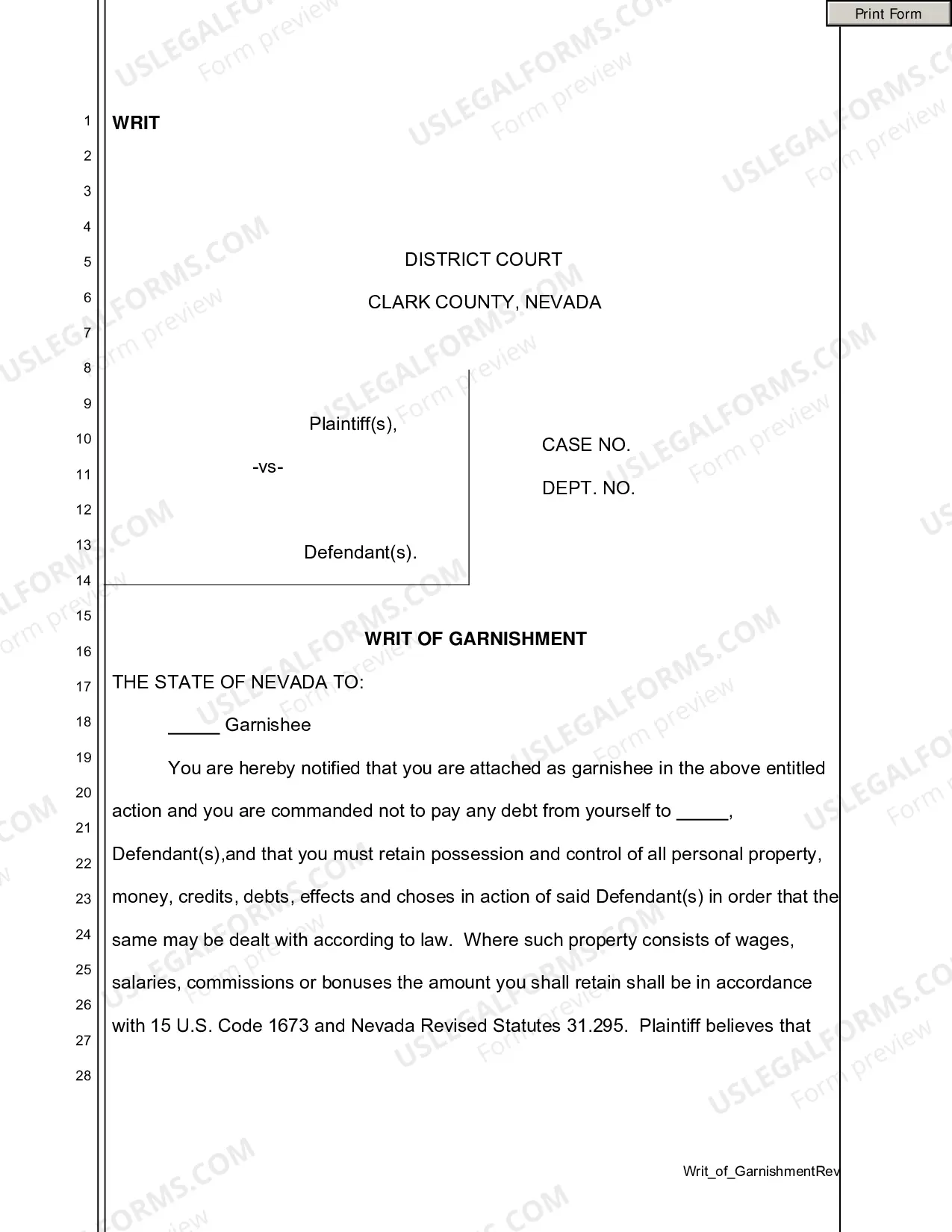

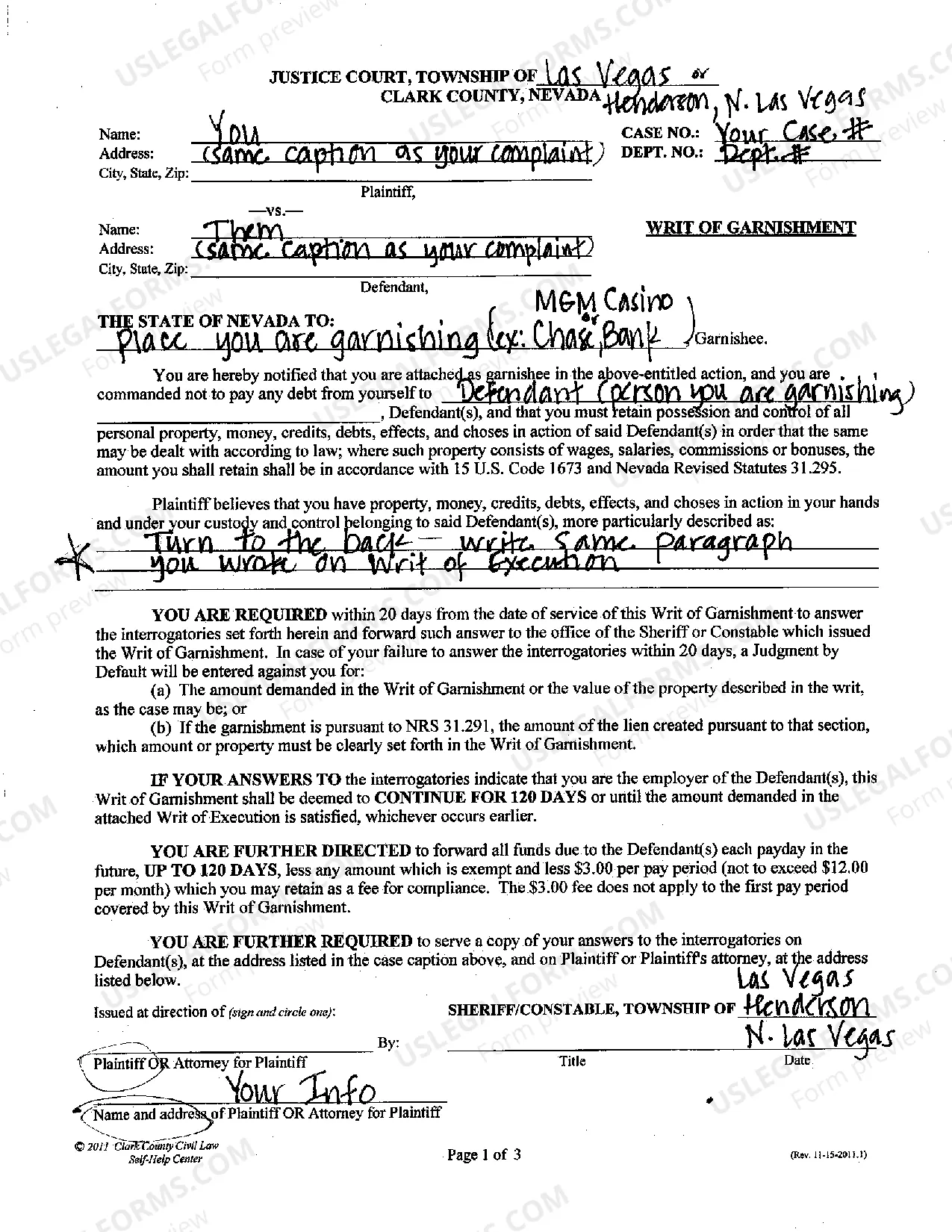

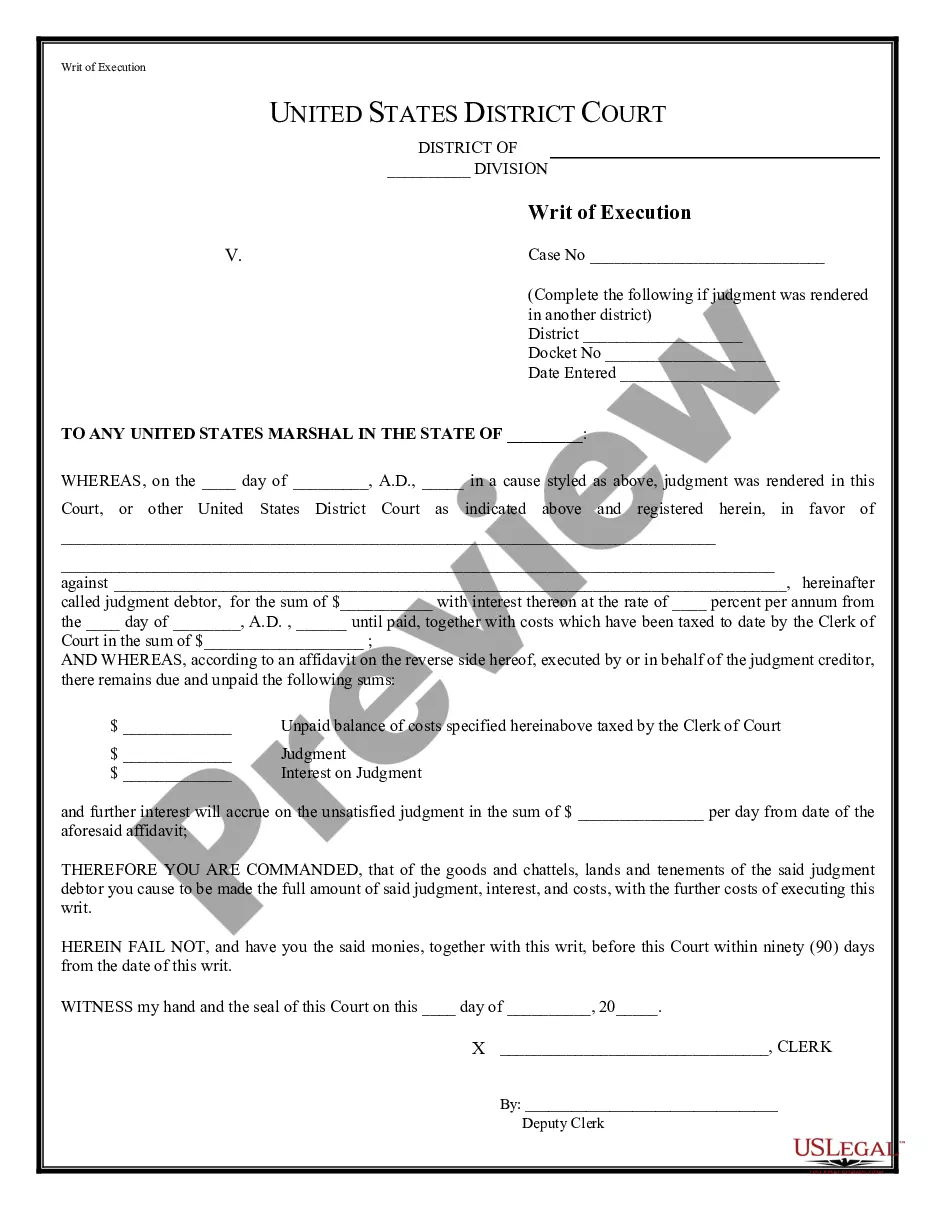

Nevada Writ of Garnishment

About this form

A Writ of Garnishment is a legal document used to collect a debt by directing a third party, typically an employer or financial institution, to withhold money belonging to a debtor. This form is utilized in Nevadaâs small claims court to ensure that the creditor can legally claim funds owed by the debtor from their accounts or wages. Unlike other debt recovery methods, the Writ of Garnishment allows creditors to take direct action against a debtor's property in a very specific legal manner.

Key components of this form

- County information where the action is filed

- Identities of the plaintiff and defendant, including the case number

- Name of the garnishee (employer or bank) from whom the funds are sought

- Details about the property or money owed to the defendant

- Instructions for the garnishee, including timelines for response

When this form is needed

