Puerto Rico Petty Cash Journal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Petty Cash Journal?

If you want to acquire, download, or print sanctioned document templates, utilize US Legal Forms, the largest assortment of legal forms, accessible online.

Use the site's user-friendly and convenient search to find the documents you need.

Various templates for business and personal use are organized by categories and states, or keywords.

Step 4. Once you have found the form you need, click the Acquire now button. Choose the pricing plan you prefer and provide your credentials to register for an account.

Step 5. Complete the purchase. You may use your credit card or PayPal account to finalize the transaction.

- Utilize US Legal Forms to obtain the Puerto Rico Petty Cash Journal in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and select the Download option to access the Puerto Rico Petty Cash Journal.

- You can also access forms you previously downloaded from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Confirm you have selected the form for the appropriate area/region.

- Step 2. Utilize the Preview option to review the form's content. Do not forget to read the details.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find other variations of the legal form template.

Form popularity

FAQ

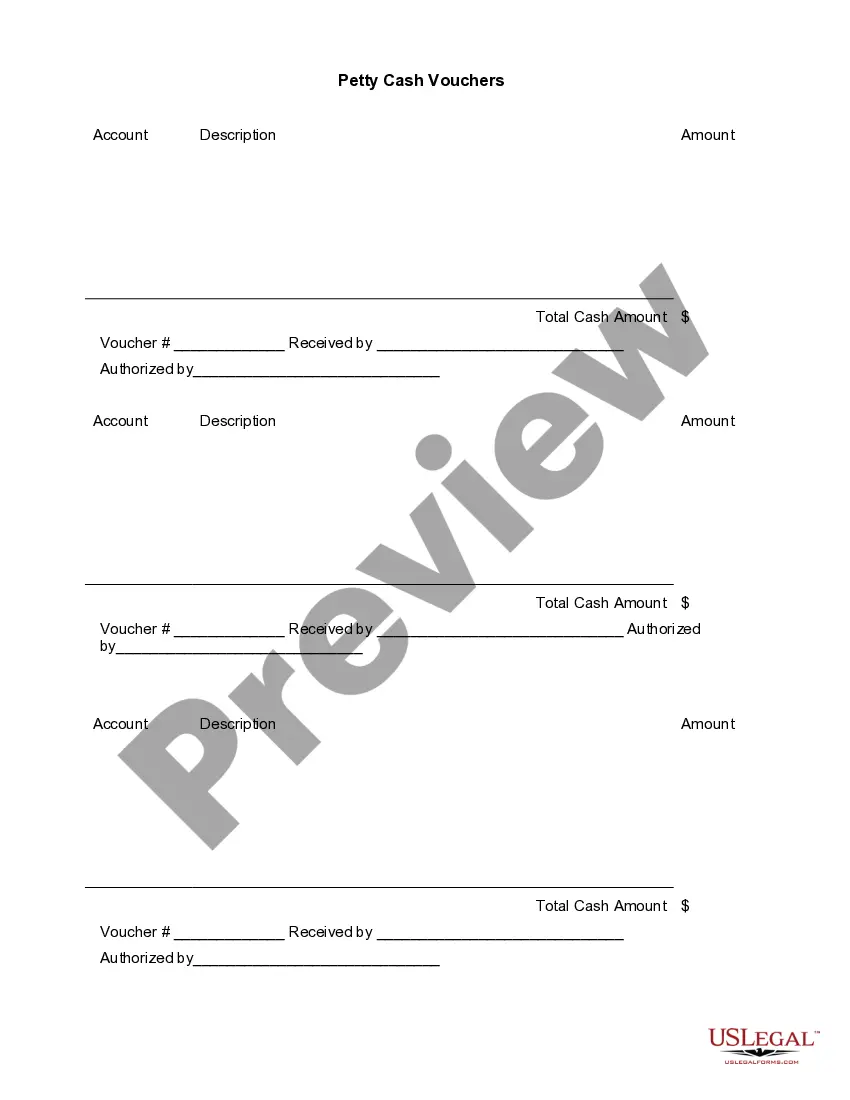

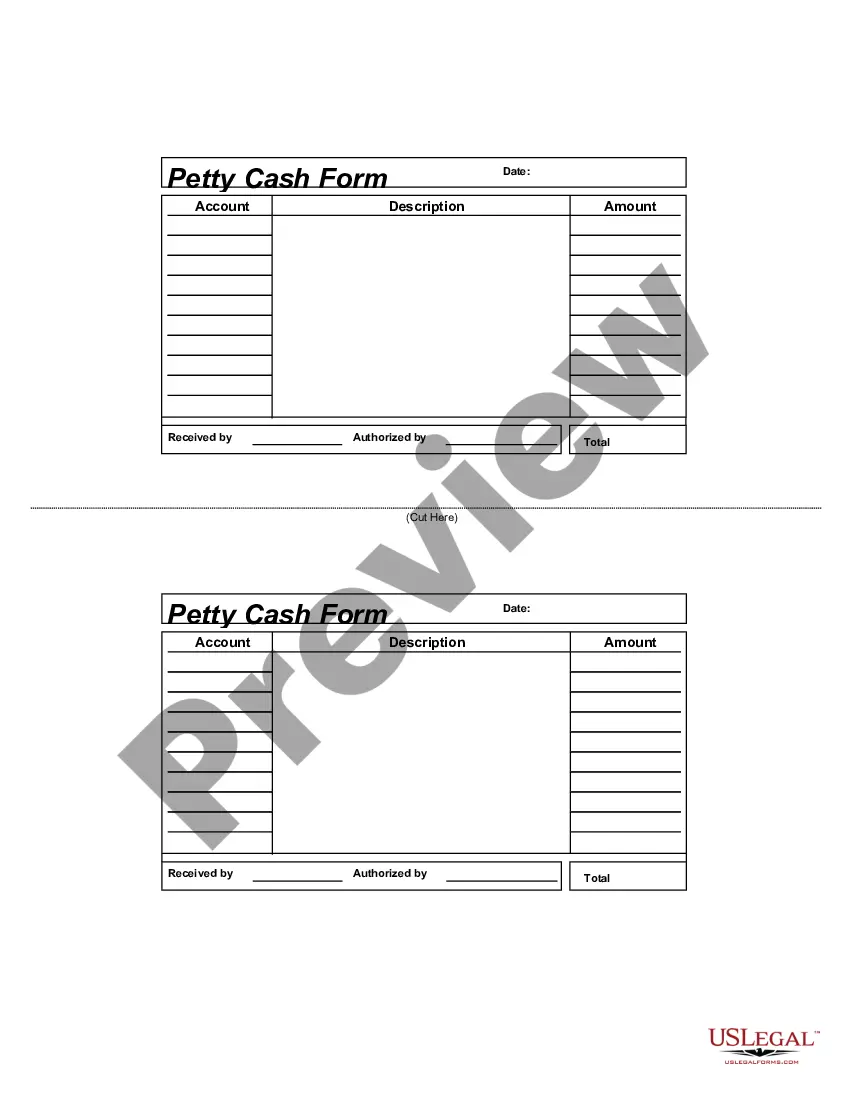

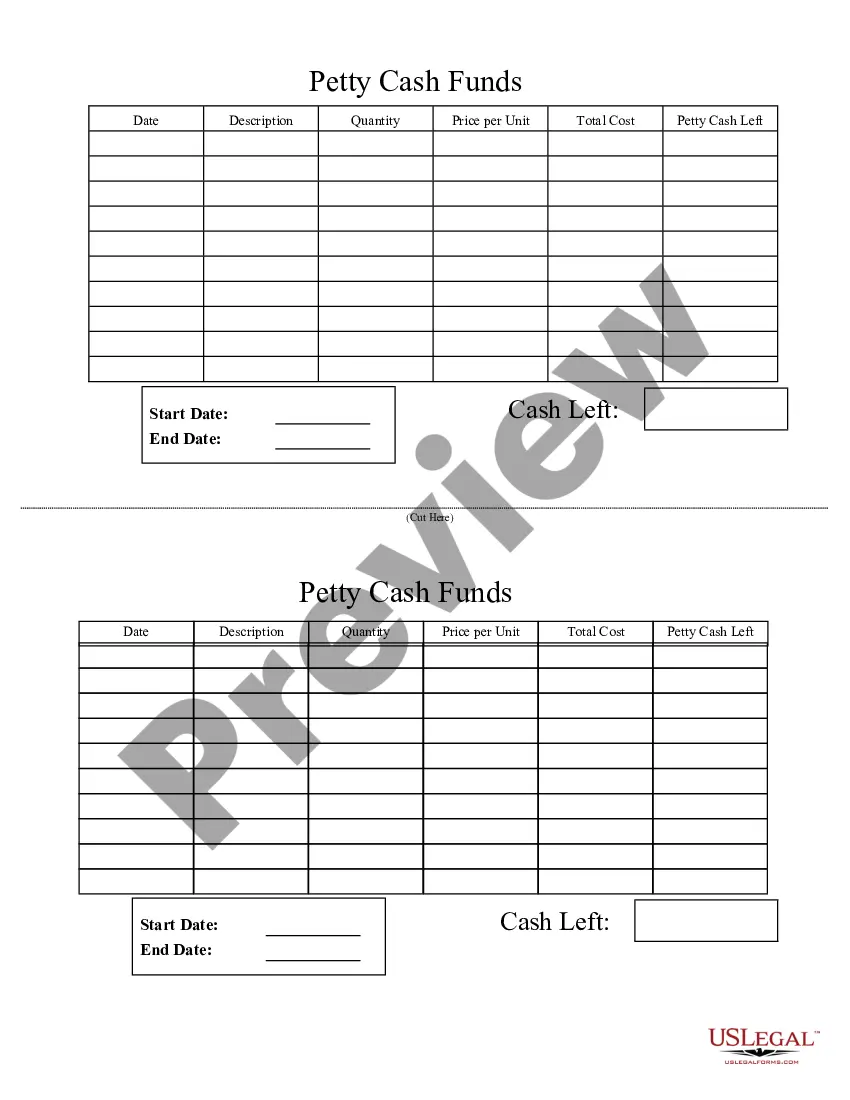

A simple petty cash book is just like the main cash book. Cash received by the petty cashier is recorded on the debit side, and all payments for petty expenses are recorded on the credit side in one column.

Petty cash funds may not be deposited into personal bank accounts or commingled with other funds.Departments may not establish bank accounts for petty cash funds.Purchases of goods and services for more than $100 should not be made with petty cash.Petty cash funds may not be expended for:

When a petty cash fund is in use, petty cash transactions are still recorded on financial statements. No accounting journal entries are made when purchases are made using petty cash, it's only when the custodian needs more cashand in exchange for the receipts, receives new fundsthat the journal entries are recorded.

Recording petty cash transactionsCreate new a bank account to represent your petty cash balance.Enter an opening balance to show the current balance of your petty cash.Record payments made from your petty cash.Record a transfer of money to top up the petty cash account.

Petty cash is a current asset and should be listed as a debit on the company balance sheet. To initially fund a petty cash account, the accountant should write a check made out to "Petty Cash" for the desired amount of cash to keep on hand and then cash the check at the company's bank.

The petty cash journal entry is a debit to the petty cash account and a credit to the cash account. The petty cash custodian refills the petty cash drawer or box, which should now contain the original amount of cash that was designated for the fund. The cashier creates a journal entry to record the petty cash receipts.

Petty cash appears within the current assets section of the balance sheet. This is because line items in the balance sheet are sorted in their order of liquidity. Since petty cash is highly liquid, it appears near the top of the balance sheet.

The journal entry that needs to be recorded is a debit (increase) to the petty cash fund and a credit (decrease) to the business checking account. Withdrawals made to the petty cash fund will be recorded as expenses.

