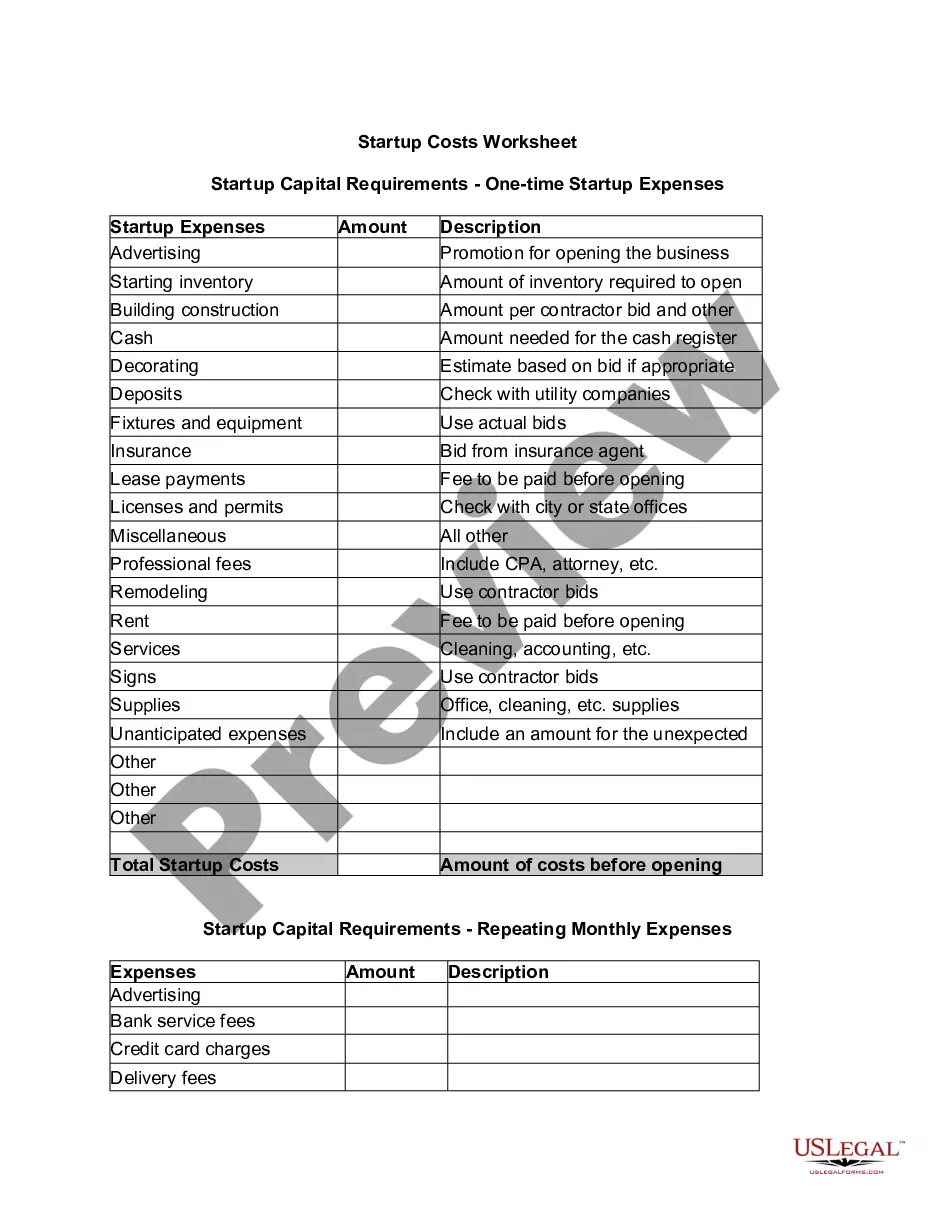

Nevada Startup Costs Worksheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Startup Costs Worksheet?

Are you currently in a situation where you require documents for either professional or personal reasons nearly every day.

There are numerous legal document templates accessible online, but locating ones you can trust is not simple.

US Legal Forms provides thousands of form templates, including the Nevada Startup Costs Worksheet, designed to comply with state and federal regulations.

Utilize US Legal Forms, one of the most extensive collections of legal forms, to save time and avoid mistakes.

The service provides professionally crafted legal document templates that you can use for a variety of purposes. Create an account on US Legal Forms and begin making your life a bit easier.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- After that, you can download the Nevada Startup Costs Worksheet template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/state.

- Use the Preview option to examine the form.

- Review the description to confirm that you have selected the right form.

- If the form is not what you are looking for, use the Lookup section to find the form that meets your needs and requirements.

- When you obtain the correct form, click Buy now.

- Select the pricing plan you want, fill in the necessary information to create your account, and pay for the order using your PayPal or Visa or Mastercard.

- Choose a suitable file format and download your copy.

- Find all of the document templates you have purchased in the My documents section. You can download another copy of the Nevada Startup Costs Worksheet at any time, if needed. Just click the form to download or print the document template.

Form popularity

FAQ

Startup costs do not include costs for interest, taxes, and research and experimentation (Sec. 195(c)(1)).

Nonqualifying costs Start-up costs don't include deductible interest, taxes, or research and experimental costs.

Startup costs will include equipment, incorporation fees, insurance, taxes, and payroll. Although startup costs will vary by your business type and industry an expense for one company may not apply to another.

Start-up costs can be capitalized and amortized if they meet both of the following tests: You could deduct the costs if you paid or incurred them to operate an existing active trade or business (in the same field), and; You pay or incur the costs before the day your active trade or business begins.

Key Takeaways. Startup costs are the expenses incurred during the process of creating a new business. Pre-opening startup costs include a business plan, research expenses, borrowing costs, and expenses for technology. Post-opening startup costs include advertising, promotion, and employee expenses.

How to calculate startup costsIdentify your expenses. Start by writing down the startup costs you've already incurred but don't stop there.Estimate your costs. Once you've developed a list of your business needs, note the average cost for each category.Do the math.Add a cushion.Put the numbers to work.

Start-up costs are amounts the business paid or incurred for creating an active trade or business, or investigating the creation or acquisition of an active trade or business.

Startup costs do not include costs for interest, taxes, and research and experimentation (Sec. 195(c)(1)).

Startup costs are the expenses incurred during the process of creating a new business. Pre-opening startup costs include a business plan, research expenses, borrowing costs, and expenses for technology. Post-opening startup costs include advertising, promotion, and employee expenses.

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.