New York Mortgage Payoff Affidavit

What is this form?

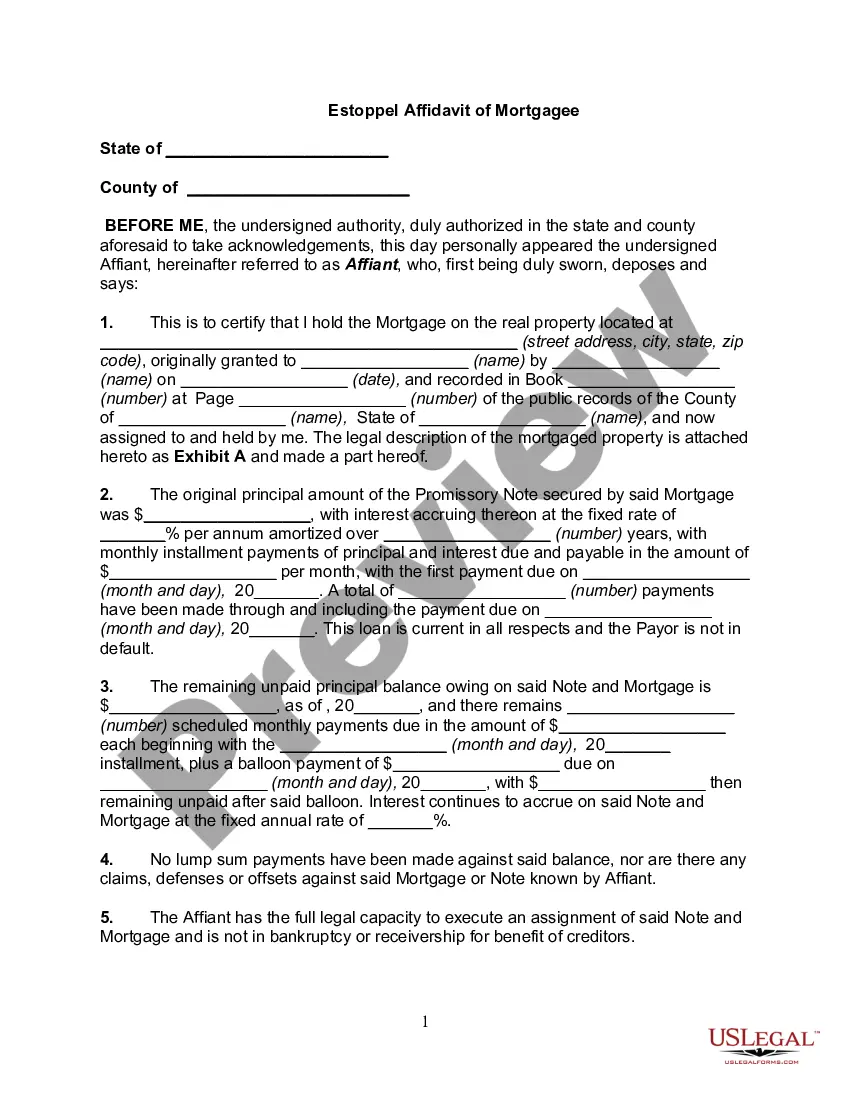

A Mortgage Payoff Affidavit is a legal document that affirms the existence of a payoff statement for a mortgage loan. This affidavit is sworn before a notary public and includes information regarding the mortgage balance and payout requirements to satisfy the loan. It ensures that the title insurance company is aware of the existing mortgage and any associated risks in omitting it from the title insurance policy. This form differs from other real estate documents as it specifically addresses mortgage payoff and title insurance considerations.

What’s included in this form

- Affiant information: Personal details about the individual swearing the affidavit.

- Property details: Identification of the property associated with the mortgage.

- Payoff letter: A statement confirming the balance and interest details necessary to settle the mortgage.

- Indemnity clause: Agreement to protect the title insurance company from any claims related to the mortgage payoff.

- Forwarding address: Contact information for future correspondence.

When this form is needed

This form should be used when you are seeking to confirm the payoff of a mortgage loan before closing a real estate transaction. It is commonly needed when the seller is discharging a mortgage and the title insurance company requires assurance that there are no outstanding claims related to the mortgage after the transaction is complete. Using this affidavit helps clear title issues and ensures smooth property transfer.

Intended users of this form

- Homeowners who are paying off their mortgage and need to confirm the payoff terms.

- Real estate agents involved in property sales where a mortgage is being settled.

- Title insurance companies seeking indemnification against potential claims related to existing mortgages.

- Buyers purchasing a property that still has an active mortgage requiring proper clearance.

Instructions for completing this form

- Fill in the title number and state for the mortgage.

- Provide the name and address of the party executing the affidavit.

- Detail the property that secures the mortgage.

- Include the date of the payoff letter and the mortgage holder's details.

- Sign and date the form in front of a notary public.

Is notarization required?

Yes, this form must be notarized to be legally valid. The affidavit requires affirmation of its contents before a notary public to ensure it meets legal requirements. US Legal Forms offers integrated online notarization, providing secure video calls and legal equivalence without the need to travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Not including the correct property address may lead to confusion.

- Failing to sign the affidavit in front of a notary public renders it invalid.

- Omitting important details from the payoff letter might affect title clearance.

- Not providing a current forwarding address can complicate future communications.

Why complete this form online

- Immediate access to a reliable legal template created by licensed attorneys.

- Easy customization to fit your specific circumstances and details.

- Downloadable and printable for convenience at any time.

- Eliminates the need for multiple in-person visits to obtain legal forms.

Looking for another form?

Form popularity

FAQ

A homeowner that wants to get rid of a current loan in favor of a new loan may also look forward to replacing a present mortgage debt. Both scenarios require the homeowner to pay off existing mortgage indebtedness. Homeowners must formally "request payoff" from their lenders for the exact amount owed.

How long does it take to get a mortgage payoff statement? Generally speaking, you should receive your mortgage payoff statement within seven business days of your request.

A payoff statement for a mortgage, sometimes referred to as a payoff letter, is a document that details the exact amount of money needed to fully pay off your mortgage loan. The payoff amount isn't just your outstanding balance; it also encompasses any interest you owe and potential fees your lender might charge.

They're often used in refinancing, consolidation loans, debts in collections, and other situations wherein a lender wants to know how much must be paid to satisfy a loan. If you have debt and you want a payoff statement, you can request one by contacting whichever lender or creditor holds the debt.

A payoff statement is a document you must request from your current loan servicer which lets us know the funds required to close out your loan(s) at a future date, which includes all interest accrued between today and that future date. It takes your daily interest into account, unlike your regular monthly statement.