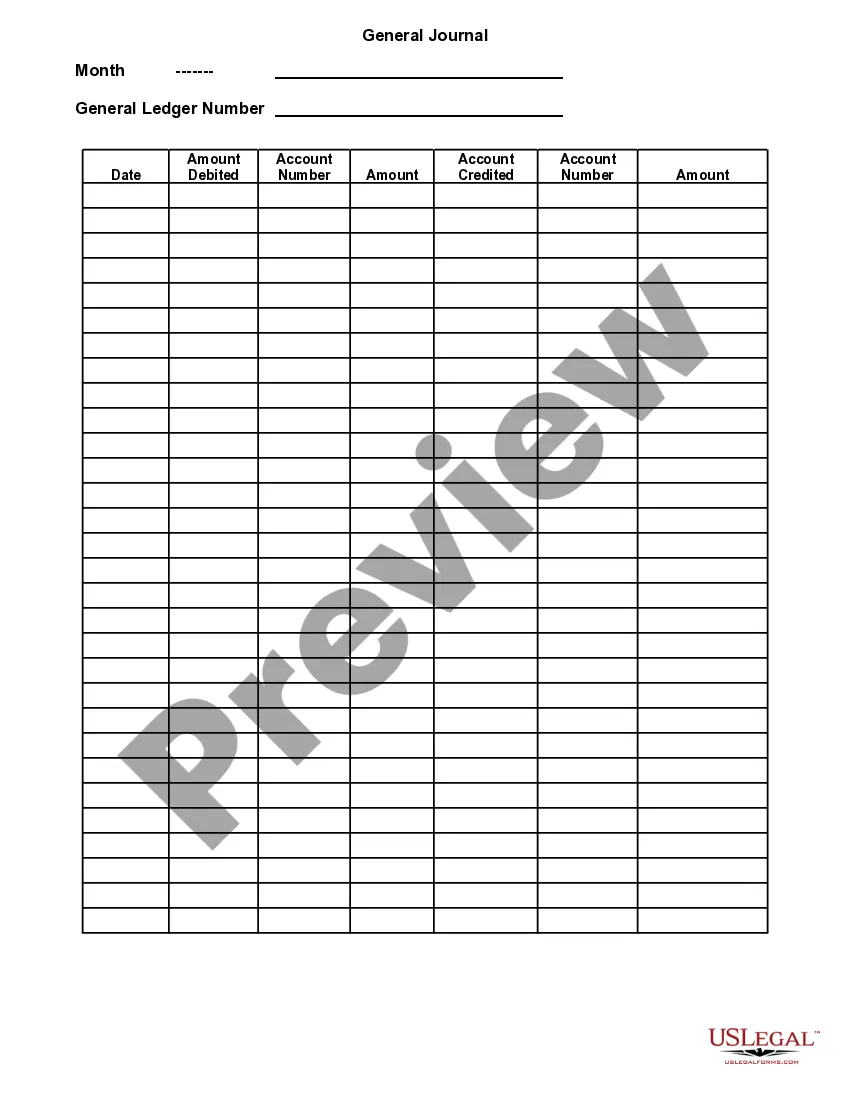

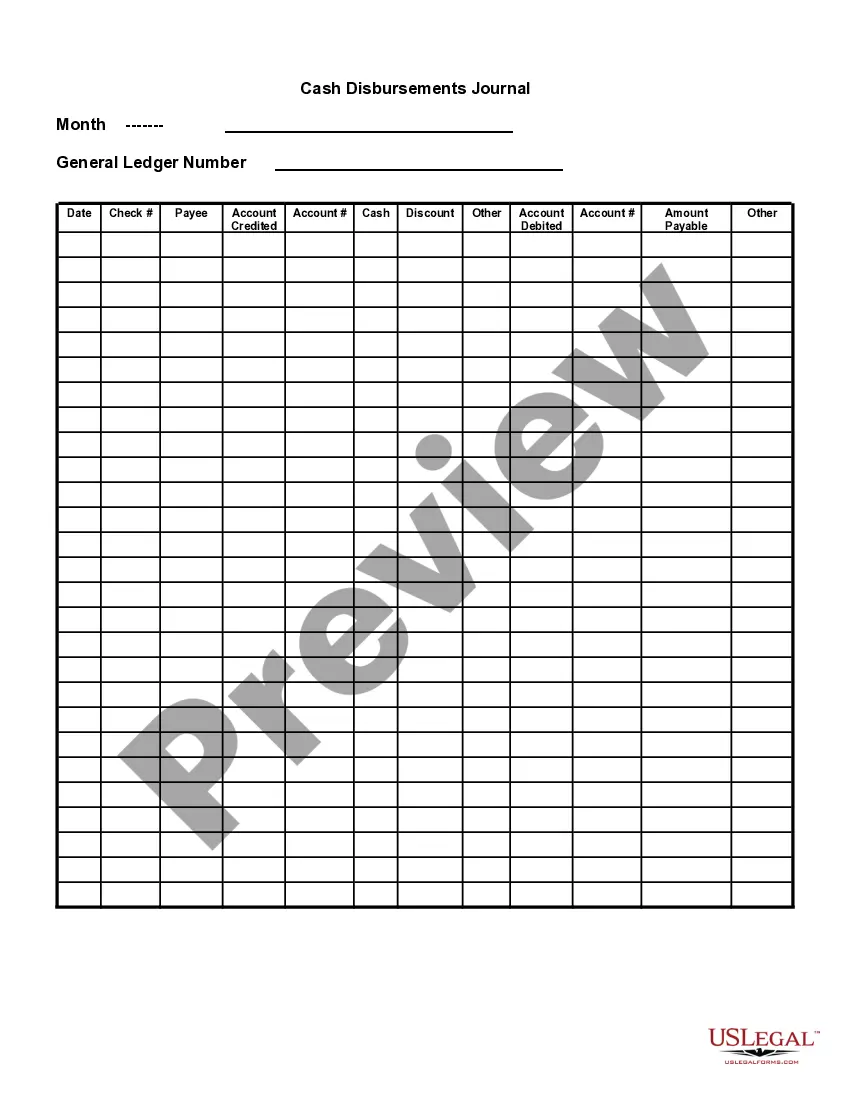

The petty cash journal contains a summarization of the payments from a petty cash fund. The totals in the journal are then used as the basis for a journal entry into a company's general ledger. This journal entry lists petty cash expenditures by expense type.

A petty cash account is an imprest account, so it is only debited when the fund is initially established or increased in amount. Transactions to replenish the account involve a debit to the expenses and a credit to the cash account (e.g., bank account).