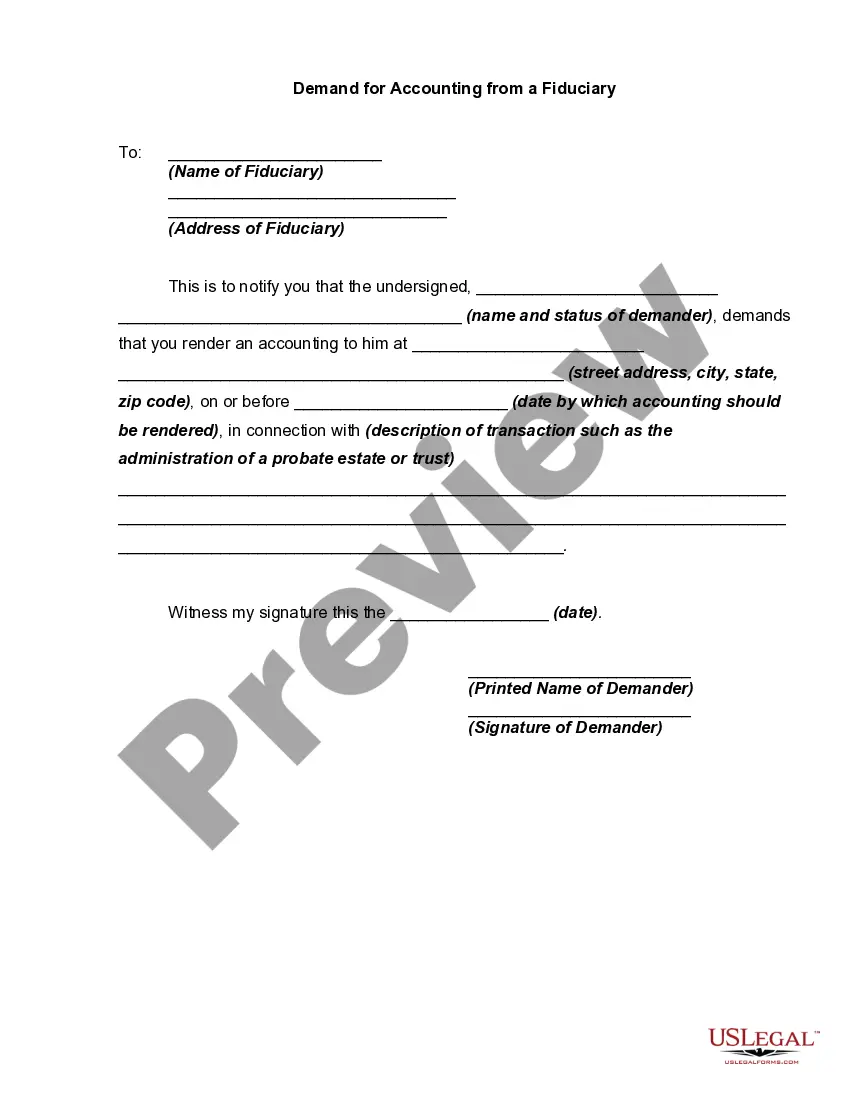

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

New York Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary Such As An Executor, Conservator, Trustee Or Legal Guardian?

Are you in a situation where you need documents for potential business or specific reasons nearly every day.

There is a wide range of legal document templates accessible online, but locating ones you can rely on is not easy.

US Legal Forms offers thousands of document templates, including the New York Demand for Accounting from a Fiduciary like an Executor, Conservator, Trustee, or Legal Guardian, which are designed to comply with state and federal requirements.

Select the pricing plan you wish, fill out the required information to create your account, and complete the purchase using your PayPal or credit card.

Choose a convenient file format and download your copy. Explore all the document templates you have purchased in the My documents section. You can obtain another copy of the New York Demand for Accounting from a Fiduciary whenever necessary; just select the desired document to download or print it.

