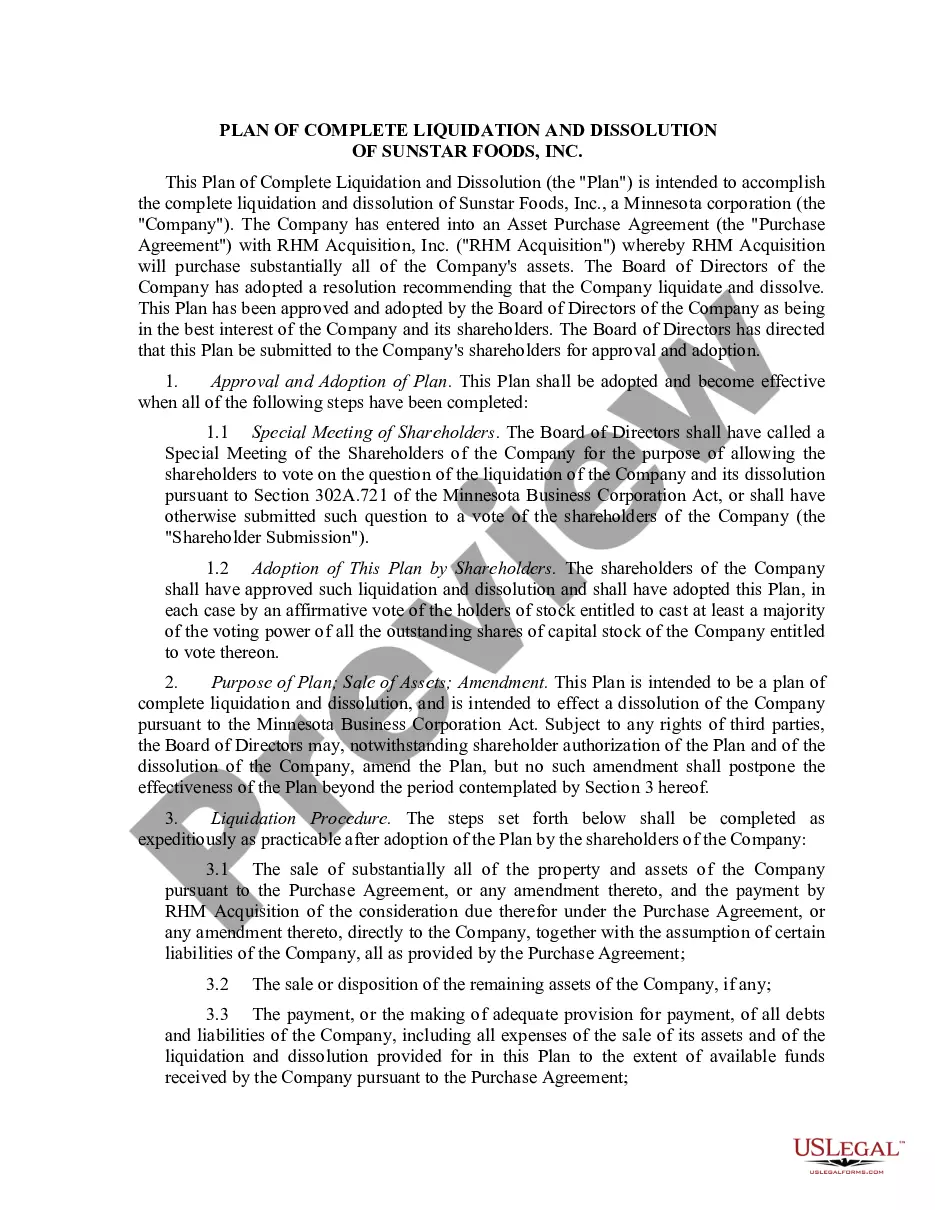

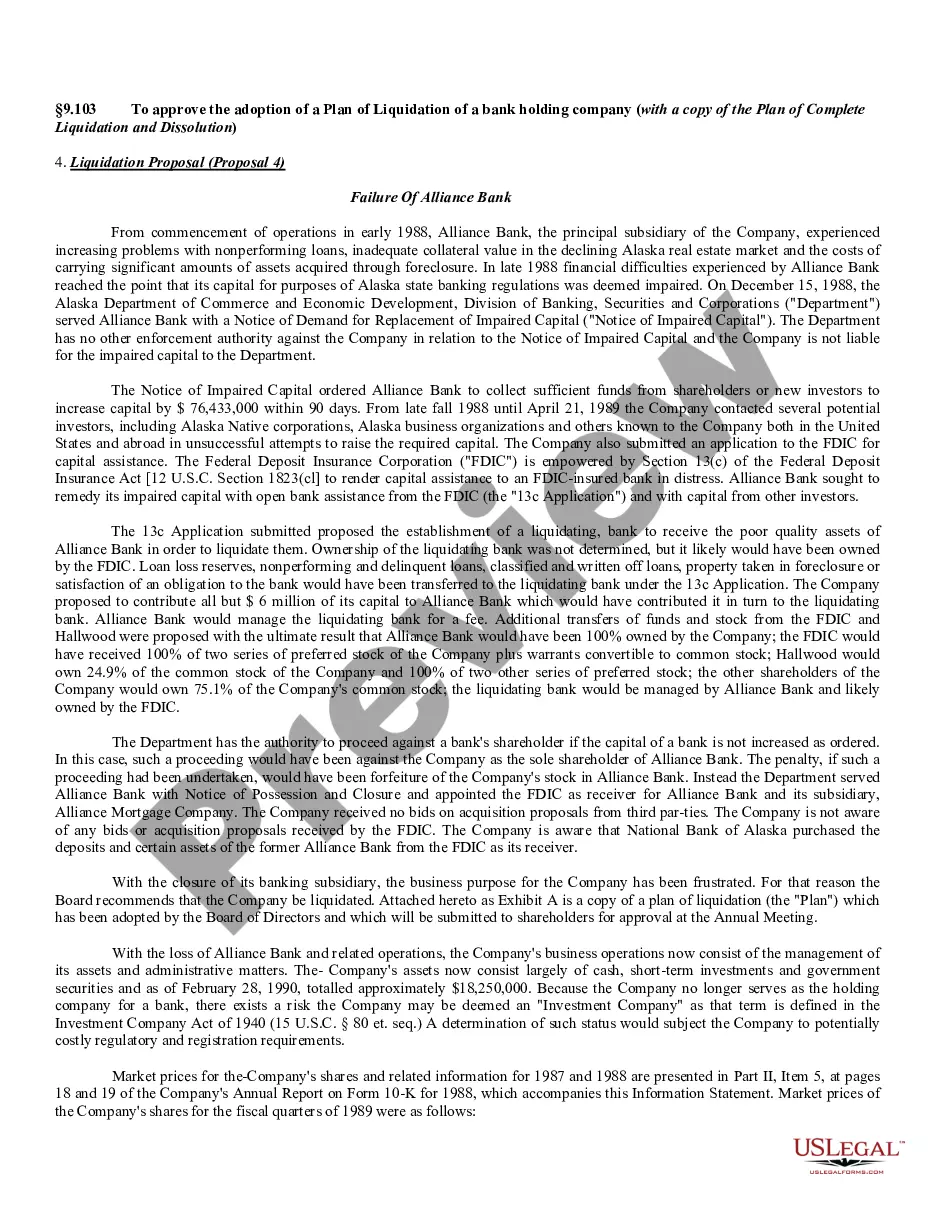

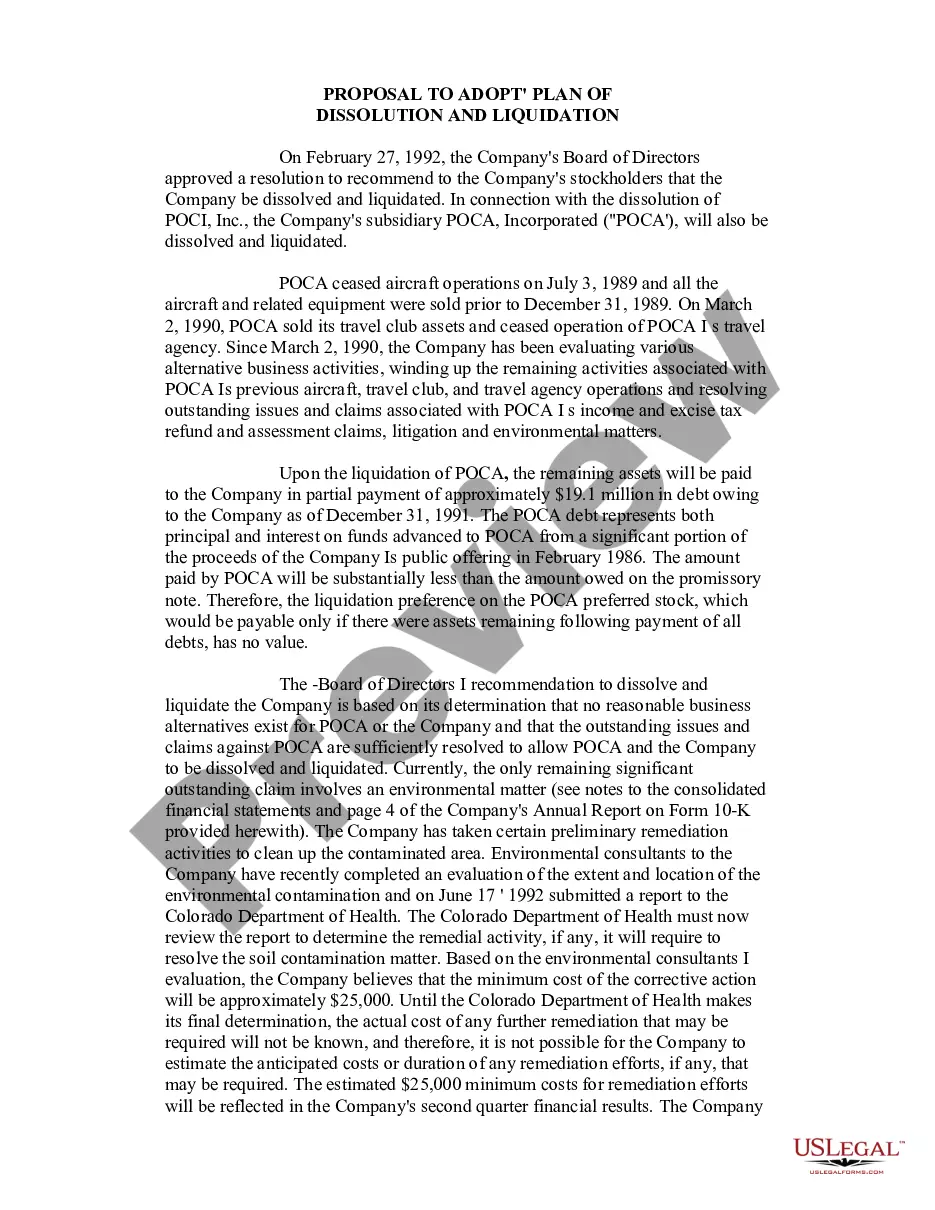

Puerto Rico Plan of complete liquidation and dissolution

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Plan Of Complete Liquidation And Dissolution?

Are you presently inside a position in which you need to have paperwork for either business or person uses nearly every day time? There are tons of legal file layouts accessible on the Internet, but getting ones you can trust is not simple. US Legal Forms delivers a huge number of kind layouts, much like the Puerto Rico Plan of complete liquidation and dissolution, that are published to fulfill federal and state specifications.

In case you are previously knowledgeable about US Legal Forms internet site and also have a free account, merely log in. After that, it is possible to acquire the Puerto Rico Plan of complete liquidation and dissolution format.

If you do not offer an accounts and want to begin to use US Legal Forms, adopt these measures:

- Find the kind you will need and ensure it is for the proper city/area.

- Use the Preview button to examine the form.

- Read the explanation to ensure that you have chosen the correct kind.

