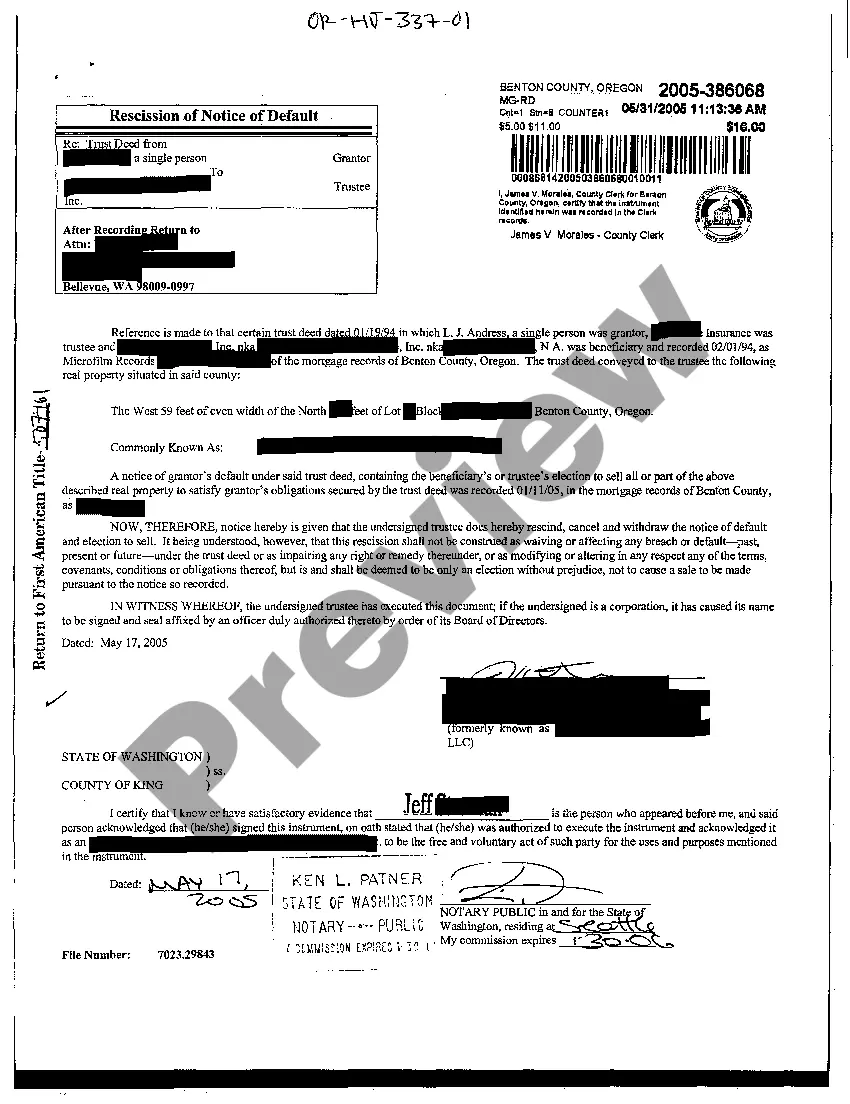

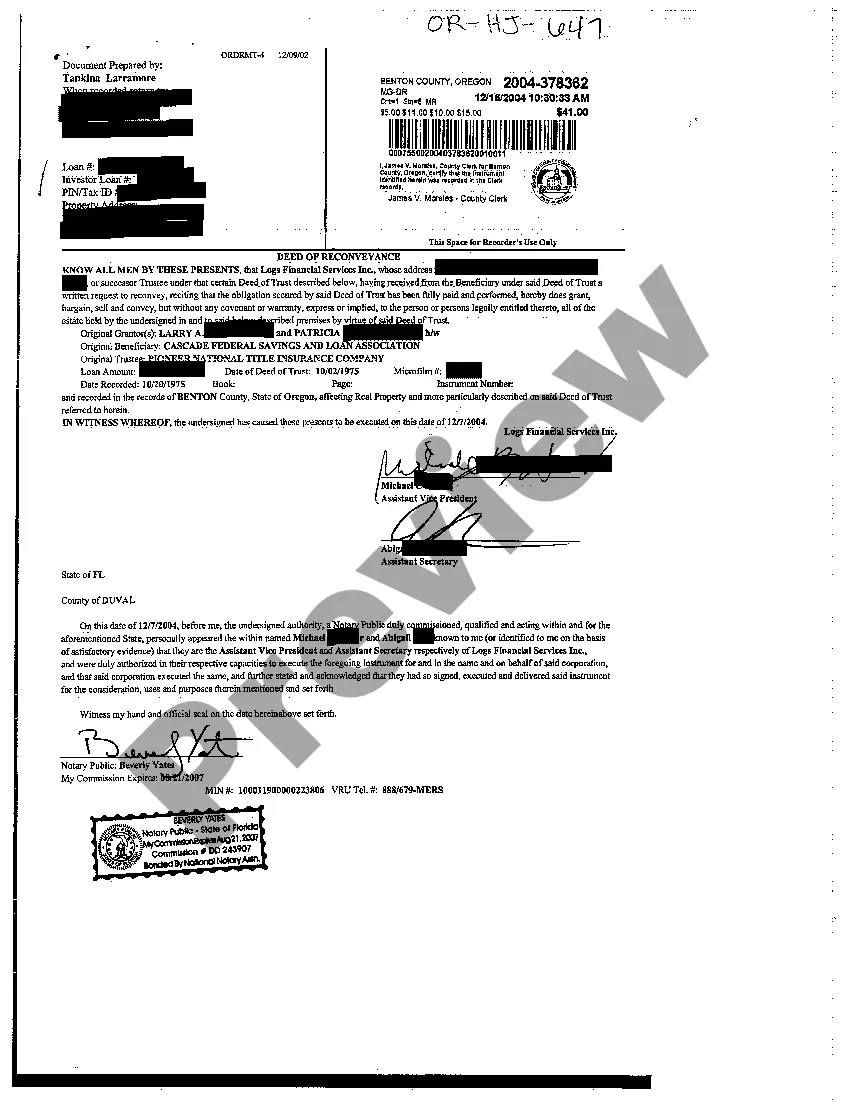

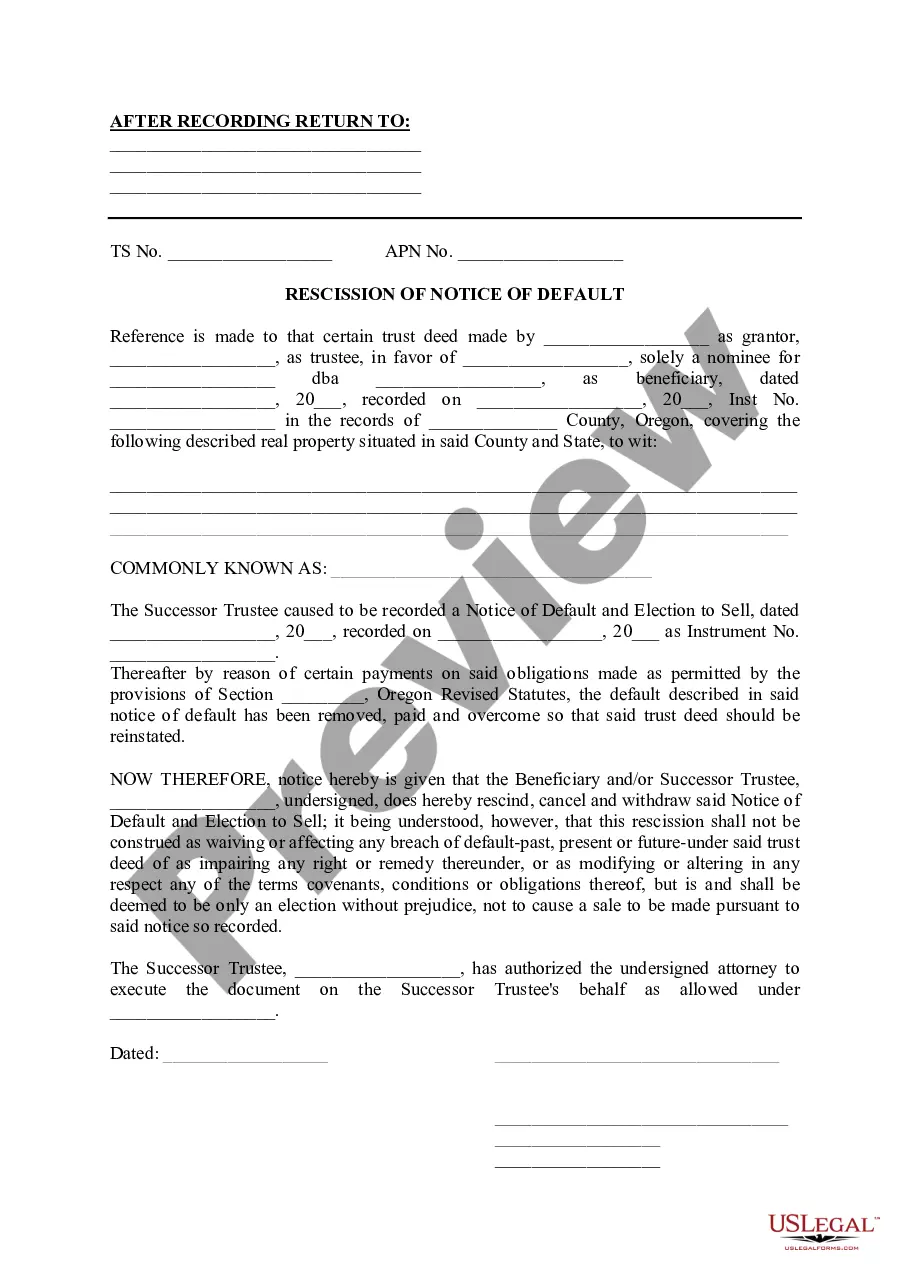

Oregon Rescission of Notice of Default

Description

How to fill out Oregon Rescission Of Notice Of Default?

Creating papers isn't the most uncomplicated process, especially for people who almost never work with legal papers. That's why we recommend using correct Oregon Rescission of Notice of Default samples made by skilled attorneys. It allows you to stay away from problems when in court or handling formal institutions. Find the samples you need on our website for top-quality forms and correct information.

If you’re a user having a US Legal Forms subscription, just log in your account. As soon as you’re in, the Download button will automatically appear on the file webpage. After accessing the sample, it will be stored in the My Forms menu.

Users without an activated subscription can easily get an account. Make use of this brief step-by-step help guide to get your Oregon Rescission of Notice of Default:

- Be sure that the form you found is eligible for use in the state it is required in.

- Confirm the document. Utilize the Preview option or read its description (if readily available).

- Click Buy Now if this file is what you need or use the Search field to get a different one.

