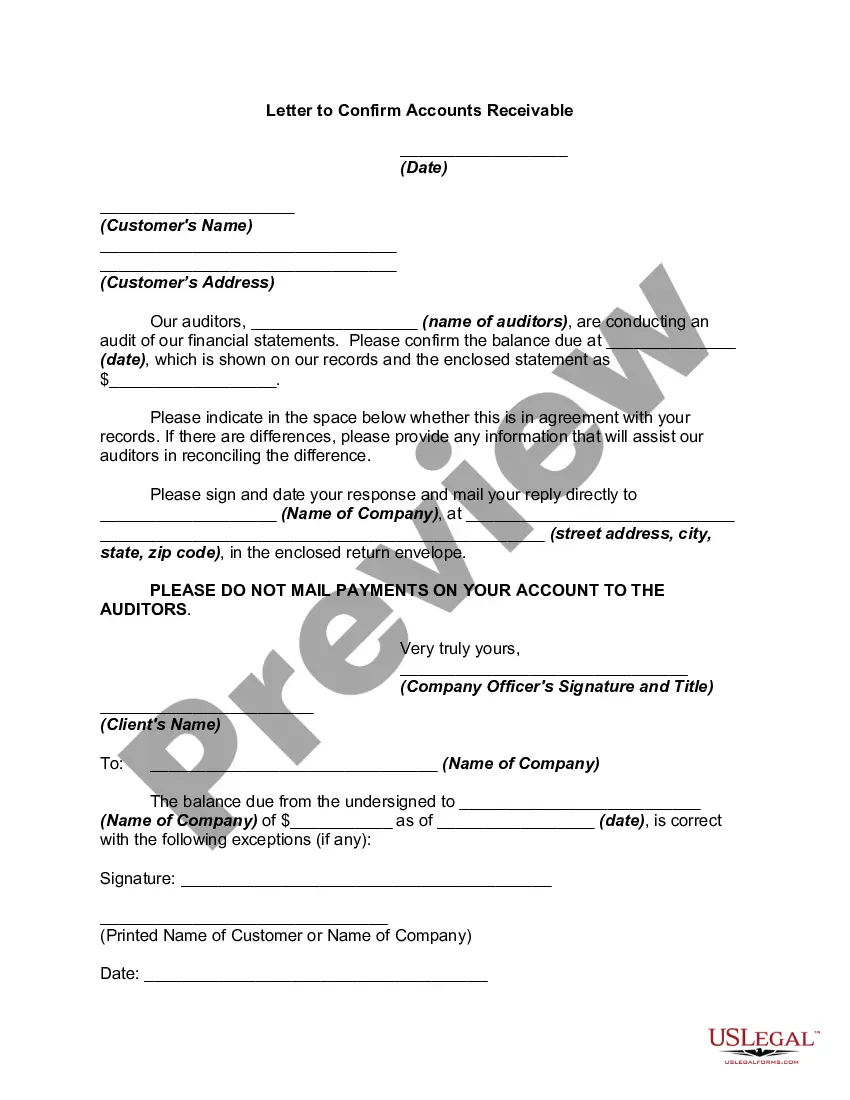

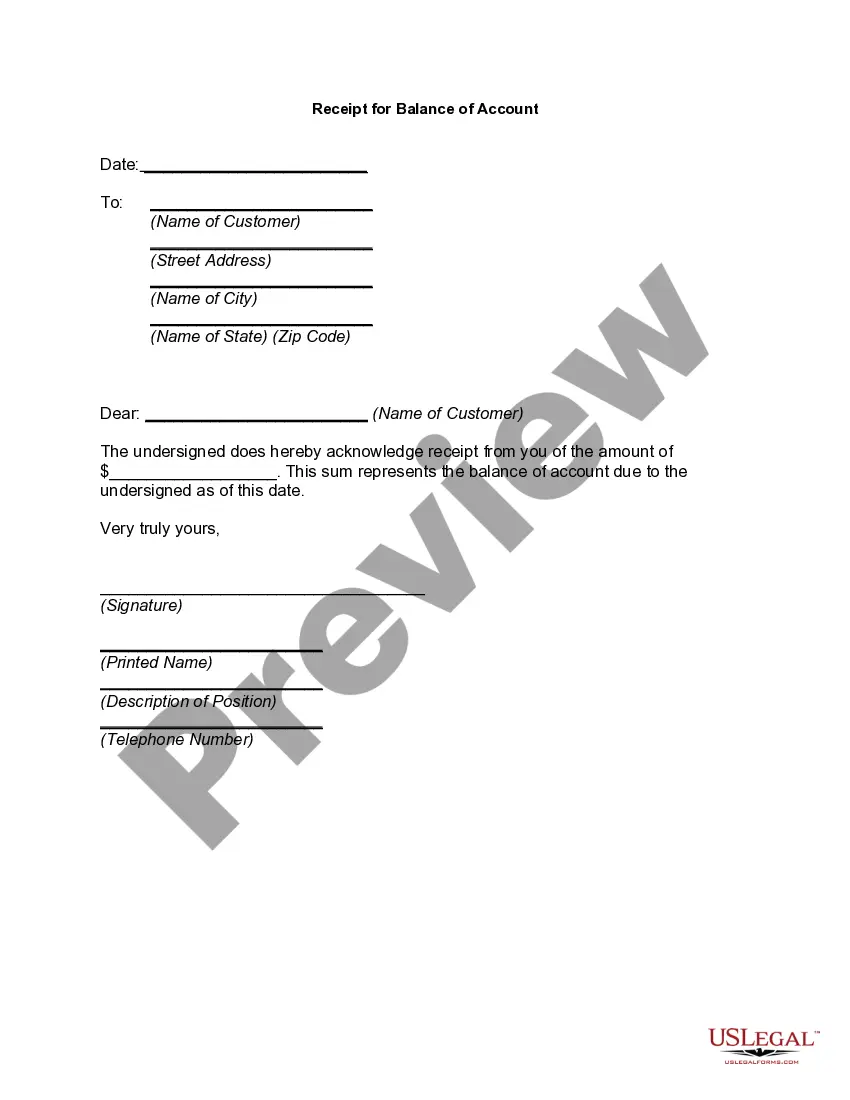

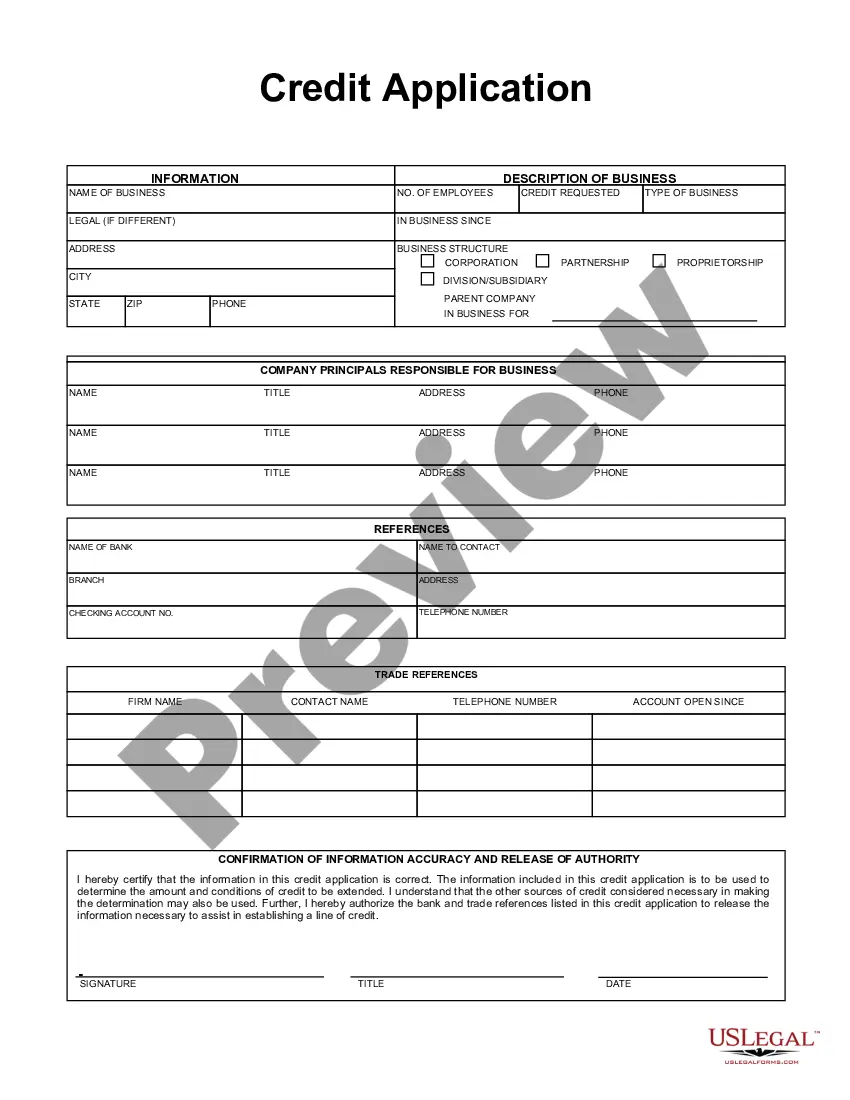

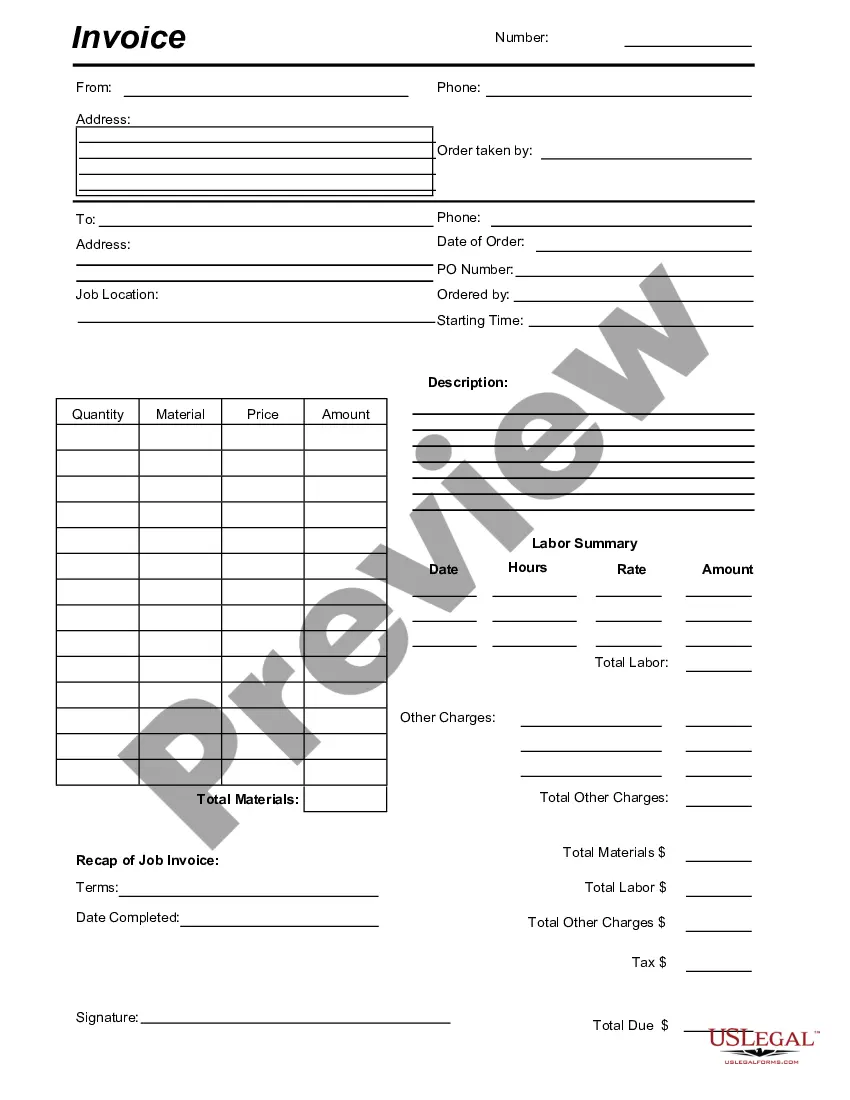

New Jersey Daily Accounts Receivable

Description

How to fill out Daily Accounts Receivable?

If you seek to be thorough, acquire, or generate authentic document templates, utilize US Legal Forms, the largest assortment of legal forms, accessible online.

Employ the site’s user-friendly and efficient search to find the documents you require.

A variety of templates for business and personal purposes are categorized by types and jurisdictions, or keywords.

Step 4. Once you have found the form you need, click the Purchase now button. Choose the pricing plan you prefer and enter your information to register for the account.

Step 5. Complete the payment. You can use your credit card or PayPal account to finalize the transaction.

- Utilize US Legal Forms to obtain the New Jersey Daily Accounts Receivable with just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and then click the Obtain button to locate the New Jersey Daily Accounts Receivable.