This form should be used when a creditor has obtained a judgment against a debtor and seeks to recover funds directly from that debtor's wages or bank accounts. Common scenarios include situations where a debtor fails to pay debts, defaults on loans, or when court orders for payment are not being met.

Who can use this document

- Creditors who have received a judgment in their favor against a debtor

- Individuals or businesses seeking legal means to recover owed amounts

- Attorneys representing clients in debt collection cases

- Any party looking to legally enforce a court order for debt repayment

Completing this form step by step

- Identify the county at the top of the form.

- Fill in the names of the plaintiff and defendant, along with the case number.

- Clearly specify the name of the garnishee, such as an employer or bank.

- Provide a detailed description of the property or funds owed to the defendant.

- Ensure all information is typed, as handwritten forms may not be accepted.

- Check for any additional requirements from the local court before submitting the form.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It is important to consult local regulations to ensure compliance with any additional requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to fill out the form completely or accurately.

- Not submitting the required copies of the form along with the original.

- Overlooking any state-specific instructions for filing.

- Incorrectly identifying the garnishee or failing to provide adequate details.

Why complete this form online

- Convenience of downloading and filling out the form at your own pace.

- Editable formats allow customization to fit individual circumstances.

- Access to legal form templates drafted by licensed attorneys ensures compliance with legal standards.

- Time-saving process without the need for in-person visits to legal offices.

Legal use & context

- A Writ of Garnishment is enforceable in accordance with Nevada law and federal regulations.

- Garnishee must comply with the writ or face potential legal penalties.

- This form is part of a broader collection process that includes obtaining a judgment prior to garnishment.

Summary of main points

- A Writ of Garnishment is a legal tool for creditors to collect debts.

- Used primarily when previous attempts to collect have failed.