- Select a suitable subscription and create your account.

- Utilize your PayPal or credit card to pay for the service.

- Download your document in a preferred format.

Right after doing these easy steps, you can fill out the form in a preferred editor. Check the completed information and consider asking a legal representative to examine your Oregon Rescission of Notice of Default for correctness. With US Legal Forms, everything gets much simpler. Test it now!

Form popularity

FAQ

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.

You can bring your loan current and stave off the foreclosure sale filing by paying the past due amount, plus penalties.You typically have to reinstate at least five days before the lender's deadline or risk the lender rejecting your payment and proceeding with a sale.

A notice of rescission is a form given with the intention of terminating a contract, provided that the contract entered into is a voidable one. It releases the parties from obligations set forth in the contract, effectively restoring them to the positions they were in before the contract existed.

The notice of default doesn't affect your credit file, but when the account defaults this will be recorded.If the debt is regulated by the Consumer Credit Act, you must be sent a default notice warning letter and have time to act on it before the default is recorded on your credit file.

Negotiate With Your Lender. If you are having financial difficulties, the worst thing that you can do is bury your head in the sand. Request a Forbearance. Modify Your Loan. Make a Claim. Get a Housing Counselor. Declare Bankruptcy. Use A Foreclosure Defense Strategy. Make Them Produce The Not.

After the lender files the Notice of Default, you get 90 days to bring your past-due bill current. After the 90 days pass, the lender files a Notice of Sale with the clerk. The Notice of Sale displays the location, date and time of the sale. It lists the trustee's name and contact information.

A few potential ways to stop a foreclosure include reinstating the loan, redeeming the property before the sale, or filing for bankruptcy. (Of course, if you're able to work out a loss mitigation option, like a loan modification, that will also stop a foreclosure.)

File for Bankruptcy Protection to Avoid ForeclosureIf your foreclosure sale is scheduled to take place in a matter of days, you can stop the foreclosure in its tracks by filing for bankruptcy. Upon your filing, something called an automatic stay goes into place.