Utilize US Legal Forms, the most extensive repository of legal forms, to save time and prevent errors. The service provides professionally crafted legal document templates suitable for various purposes. Create an account on US Legal Forms and start making your life simpler.

- If you are already familiar with the US Legal Forms site and possess an account, simply Log In.

- After that, you can download the New York Demand for Accounting from a Fiduciary like an Executor, Conservator, Trustee, or Legal Guardian template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the document you need and ensure it is for the correct city/state.

- Use the Preview button to review the form.

- Check the description to make sure you have selected the right document.

- If the document is not what you are searching for, use the Search field to find the form that meets your needs and requirements.

- Once you find the appropriate document, click Buy now.

Form popularity

FAQ

To hold a trustee accountable, beneficiaries can start by requesting a clear accounting of the trust's activities. If the trustee fails to respond satisfactorily, they can file a New York Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian. Engaging legal assistance can also provide guidance throughout this process to ensure proper adherence to trust laws. Ultimately, knowing your rights and actively participating can empower you to secure the transparency you deserve.

A petition to compel accounting is a formal request made to the court to require a fiduciary, like a trustee, to provide a detailed accounting of their financial management. This is often necessary when beneficiaries feel neglected or overlooked in the decision-making process. In cases where a New York Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian is ignored, this petition serves as a vital tool for accountability. It helps safeguard the financial health of the trust and ensure beneficiaries receive their rightful due.

If a trustee does not provide accounting, it raises concerns about the management of the trust. Beneficiaries have the right to request a New York Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian. This request ensures transparency and may lead to court intervention if needed. Ultimately, accountability is crucial to maintaining trust and protecting beneficiaries' interests.

To ask for an accounting of a trust, you should directly communicate with the trustee, preferably through a written request. Be clear about your rights as a beneficiary and reference any legal obligations the trustee has regarding disclosure. If you encounter resistance, you can escalate your request via a New York demand for accounting from a fiduciary. This process allows you to formally obtain the financial information you are entitled to receive.

To demand an accounting, begin by drafting a clear and professional letter outlining your request to the fiduciary involved. Make sure to include specific details about the accounting you seek, referencing relevant laws that support your request. If the fiduciary does not respond, you may take further steps to initiate a New York demand for accounting from a fiduciary. This will legally compel them to provide necessary financial disclosures.

If a trustee is reluctant to provide an accounting, the first step is to issue a formal written request for this information. Should this approach be ineffective, you can consider legal action by filing a New York demand for accounting from a fiduciary. This process helps to enforce your rights as a beneficiary and mandates the trustee to disclose financial information regarding the trust or estate.

Yes, a beneficiary of a trust has the right to demand an accounting from the trustee. This legal right allows beneficiaries to understand how the trust assets are being managed and whether they are being distributed appropriately. If the trustee is unwilling to cooperate, you may need to initiate a New York demand for accounting from a fiduciary. This formal request can compel the trustee to provide the necessary financial details.

Requesting an accounting of an estate can be done by contacting the executor directly and asking for a detailed account of the estate's finances. If the executor does not provide this accounting voluntarily, you may need to escalate your request by filing a New York demand for accounting from a fiduciary. This legal avenue ensures that your rights as a beneficiary are protected, and that you receive the transparent information you deserve.

To demand an accounting of a trust, you should send a written request to the trustee detailing your request. Clearly state that you are invoking your rights under the relevant laws governing the trust, which often allows beneficiaries to receive financial disclosures. If the trustee does not respond or comply, consider pursuing a New York demand for accounting from a fiduciary. This formal process can help you obtain the required financial records.

In New York, an executor is obligated to provide an accounting to the beneficiaries of an estate. This transparency helps beneficiaries understand how the deceased's assets are being managed and distributed. If you have concerns about the executor's actions, you may consider filing a New York demand for accounting from a fiduciary. This ensures you receive the necessary information regarding the estate's financial activities.