- Must be accurately completed and submitted as per local court rules.

- Check for any specific Nevada regulations that may apply to your situation.

Looking for another form?

Form popularity

FAQ

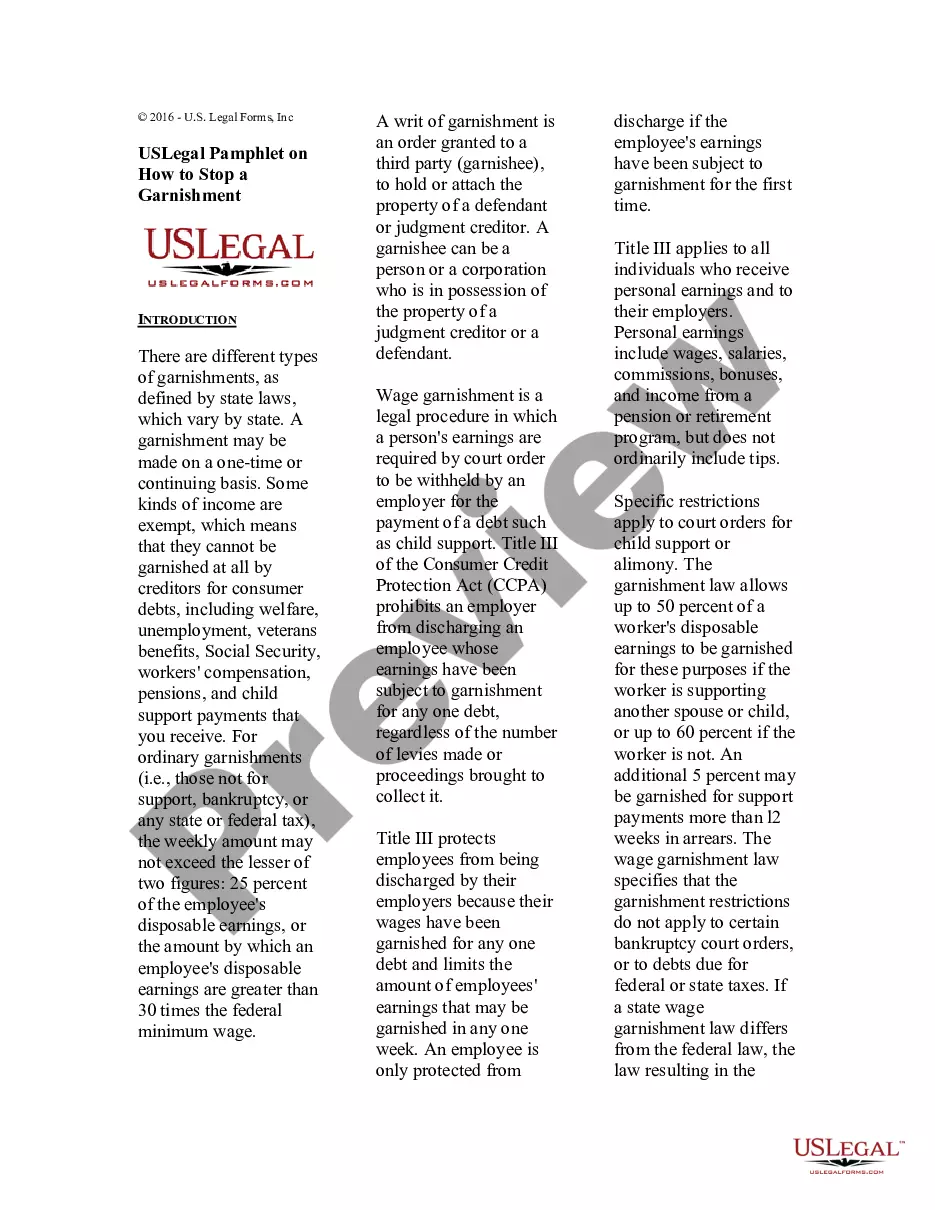

It releases your garnishment! When a creditor sues you, they eventually get a judgment in court. With this judgment, they can send a letter to your employer so that they can garnish your wages.A release of garnishment would stop any future garnishments.

The Order dissolves the existing writ of garnishment. It means that whatever was being garnished, wages or bank accounts, are no longer subject to the writ of garnishment.

It means that the court order to your employer to garnish your wages is dismissed. However, if you still owe money to the creditor, the creditor still can pursue you through other channels including if you start a new job elsewhere.

If you are served with a garnishment summons, do not ignore these documents because they do not directly involve a debt that you owe. Instead, you should immediately freeze any payments to the debtor, retain the necessary property, and provide the required written disclosure.