- You can also access forms you have previously downloaded in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure that you have selected the form for the correct city/state.

- Step 2. Use the Review option to examine the form's content. Don't forget to read the details.

- Step 3. If you are dissatisfied with the form, use the Search field at the top of the screen to find alternative versions of the legal form template.

Form popularity

FAQ

The daily task of an accounts receivable clerk includes managing and recording incoming payments, sending invoices, and following up on overdue accounts. For organizations looking at New Jersey Daily Accounts Receivable, an efficient clerk ensures timely collections. This position plays a key role in maintaining the company's financial health.

To calculate days in AR,Compute the average daily charges for the past several months add up the charges posted for the last six months and divide by the total number of days in those months.Divide the total accounts receivable by the average daily charges. The result is the Days in Accounts Receivable.21-Feb-2022

The average accounts receivable turnover in days would be 365 / 11.76, which is 31.04 days. For Company A, customers on average take 31 days to pay their receivables.

To calculate days in AR,Compute the average daily charges for the past several months add up the charges posted for the last six months and divide by the total number of days in those months.Divide the total accounts receivable by the average daily charges. The result is the Days in Accounts Receivable.21-Feb-2022

Example of Days Sales Outstanding With a DSO of 21.7, Company A has a short average turnaround in converting its receivables into cash. Generally speaking, a DSO under 45 days is considered low. However, what qualifies as a high or low DSO may vary depending on the business type and structure.

Accounts receivable days is the number of days that a customer invoice is outstanding before it is collected.

Account receivable (AR) at the beginning and end of the time period. Accounts payable (AP) at the beginning and end of the time period. The number of days in the period (e.g., year = 365 days, quarter = 90)

The first metric is Days in Accounts Receivable (A/R). Days in A/R refers to the average number of days it takes a practice to collect payments due. The lower the number, the faster the practice is obtaining payment, on average. Days in A/R should stay below 50 days at minimum; however, 30 to 40 days is preferable.

The average accounts receivable turnover in days would be 365 / 11.76, which is 31.04 days. For Company A, customers on average take 31 days to pay their receivables.

Just divide your AR the money due to you from customersby your AP, the total short-term liabilities like credit cards and outstanding bills. If you have long-term loans, only include the monthly payment in this total. The ratio will vary by business, but several rules of thumb: A ratio of or less is risky.