- If the kind is not what you`re searching for, use the Look for area to find the kind that meets your needs and specifications.

- If you get the proper kind, click on Buy now.

- Select the prices program you desire, fill out the required information and facts to make your bank account, and purchase your order utilizing your PayPal or bank card.

- Decide on a hassle-free paper structure and acquire your backup.

Locate each of the file layouts you may have bought in the My Forms food selection. You may get a more backup of Puerto Rico Plan of complete liquidation and dissolution any time, if necessary. Just click the necessary kind to acquire or produce the file format.

Use US Legal Forms, the most extensive selection of legal types, to save efforts and avoid faults. The services delivers appropriately made legal file layouts which can be used for an array of uses. Create a free account on US Legal Forms and begin generating your life easier.

Form popularity

FAQ

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.

To qualify as a tax-free subsidiary liquidation, the requirements under IRC §332(b) must be met. These requirements include ownership of at least 80% of the subsidiary's stock, complete cancellation or redemption of all of the subsidiary's stock, and completion of the liquidation with certain time limits.

IRC §331 provides rules for the tax treatment of shareholders receiving distributions in a complete liquidation of a corporation. In a complete liquidation, a corporation usually distributes all of its assets to the shareholders in exchange for all of its stock pursuant to a plan of a complete liquidation.

Section 332 creates an exception to the general rule of IRC §331(a), but this exception requires that the shareholder receiving the distribution be a corporation that owns at least 80% of the distributing corporation's stock. Partnership Taxation taxtaxtax.com ? corp ? study ? Study5 taxtaxtax.com ? corp ? study ? Study5

IRC §331 provides rules for the tax treatment of shareholders receiving distributions in a complete liquidation of a corporation. In a complete liquidation, a corporation usually distributes all of its assets to the shareholders in exchange for all of its stock pursuant to a plan of a complete liquidation. §331, Gain or Loss Treatment of Shareholders in Complete ... CCH Answer Connect ? irc ? explanation ? 3... CCH Answer Connect ? irc ? explanation ? 3...