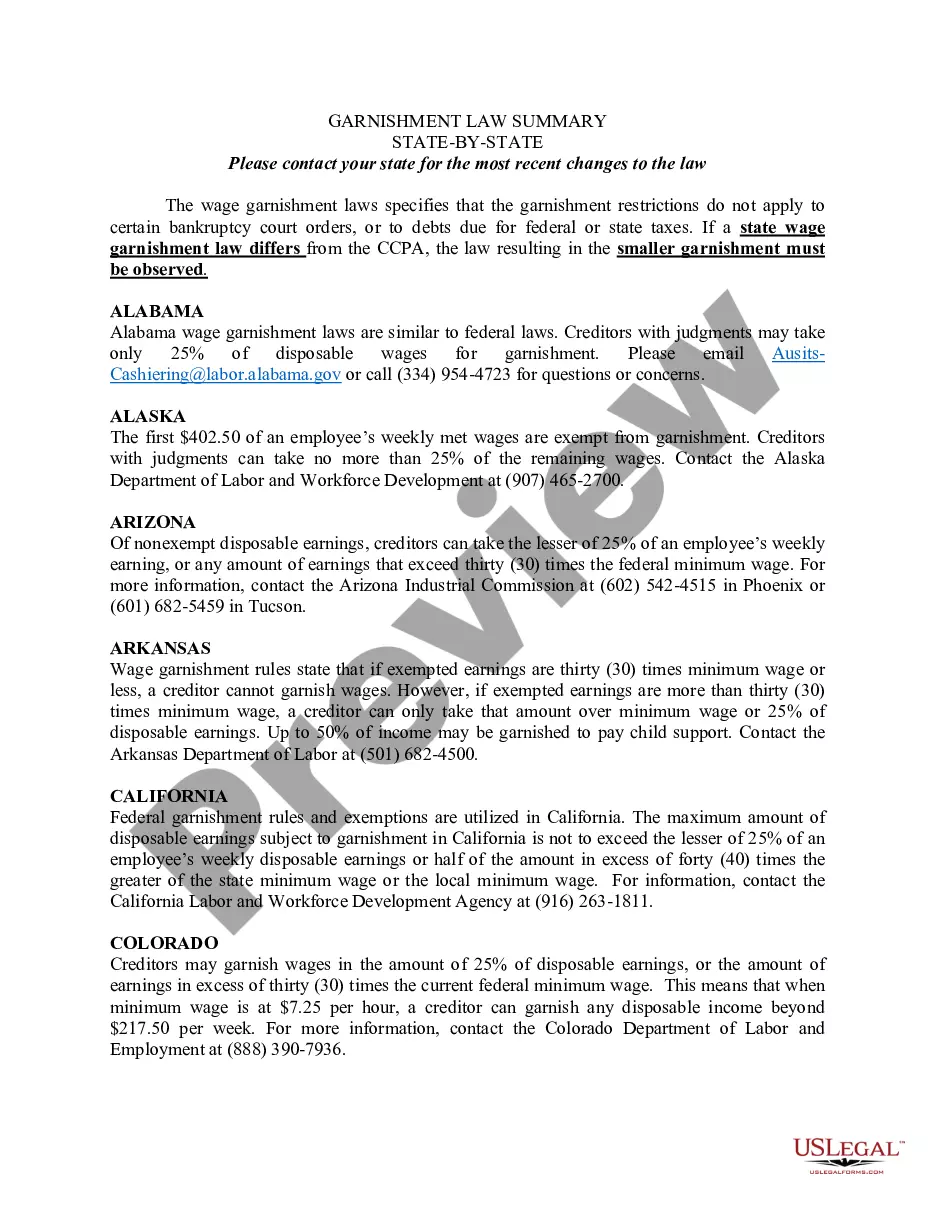

What you can do about wage garnishment.You have to be legally notified of the garnishment. You can file a dispute if the notice has inaccurate information or you believe you don't owe the debt. Some forms of income, such as Social Security and veterans benefits, are exempt from garnishment as income.

Like federal law, in Nevada, up to 50% of your disposable earnings may be garnished to satisfy an order for the support of any person, such as spousal or child support, if you're currently supporting a spouse or a child who isn't the subject of the order.

In most states, employers answer a writ of garnishment by filling out the paperwork attached to the judgment and returning it to the creditor or the creditor's attorney.

Federal Wage Garnishment Limits for Judgment Creditors If a judgment creditor is garnishing your wages, federal law provides that it can take no more than: 25% of your disposable income, or. the amount that your income exceeds 30 times the federal minimum wage, whichever is less.